Will the rotation into value continue?

Thought Leadership

Will the rotation into value continue?

Wed 31 Mar 2021

The year of the vaccine

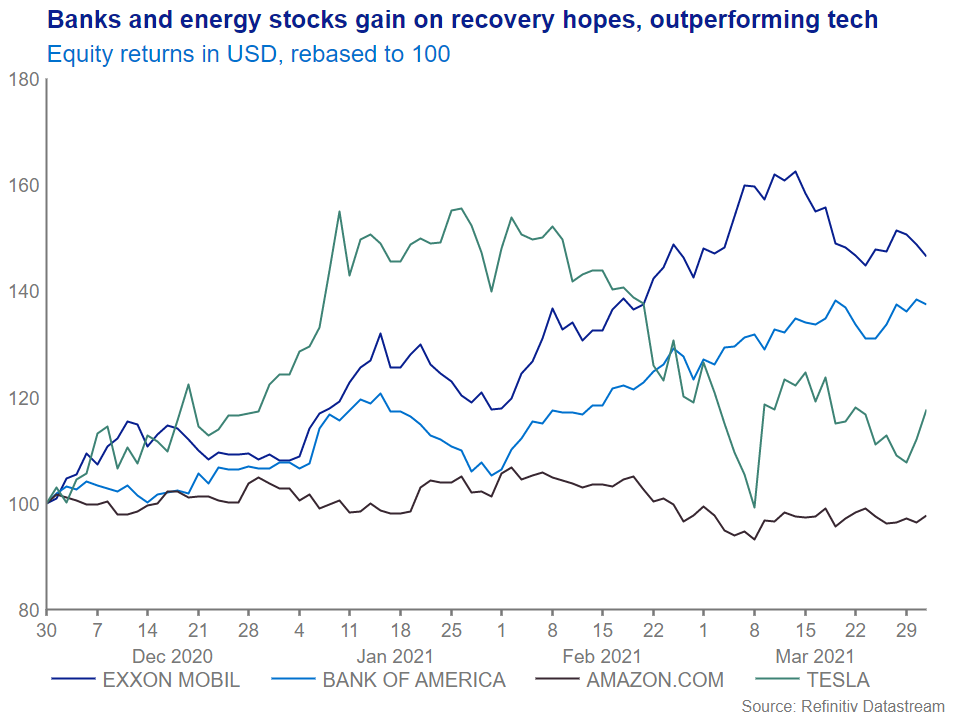

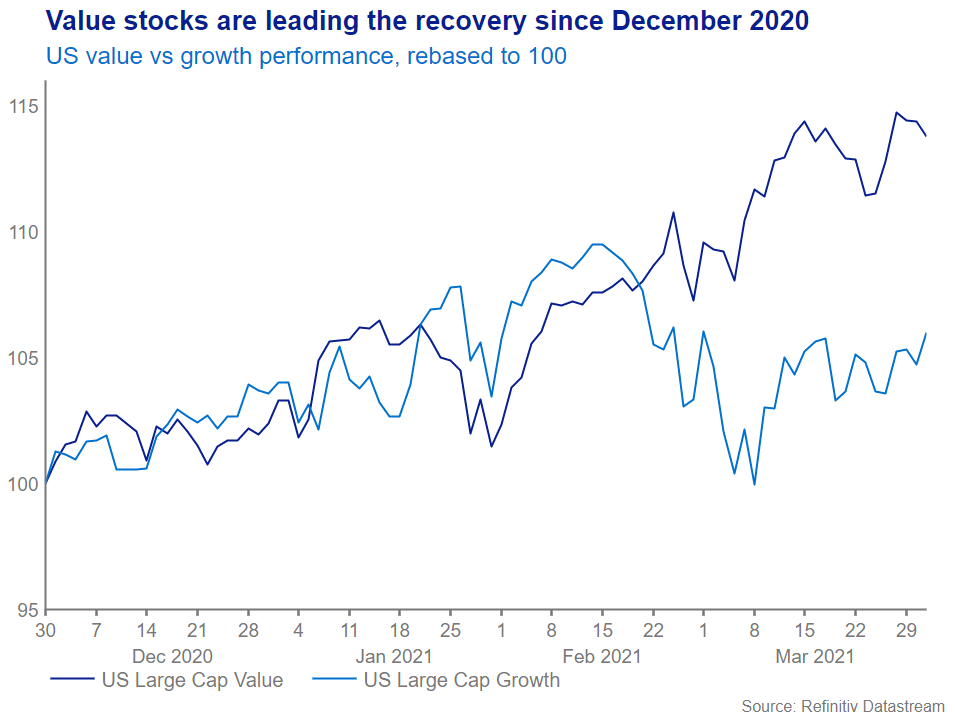

Successful vaccines, the passing of the US election and an increasing belief in strong global growth in 2021 have all come together to spur global equity markets and risk assets higher over the past few months. After a decade of fast-growing technology companies dominating the markets, a strong economic recovery could cause a major shift. Value stocks – or cheaper shares such as banks and energy firms – have handsomely outperformed fast-growing stocks such as the big tech names in 2021 so far. Stocks such as Bank of America and Exxon are beating the likes of Tesla and Amazon.

And then there are rising bond yields and inflation…

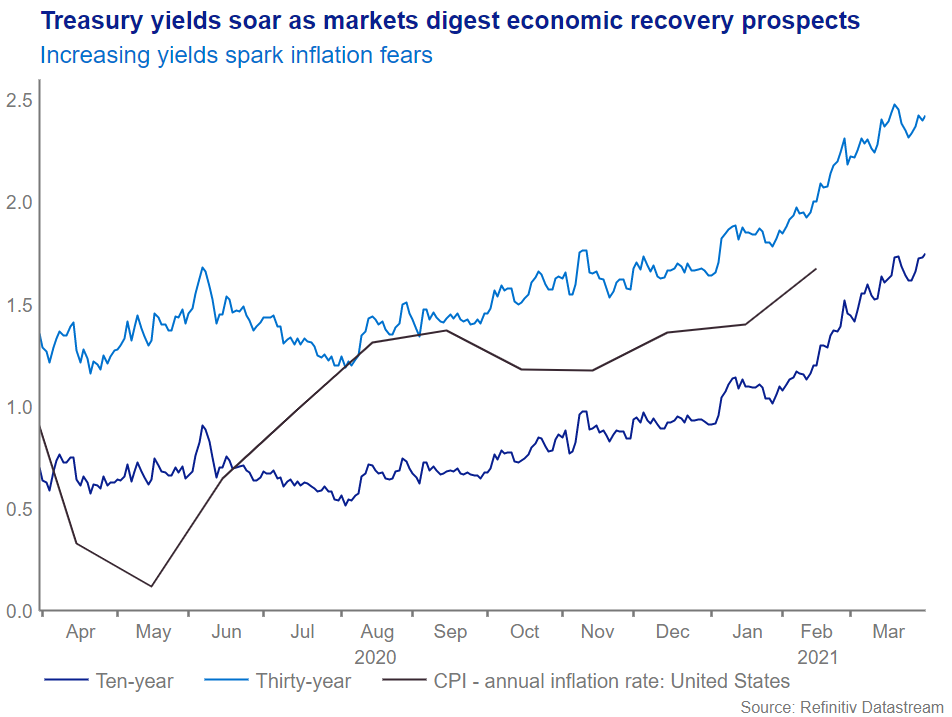

US Federal Reserve Chairman Jerome Powell suggested that the central bank would let inflation run hotter if it helped achieve full and inclusive employment. Recent concerns about inflation have driven bond yields higher. This month yields on the benchmark US 10-year treasury climbed to 1.75%, the highest since January 2020, while the 30-year treasury yield jumped to 2.5% for the first time since August 2019. Higher inflation, after all, often comes with an uptick in economic growth, which should benefit value stocks that are economically sensitive – like those of banks and energy companies – more than those that aren’t, like tech. That’s reflected in share price moves this year too: US energy and banks stocks have outperformed tech stocks by 33% and 16% respectively.

Can the rotation sustain itself beyond 2021?

While it remains to be seen how long value leadership will last, many of the drivers that led investors to flock to growth stocks have reversed and now favour value stocks. The jury is still out on whether we will see a generalised correction in stock markets, and there would have to be the prospect of interest rate rises or other monetary tightening before that occurs. We believe that even if a rotation takes place there will be winners and losers among both growth and value shares – they will not all go up, and all go down. For instance, over the past year, people have made themself even more familiar with digitalisation by shopping online and working from home. Therefore, technology shares and other growth companies could continue to serve investors well even in a post-Covid world.

Weekly market update: The Fed is not the answer to everything!

US, UK and European equities were relatively unchanged in Sterling terms last week, faring -0.1%, +0.1% and -0.1% respectively, amid concerns that the rate of global growth could start decelerating. Japanese equities were up +4.0% despite the resignation of Prime Minister Yoshihide Suga, while emerging market equities were up +2.7%, positive for a second week in a row after the Chinese tech sector had fallen significantly in previous weeks. Globally, stocks were up +0.3%, with energy and financials being the only sectors exhibiting losses. The US 10Y Treasury yield was down -1.5bps finishing the week at 1.322%. The German 10Y Bund yield was up +6.2bps amid higher than expected inflation in the euro area. Sterling was up +0.8% against the US Dollar and unchanged relative to the Euro. In US Dollar terms gold lost -0.1%, while oil prices rose slightly by +0.1%.

Weekly Market Update: Stock gains muted despite signs of a trade deal

Global equities were positive last week, however energy stocks fell precipitously on plummeting oil prices, so that overall in local terms returns were +0.8%. Positive sentiment was boosted as the off-again, on-again negotiations between the US and China appear to be on-again, while a revised estimate of Q3 GDP showed the US economy expanded at […]

Macro of the Week – Fed hikes rates, more expected

As widely expected the FOMC raised the Fed Funds Rate target by 0.25% to a range of 1.5% – 1.75%, in what was a unanimous decision by the committee. It was the sixth rate hike since the GFC as the central bank looks to ‘normalise’ interest rate policy and was the first major decision under […]

Weekly Market Overview – Equity markets bounce despite inflation scare

Despite a brief panic on Wednesday when US inflation figures came in higher than expected, stoking fears of accelerated interest rate rises, markets had a strong week across the board following 2 weeks of significant market weakness. US markets were up 4.4% in USD terms, however weakness in the currency meant the return in Sterling […]

WEEKLY MARKET UPDATE: SECOND WAVE FEARS SEE MARKET JITTERS

Equity markets sold off across the board last week, declining initially amid fears of a secondary wave of infections and a pessimistic outlook from the Fed, although there was a sharp recovery later in the week on additional stimulus expectations. In local terms global equities fell -2.5%. However due to Sterling weakness, in part due […]

Weekly Market Update: US Equities continue their rebound, oil enters bear market and Democrats win the House

Read our full Market Update Week 45 Market Update US stocks continued their rebound this week, with energy and financials sectors up +1.4% and +1.5%, while the tech sector suffered as Amazon and Apple saw big falls. General Electric also fell to it lowest level since the GFC. Emerging Market equities were down -2.4% in Sterling […]

Weekly Market Update: Sterling depreciation buoys Global Equities, bond yields fall

Global stocks were down -0.4% in local currency terms last week, however returns for UK investors were +0.3% after Sterling depreciated versus major global currencies, down -0.5% and -0.3% versus the US Dollar and the Euro respectively. US, UK and European stocks returned +0.3%, +0.4% and -0.3% over the week, whilst Emerging Markets equities posted […]

Weekly Market Update: Markets rally, Tesla delisting cancelled

Read our full Market Update Week 34 Market Update Last week and Monday was a positive period for risk assets, with global stocks returning +0.7%. EM equities gained the most, up +3.2% in Sterling terms and 4.6% in local terms, buoyed by Donald Trump’s announcement that he is prepared to resume talks with China (although […]

Weekly Market Update: US growth powered by strong retail sales

Read our full Market Update Week 33 Market Update Returns were mixed for equities in local terms as, aside from US equities which made a +0.7% return, all major regions fell. Similarly in Sterling all markets were down bar US and global equities which gained +0.8% and +0.1% respectively. Both European and Japanese markets returned […]

Weekly Market Update: Markets correct on NAFTA and Tech concerns

Read our full Market Update Week 36 Market Update Equities saw sizeable falls across the board last week, both in local and Sterling terms. UK stocks fell -2.0% with US and Global stocks down -0.7% and -1.5% in GBP. Other areas fared even worse, as European, Japanese and EM equities lost -2.3%, -2.6% and -2.8% […]

Weekly Market Update: US sanctions further Turkish instability

Read our full Market Update Week 32 Market Update As the pound continued its decline into last week, in local terms equity markets fell across the board aside from UK equities which made a +0.6% return. In Sterling all markets were up bar European equities, with US and global equities gaining the most with +1.9% […]

How British retailers “gamed” themselves into a corner

When my daughter was first born she had trouble sleeping and hated her cradle. So I used to hold her by to the kitchen fan (new parents take note, this works!) for about 10’, until she was fast asleep. It worked magic every time. Until it didn’t. A few weeks later she didn’t like it […]

Weekly Market Update: Bank of England and ECB keep rates unchanged

Read our full Market Update Week 37 Market Update Equities rose across the board last week, both in local and Sterling terms. UK stocks gained +0.4% with US and Global stocks up +0.1% and +0.3% in GBP terms. Other areas fared even better, as European and Japanese equities rose +0.8% and +0.6% respectively. However, Emerging […]

Weekly Markets Update: US Equities reach highs; May’s Chequers plans ambushed

Read our full Market Update Week 38 Market Update UK stocks traded higher with the FTSE 100 edging closer to the 7500 level, closing at 7472 point, up +2.65% for the week. In the US the S&P 500 reached new highs, returning +0.8% in GBP terms. Global stocks were up +1.5% in local terms and +1.6% […]

Weekly Market Update: Stocks sell off globally on rising bond yields

Read our full Market Update Week 41 Market Update Global indices suffered significant falls last week, down -4.1% in local terms and -4.5% in Sterling terms. US equities led the weak performance, experiencing their biggest losses in 8 months on Wednesday. Technology stocks were particularly affected as market participants reacted badly to rising bond yields. […]

Weekly Market Update: Global equities rebound, US treasury yields pick up, Italy still turbulent

Read our full Market Update Week 42 Market Update US indices rebounded this week, leading the pack with a +1.3% gain after the significant correction that investors have seen in recent weeks. US stocks are climbing as tax cuts have lead to significant EPS growth and many companies, including financials, have beaten earnings estimates. The US […]

Weekly Market Update: Global stocks down for the week, capital flows to US bonds, UK budget contingent on Brexit

Read our full Market Upate Week 43 Market Update Global stocks continued to slide this week, with US stocks leading indices lower, the S&P 500 falling -2.2% in Sterling terms. The NASDAQ lost -3% due to disappointing results from Tech companies and a drop in the Consumer Discretionary sector following a disappointing sales outlook from […]

Weekly Market Update: Equities rally ahead of US midterms

Read our full Market Update Week 44 Market Update Global stocks rebounded this week, with Emerging Market equites soaring over 5% in GBP terms. The S&P 500 was up 1.9% and Japanese equities saw a healthy rebound returning 3.4%. US 10-year Treasury yields rose to 3.22%, but didn’t break through 3.25%, a resistance level investors are […]

Inflation momentum will recede. But prices may remain elevated.

There’s a strong possibility we may see the end of the episode soon. But supply chains could take long to mend and overall price levels could remain elevated versus pre-pandemic numbers.

US Midterm Elections: What is the outlook for markets?

The US goes to the polls today for midterm elections. Every seat of the lower chamber (the House) is up for election (as it is every two years!), while a third of the upper chamber (the Senate) will also be voted on (Senators are elected every six years). For comparison to the UK Parliament, the […]

Weekly Market Update: Equities rally despite no one liking Facebook’s outlook

Read our full Market Update Week 30 Market Update Japanese and Emerging Market equities lead markets higher last week, gaining +2.6% and +2.2% respectively in Sterling terms. These regions had their best week in more than two months, as China’s stimulus measures buoyed the region. News of an agreement reached between President of the European Commission […]

Weekly Market Update: Global stocks continue their rebound while Oil prices drop further and Brexit uncertainty heightens

Read our full Market Update Week 46 Market Update Global stocks continued their rebound this week, with both Global and European equities up +0.3%. Emerging Market equities led the pack, returning +2.5% as the slide in oil prices gave a boost to emerging market currencies. UK Stocks were hit by further Brexit volatility, hardest hit stocks […]

Weekly Market Update: Global stocks rally with US stocks higher after Fed’s comments

Read our full Market Update Week 48 Market Update Last week US equities had already seen a solid rebound, up over 2% for the week in US Dollar terms, when on Wednesday Jerome Powell’s apparent U-turn on interest rates, stating that “they remain just below the broad range of estimates of the level that would […]

Weekly Market Update: Equities sell off on renewed trade war fears

Read our full Market Update Week 49 Market Update US equities sold off significantly last week, down -4.4% in Sterling terms, as trade war concerns weighed on American stocks, erasing the gains made in the previous week. Global equities were down -3.5% in Sterling terms, with all sectors apart from utilities experiencing negative returns. Emerging Market […]

Weekly Market Update: China concerns see market volatility

Read our full Market Update Week 50 Market Update Last week the main driver for UK investor returns was the weakness in Sterling, which fell -1.1% vs USD and -0.5% vs EUR. The majority of the drop came on Friday as Theresa May’s inability to win concessions from the EU created further uncertainty about the future […]

Weekly Market Update: Sterling continues to depreciate, global yields

Market Update This week saw mixed equity returns, with global stocks down -0.3% in Sterling terms. Emerging Markets posted a strong gain of +1.3%, which was supported by the Sterling depreciation observed across the period, while US stocks were down -0.7% for the week. Japanese equities fell -0.8% in local currency, however, the GBP/JPY rate […]

Who will be the leaders of Artificial Intelligence? How should “big tech” be regulated

We are at an inflection point. Technological innovation drives our economy, and ultimately, our standard of living. From rail roads to the Internet, technological progress has pushed our productivity levels to new heights, and we are now on the brink of the next step of this evolution. Artificial Intelligence. Once just the topic of sci-fi […]

Weekly Market Update: Global equities rally, Sterling depreciates as likelihood of a no-deal increases

Market Analysis This week saw strong equity market returns, with global stocks up +2.0% in Sterling terms. US equities were up +2.6% for the week, with returns enhanced by Sterling depreciation versus the US Dollar and earnings outperformance from both Google and Starbucks. UK, European and Japanese equities were up +0.6%, +1.1%, and +0.5% respectively. […]

Weekly Market Update: Stocks sink as the Fed disappoints traders

Market Analysis This week saw stocks suffer globally, with global stocks down -1.1% in Sterling terms. US equities suffered their worst week thus far in 2019 as market sentiment was dealt twin blows by disappointing signals from the Fed and the announcement of new tariffs on imports from china. US equities were down -1.2% for […]

Are UK risk assets pricing in the possibility of political realignment?

UK assets continue to trade at a discount to the rest of the world, however, with so much political uncertainty facing the UK this may be justified. Boris Johnson’s new special adviser Dominic Cummings is by all means unorthodox. Mr. Cummings was the Campaign Director for Vote Leave in 2016, and used machine learning and data […]

Weekly Market Update: Yield curve inversion spooks markets

Read our full Market Update Week 33 Market Analysis Last week saw equities decline globally, both in local and Sterling terms. US stocks recorded a third straight week of losses as trade and growth worries unsettled investors, down -1.6% in Sterling. The typically defensive consumer staples and utilities sectors performed best within the S&P 500 […]

Weekly Market Update: Global equities decline as trade war escalates

Read our Full Market Update Week 34 Market Analysis Last week equities continued to decline, both in local and Sterling terms. Emerging Markets led the decline, falling -1.5% in Sterling terms. US, UK and Japanese stocks fell -0.9%, -0.2% and -0.9% respectively. European stocks were flat in Sterling terms. Globally, the best performing sectors were […]

Weekly Market Update: BoE raises rates to highest level since 2009

Read our full Market Update Week 31 Market Update In local terms, equity markets fell across the board, aside from US equities which made a +0.8% return in USD (+1.5% in GBP). Global equities were flat in local terms but up +0.7% in Sterling as the Pound hit its lowest level since last September amid […]

Weekly Market Update: Oil spikes as US inflation hits Fed target

Read our full Market Update Week 26 Market Update Global equities saw a second straight week of negative performance, down -0.7% in Sterling terms, with all major indices experiencing falls in both local and GBP terms. Once again escalating trade tensions were the prime reason for weak performance, although for the second week running UK stocks […]

Weekly Market Update: Trump questions Fed policy

Read our full Market Update Week 29 Market Update Sterling took another hit last week as lack of government unity surrounding Brexit saw the currency fall -0.7% vs USD, -1.1% vs EUR and -1.5% vs JPY. These moves increased returns on overseas equities for UK investors, with Japanese equities leading the way with +2.3% and […]

Weekly Market Overview – Despite scheduled talks, looming trade war roils markets

Donald Trump’s announcement of around $60bn of tariffs against China due to intellectual property violations saw markets experience large losses, as participants feared an escalating trade war. China is expected to hit back with levies aimed at industries and states where Mr Trump’s supporters are concentrated. Equity falls came despite Congress agreeing a $1.3tn spending […]

Weekly Market Overview– Equities fall on rising US yields

Equities suffered their worst week since 2016 and subsequently fell over 4% on Monday as concerns over rising US Government bond yields spilled over into risk assets. As of Monday, US 10Y Treasury yields were at 2.84%, having increased from 2.4% at year end, resulting in a total return of -3.1% over the period. The […]

Macro of the Week – US wages accelerate

US hiring picked up in January and wages rose at the fastest pace since the GFC. Hourly earnings increased 0.3%, resulting in an unexpected year-on-year increase of 2.9%, up from 2.7% in December (which was also revised up from 2.5%). This was on the back of a nonfarm payrolls increase of 200k, which was upwardly […]

Monthly Market Outlook: February 2018

Read our Monthly Market Update Global equity markets were positive again, registering a 5.3% performance in January, benefiting from the positive sentiment and the passing of the US tax reform at the end of 2017. The macroeconomic environment was less supportive, however, as some key indicators suggested that global economic momentum was slowing down in […]

Weekly Market Overview – Nervous equity markets continue to slide

Concerns over US Government debt levels, softening global macro data and a potentially hawkish Federal Reserve once again lead to negative equity returns after a significant sell-off in the previous 2 weeks. All global equity markets are now in negative territory for the year in both local and Sterling terms. Last week US markets were […]

Macroeconomic View – German exports accelerating

German exports were weak for the month, up only 0.3%, but are still accelerating year-on-year. Chinese exports were stable, but imports picked up significantly, offsetting last month’s weak data. UK The Markit Services PMI dropped slightly to 53 from 54.2. The Halifax House Price Index year-on-year for the 3 months to January fell from 2.7% […]

Macroeconomic View – French unemployment down

French ILO unemployment dropped unexpectedly from 9.6% to 8.9%. It was further proof of the strength in the French, and subsequently, the European economy. European equities lost 1.5% briefly after the US inflation report was released, with figures higher than expected. The market recovered, but the move is indicative of the factors that affect traders. […]

Macro of the Week – US inflation accelerates

US CPI inflation surprised markets, remaining unchanged in January at 2.1%, driven by sharp increases in clothing and energy costs. There had been expectations for a fall to 1.9%. Core inflation was also stable at 1.8%, again above expectations […]

Weekly Market Overview – Recovery continues despite rates normalisation talk by Fed

The market sell-off at the start of February was largely attributed to fears of rising interest rates in the US, with concerns that planned increases in fiscal stimulus to an already strong economy meant the Fed was getting behind the curve. Last week various members of the FOMC, although notably not the Chair Jay Powell, […]

Macro of the Week – UK GDP slowing

The UK economy grew more slowly than previously estimated in Q4 2017, increasing by 0.4% quarter-on-quarter according to the second estimate by the ONS. This figure was a 0.1% downgrade from the original estimate. The downward revision was due to slower […]

Weekly Market Overview – Markets fear Taylorisation of Fed and trade wars

Markets continued their recent rocky period, with two separate events causing unease for investors. The first was Jay Powell’s first congressional testimony on Tuesday where he hinted at a faster pace of interest rate rises and stated a preference for rules based interest rate decisions. For example the Taylor Rule proscribes an interest rate for […]

Weekly Market Overview – US jobs report eases inflation fears

Markets had a strong run last week with all major equity markets posting gains in both local and GBP terms, except for Japan which suffered a loss in Sterling. The market seems to have fully rebounded following the sell–off at the beginning of February, with the Nasdaq back at a record high. US equities led […]

Monthly Market Outlook: March 2018

Read our Monthly Market Update February saw the return of volatility for stocks after nearly two years, as a confluence of catalysts affected equity markets: US Bond yields breaking critical levels above 2.55%, a new more hawkish and uncertain Fed, the deterioration of the global trade climate and renewed political uncertainty in Europe and the UK. […]

Weekly Market Overview – Trade war concerns weigh on markets

Both US equities and the US Dollar fell last week when multinational companies such as Boeing were hit as Donald Trump sought to impose new tariffs on China, pressing China to cut its trade surplus with the US by $10bn. As a result, there is an increased likelihood of a trade war between the worlds […]

Weekly Market Overview – Despite US assurances, trade war fears still weigh on markets

With the continued escalation of threats of tariffs between the US and China, markets suffered another week of negative returns. Global equities were down -1.0% in Sterling terms, dragged lower by US equities which returned -1.8%. Emerging Market and Japanese equities also suffered, down -1.1% and -1.0% respectively. European equities were relatively unscathed with a […]

Weekly Market Update: Global stocks up heading into earnings season

Read our full Market Update Week 28 Market Update Global markets were up last week by +1.4%, despite a mid-week blip as once again Donald Trump increased the stakes against China, threatening tariffs on $200bn worth of exports. US stocks were up +1.9% in Sterling terms, however Emerging Market equities gained the most, up +2.0%. […]

Monthly Market Outlook: April 2018

Read our Monthly Market Update After February ended a run of 11 consecutive months of positive, less volatile returns for equities, March saw risk assets continue to suffer as US bond yields peaked near 3% and fears of a global trade war came closer to fruition, with President Trump placing tariffs on Chinese imports of steel […]

Weekly Market Overview – Markets shrug off US strikes on Syria

Markets were volatile last week due to the possibility of air strikes on Syria, however opened slightly up on Monday morning after the US took action over the weekend. Equity markets were positive across the board in local terms last week, however Emerging Market and Japanese equities posted losses in GBP terms as the Pound […]

Macro of the Week – UK GDP sees marginal improvement

The NIESR GDP growth estimate for the 3 months to March was revised up to 0.2% from 0.1% in February, having been revised down from 0.3%. However the figure is still a reduction from the 0.4% growth seen in Q4 2017. Quarterly growth of 0.2% equates to just 0.8% annual growth. According to Amit Kara, […]

Mazars Weekly Market Update: Apple sours market recovery

Read our full Market Update Week 16 Market Update Equity markets saw another week of recovery with positive returns across all regions. Returns for UK investors were boosted by a weak return from Sterling, which sold off 1.75% on a trade weighted basis as Mark Carney, the Governor of the Bank of England, made comments […]

Mazars Weekly Market Update: Weak UK growth sees Sterling sell-off

Read our full Market Update Week 17 Market Update Global equity markets were flat to positive in local terms last week, however a large sell-off in Sterling due to fading expectations for a rate hike at the next MPC meeting in May meant that returns were positive for UK investors. Global equities returned 1.6%, US […]

Monthly Market Outlook: May 2018

Read our full Monthly Market Update Following two months of negative returns for risk assets, equities rallied in April as trade war fears were downplayed and positive earnings, especially in the US, continued to come through. The month was also notable in that markets sold off over fears of an escalation of the Syria conflict, […]

Combustible Commodities, Bruised Banks: Why Brexit isn’t the only headwind for UK equities

Whisper it very quietly, lest we jinx it: UK equities have been on a strong run recently. When was the last time you could say that? Certainly not since Brexit, which has been blamed for the poor performance versus global peers. However looking at the 4 quarters leading up to and including the Brexit vote, […]

Weekly Market Update: Italian populist government calms markets, US populist tariffs re-ignite concerns

Read our full Market Update Week 22 Market Update Markets sold off and yields rose in the first half of the week on fears about repercussions of the Italian President rejecting the populist coalition’s choice of finance minister and attempting to install a technocrat government. There were concerns that a new set of elections would […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

Weekly Market Update: Markets shrug off US G7 communique snub

Read our full Market Update Week 23 Market Update Last week markets were back in risk-on mode, as Global equities gained +0.9% in Sterling terms, led by US stocks which were up +1.2%. The gains were fairly evenly dispersed amongst sectors, although Utilities were the main loser as Treasury yields crept higher. Japanese equities were […]

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

Weekly Market Update: Global central banks turning hawkish?

Read our full Market Update Week 24 Market Update Global markets had a second straight week of gains in Sterling terms, again led by US equities (+1.0%, +0.1% in local), with European equities also faring well (+1.0%, +1.5% in local). Japanese equities also gained +0.4%, however UK equities and Emerging Market equities were down -0.6% […]

Weekly Market Update: Global stocks fall as economic data disappoints

Read our full Market Update Week 40 Global stock markets fell throughout the week, both in local currency terms and Sterling terms. UK assets led the decline, down -3.5% on the news of weaker economic data out from the services industry. US stocks were down up -0.4% in Sterling terms, with similar returns observed in local […]

Weekly Market Update: Worrying signs for German manufacturing

In a sluggish week for equities, equities fell in both local and Sterling terms. US, Emerging Markets and European stocks each fell -0.6% in Sterling terms, however European stocks were up marginally +0.1% in local terms. Japanese stocks rose slightly, by +0.5% in Sterling terms, while UK stocks fell -0.3%. Over the week Sterling fell […]

iPhone-as-a-service? Enter the period of everything-as-a-service

Charles Darwin gave us the theory of evolution. The species most adept to change survives. This model applies not just to organisms but to economies and businesses. In fact, so ubiquitous is the analogy between business and hunting and survival dynamics the language we use to describe ordinary business processes and transactions often stem from […]

Weekly Market Update: Bond yields rise, Pound rallies on potential Brexit “pathway”

Read our full Market Update Week 40 Global stocks gained throughout the week in local terms, however they fell in Sterling terms after the Pound rallied on news of a potential “pathway” to a Brexit deal. Global stocks fell -1.5% in Sterling terms, with the decline led by weak performance from US and Japanese equities; […]

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

Weekly Market Update: Flexible Federal Reserve Sends Cable and Yields Higher

Read our full Market Update Market Update US equities climbed +1.4% last week with, major indices setting new record highs, as US Federal Reserve Chairman Jerome Powell announced a shift in how the Fed views inflation, saying it won’t increase interest rates to respond to low unemployment levels and also won’t worry as much about […]

From trade wars to tech wars?

Banning the President of the United States from Twitter might have come as a relief for some, but not for Jack Dorsey, the founder and CEO of Twitter itself. In a series of posts he acknowledged that the move has opened a particular can of worms he was previously keen on keeping shut. The discussion […]

Weekly Market Update: Markets Rally for Second Week as Inflation Expectations Return

Global equities continued last week’s gains, rising +0.7% in Sterling terms. UK equities, amongst the top performing major markets, rose by +1.6%. They were supported by rising oil prices and positive returns from energy companies, as the domestic market is overweight to the Energy sector. European equities, amid high volatility, were up +0.8%, due to improved coronavirus infection rates and hopes of a large U.S. economic stimulus. US equities rose +0.4%, the worst performing major region. Globally, Energy was the best performing sector whilst Utilities and Cons. Discretionary were the only sectors to finish the week down. Emerging Markets maintained their strong performance since the start of the year, posting gains of +1.5%. Sterling rose +0.8% and +0.3% against the US Dollar and Euro respectively, continuing its strengthening trend this year. The US 10Y yield rose 4.5bps to 1.2% and the UK 10Y rose 3.5bps to 0.52%. Gold fell -2.0% on the week, while Oil rose +3.7%.

Weekly Market Update: Bonds Sell Off Spills Over to Wider Market

A significant rise in US Treasury yields unsettled markets last week. US equities fell -1.9% in Sterling terms, with Tech stocks suffering their worst week in nearly six months. UK equities fell -1.9%, with Energy and Financials the only two positive sectors for the week. Emerging Markets suffered the greatest sell-off, having led global equity markets so far this year. UK and Emerging Markets are the only major equity markets still positive for the year in Sterling terms. Globally the only positive sector was Energy which was supported by rising oil prices. Investors will keep a keen eye on the OPEC+ meeting this week for any indication of increased oil supply. Japanese equities fell -2.4% in Sterling terms, the worst performing region year-to-date for UK investors. The US 10Y yield continued its rise, up 6.9 bps to 1.4%, at one point hitting 1.6%, and the UK 10Y rose 12.2 bps to 0.8%. Long-term yields are now trading at their highest level since the pandemic. Gold fell -2.3% on the week, while Oil rose +4.4% to $62.7.

Weekly Market Update: Investors dilemma: Cheaper bonds or returning dividends?

Markets returned to positive territory this week, supported in part by progress on the Biden stimulus bill. However, chair of the Federal Reserve Jerome Powell’s speech, with a lack of updates to current policy, disappointed investors leading to a sell-off on Thursday afternoon. US equities rose +1.7% in Sterling terms. UK equities rose +2.5%, with UK equity markets benefiting from rising oil prices. Emerging Markets grew +0.9% in Sterling terms, although this was a more moderate +0.1% in local currency terms. Globally the best performing sector was Energy, whilst IT was the worst performing, as the rising yield environment impacted valuations. Japanese equities rose +1.0%. The US 10Y yield continued its rise, up 16.1 bps to 1.6%, while the UK 10Y fell 6.4bps to 0.8%. Gold fell -1.1% on the week. Oil rose sharply, up +8.4% on the week to $66.5 following the OPEC meeting where it was decided to hold production at current levels, when a rise in production had been anticipated.

Weekly Market Update: Stocks ended the week near all time highs

A positive week for equities saw all major equity markets close the week positive in local currency terms. With Sterling continuing its bullish start to the year this pushed EM equities down to a flat week in Sterling terms. US equities rose +2.0% in Sterling terms, hitting record highs. US equities were helped by falling bond yields, from Tuesday, which helped boost equity investor sentiment. UK equities rose +2.1%. Globally the best performing sector was consumer discretionary, whilst telecoms was the worst performing. Japanese equities rose +1.5%, erasing their losses year-to-date. The US 10Y yield continued its rise, although more modestly, up 5.9 bps to 1.6%, while the UK 10Y rose 6.6bps to 0.8%, reversing last week’s fall. Gold rose +0.8% on the week. Oil fell, after last week’s strong rise, down -1.4% on the week to $65.8. Oil is up +32.6% on the year, highlighting the extent to which vaccination programmes are increasing forecasters’ outlooks for economic activity later this year.

Weekly Market Update: The Yield, Not “Inflation” Will Determine the Rotation

Equity market gains early last week were, broadly speaking, eroded as bond yields continued to rise, reaching one-year highs. Amid falling oil prices and rising political uncertainty caused by potential bans on vaccine exports coming out of the EU, many major equity markets fell last week. US equities fell -0.5% from record highs in Sterling terms, despite the country surpassing 100 million vaccinations on Friday. UK equities fell -0.7%, now down -2.4% from their 52-week highs in January. Globally the best performing sector was healthcare, whilst energy, due to oil prices, was the worst performing. Japanese equities rose +3.6% and are the best performing major equity markets this year. The US 10Y yield continued its rise up 9.6bps to 1.7%, while the UK 10Y rose 1.6bps to 0.8%. Gold rose +1.3% on the week. Oil has seen back-to-back weekly declines, down -6.1% to $61.2 a barrel, due to a glut of supply and weakening demand forecasts.

Weekly Market Update: Rational Exuberance

Markets opened positively this week thanks to the impact of stronger than anticipated US payrolls data released over the bank holiday. Meanwhile, the EU vaccination campaign is finally beginning to pick up pace. US equities rose +3.4% in Sterling terms, reaching further record highs. UK equities rose +2.7% in the final week before the second phase of lockdown easing. European equities rose +3.2% in Sterling terms, supported by the increased likelihood of fiscal stimulus in the region. Emerging market equities fell in local currency terms, but gained +0.1% in Sterling terms. Globally, the best performing sector was information technology, whilst energy was the worst performing. The US 10Y treasury yield fell slightly down 6.3 bps to 1.7%, while the UK 10Y gilt yield fell 2.1 bps to 0.8%. Gold rose +1.6% last week. Oil fell for the second week, down -2.8% to $59. Oil has fallen almost -20% from its earlier surge, driven partly by a more challenging route out of the pandemic than originally forecast.

Weekly Market Update: US Inflation Unnerves Equity Markets

Global economies are reopening, and moving into the recovery phase, this pickup in activity has lead investors to question the potential impact on inflation. Investors are cautious of whether inflationary effects will be transitory or long-lasting. The US inflation reading unnerved markets and all major equity markets fell last week. US equities fell -2.2% in Sterling terms, partly driven by currency effects, markets had sold off sharply at the start of the week before recovering in the latter half. UK equities, which typically move inversely to Sterling, due to high levels of overseas earnings, fell -1.2%. Japanese equities fared worst last week, caught in global equity volatility and increased lockdowns, falling -4.0% last week. Despite strong Chinese equity performance, emerging market equities fell -3.8% in Sterling terms. The US 10Y yield rose 5.1bps to 1.6%, while the UK 10Y rose 8.2bps to 0.9%. Both gold and oil were nearly unchanged, falling -0.2% and -0.1% on the week respectively.

Is gold a good hedge against inflation?

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise.

Quarterly Outlook: An investor’s inflation and growth playbook

Investing during the past twelve years has been underpinned by a basic principle: market participants have been encouraged to take risks, mainly to offset the trust shock that came with the 2008 financial crisis (GFC). Each time equity prices have fallen significantly, the Federal Reserve, the world’s de facto central bank, would suggest an increase in money printing, or actually go ahead with it if volatility persisted. Bond prices, meanwhile, kept going up, as central banks and pension funds were all too happy to relieve private investors of their bond holdings even at negative yields. Market risk was all but underwritten.

Weekly Market Update: US equities near all time highs as earning beat expectations

Market Update Global equities rallied last week, with US equities leading the way, up +1.4% in Sterling terms, boosted by 87% of US firms beating earnings expectations. European equities were up a similar amount in local terms, however up only +0.4% in Sterling terms. UK equities were up +0.2%, however Japanese equities fell -1.3%. With […]

Weekly market update: How much longer can liquidity mask reality?

Global stocks were down -1.1% in Sterling terms last week amid fears of momentum fading and growth concerns due to the persistence of supply chain issues. Japanese stocks were the only region to post gains, rising by +3.8% in Sterling terms, buoyed by news of prime minister Suga stepping down and expectations of further stimulus. UK, US and European equities were all down -1.5% driven by inflation concerns and uncertainty about the economic outlook. Globally, all sectors exhibited losses apart from consumer discretionary. The US 10Y Treasury yields were up 1.7bps, finishing the week at 1.343%. German 10Y Bund yields were up +2.6bps to -0.332% after the ECB announced it would reduce the pace of its pandemic asset purchasing programme. Sterling fell against the US Dollar by -0.2% and rose by +0.4% vs the Euro. In US Dollar terms gold lost -2.1%, while oil was up by +0.7%.

WEEKLY MARKET UPDATE: MARKETS SLIDE ON US-CHINA CONSULATE CLOSINGS

MARKET UPDATED Despite recent strength, equities closed lower last week as tensions between the US and China were ratcheted up, with the forced closure of the Chinese consulate in Houston and the arrest by the US of a Singapore national who has admitted spying for China. In response China has ordered the US consulate in […]

Weekly Market Update: China’s ‘LTCM moment’ may be the least of its problems, and ours.

Global stocks were relatively unchanged in Sterling terms (down -0.7% in USD terms) last week amid investors’ skepticism around supply chain issues hampering growth, elevated valuations and future monetary policy. Japanese stocks posted gains for a consecutive week, rising by +1.1%, as campaigning began for the next president of Japan’s ruling LDP. UK stocks fell by -0.9% amid higher than expected inflation, while US stocks were up +0.2% driven by a strengthened US Dollar. Globally, all sectors exhibited losses apart from energy stocks which posted solid gains of +2.8%. The US 10Y Treasury yield was up 2.1bps finishing the week at 1.363%, while the UK 10Y yield was up 8.9bps reaching 0.848%. Sterling fell against the US Dollar by -0.7% and remained flat against the Euro. In US Dollar terms gold lost -1.2%, while oil was up by +4.0%.

The UK’s energy market and its broader implications

Much of the recent news in the UK has been devoted to the spike in household energy costs and the potential collapse of the number of providers in that market from around 50 to 10 by the end of winter. In fact, since writing this first draft of this piece 2 providers have gone bust, leaving more than 800,000 customers without a provider. Of itself this is an interesting topic: it seems remarkable that rising wholesale gas prices can rupture the UK energy market and reduce the number of energy providers by 80%. For us the more relevant question relates to the wider economy and how energy costs can impact consumer demand and inflation, which contributes to our discussions when deciding asset allocation. This blog post aims to explore the former and explain the Mazars Investment Team thinking on the latter.

Fight the Fed… when it’s hawkish (and a few words about Germany)

Stock indices in most developed market regions rebounded strongly after Monday’s acute sell off amid fears of Evergrande’s default - global stocks were up +0.7% in GBP terms. EU stocks were up +1.7% despite business activity losing steam, while US stocks rose +1.0% after recording their biggest daily drop since May 12th, on Monday. UK stocks rose by +1.0% as the BoE announced that rates will be unchanged; however holding a more hawkish stance. Globally, Energy stocks continued their upward trend posting solid gains of +4.0% followed by financials, IT and consumer discretionary. The US 10Y Treasury yield was up 8.9bps finishing the week at 1.453%, while the UK 10Y yield was up 7.4bps reaching 0.922%. Sterling fell by -0.4% and -0.3% against the USD and the Euro respectively. In US Dollar terms gold rose by +0.2%, while oil was up by +3.4%.

Weekly Market Update: Reducing to equal weight

Equities in most major markets pulled back amid inflation worries, persistent supply side issues and more contractionary anticipated monetary policy - global stocks were down -1.6% in GBP terms. US stocks were down -1.2% as uncertainty loomed around the federal debt ceiling and the approval of the USD 1 trillion infrastructure bill. EU stocks were down -1.2% amid higher than expected inflation while UK stocks were down -0.3% despite an upward revision of latest GDP figures. Globally, Energy stocks continued their upward trend for another week in a row posting solid gains of +4.9%, with the rest of the sectors pulling back. The US 10Y Treasury yield was up 1.2bps finishing the week at 1.465%, while the UK 10Y yield was up 8.2bps reaching 1.00%. Sterling fell by -1.0% against the USD. In USD terms gold rose by +1.6%, while oil was up by +3.5%.

Weekly Market Update: Port congestion isn’t dealt with interest rate hikes

Equities in most major markets edged higher last week, partly offsetting the previous week’s losses, with global stocks up +0.3% in GBP terms. US stocks were up +0.4% despite the disappointing jobs report published on Friday. European stocks were up +0.2% amid high volatility while UK stocks were up +1.0% despite the BoE’s new Chief Economist raising the alarms on inflation’s persistence in the coming months. Globally, energy stocks outperformed all sectors for a fifth week in a row, posting solid gains of +4.9%, followed by financials, utilities and materials. The US 10Y Treasury yield was up 15.0bps, finishing the week at 1.612%, while the UK 10Y yield was up 15.6bps reaching 1.158%. Sterling rose by +0.5% against the US Dollar. In USD terms gold pulled back by -0.6%, while oil was up by +4.1%, reaching $81 per barrel.

Weekly Market Update: Look it’s China

Equities in most major markets posted gains last week with global stocks up +1.1% in Sterling terms, amid some improved economic figures. US stocks were up +0.8% as the earnings season kicked off strongly with major banks beating earnings expectations. EU stocks were up +1.6% despite a contraction in the industrial sector while UK stocks were up +2.0% amid strong macroeconomic data showing output growth during August. Globally, almost all sectors posted gains with cyclicals outperforming relatively versus more defensive stocks. The US 10Y Treasury yield was up 3.8bps finishing the week at 1.574%, while the UK 10Y yield was up 5.6bps reaching 1.105%. Sterling rose by +1.0% against the US Dollar. In USD terms gold pulled back by -0.4%, while oil was up by +2.5% reaching $82 per barrel.

Monthly Market Update: Policy Challenges

Seen from a bird’s eye view, the Fed has turned more hawkish in preparation to taper asset purchases. As a result, markets are now more prone to respond with volatility to rising risks, of which there’s no shortage: From soaring natural gas prices to impaired supply chains threatening consumers and businesses; from a new status […]

Weekly Market Update: Santa rally, or not, we remain equal weight

Equities in most major markets posted gains last week with global stocks up +1.4% in Sterling terms, amid stronger investor sentiment. US stocks were up +1.7% as positive earnings surprises continued for a second week in a row. EU stocks were up +1.2% despite heightened concerns that a rate hike could come sooner than expected, while UK stocks were down -0.4% as the latest inflation readings remained above the BoE’s 2% target. Globally, most sectors posted gains with healthcare and utilities being the best performing, while materials and telecoms underperformed. The US 10Y Treasury yield was up 6.2bps finishing the week at 1.632%, while the UK 10Y yield was up 3.9bps reaching 1.145%. Sterling remained flat against the US Dollar. In US Dollar terms gold was up +1.4%, while oil was up +2.9% reaching $84 per barrel.

Weekly Market Update: From pandemic to Sustain-omics: The end of liberal capitalism?

Equities in most major markets posted gains last week with global stocks up +1.4% in Sterling terms, amid stronger investor sentiment. US stocks were up +2.0% as positive earnings surprises continued during the busiest week of the earnings season. EU stocks were up +1.2% amid strong corporate earnings, while UK stocks were up +0.5% as the OBR revised its outlook for the UK economy upwards. Globally, consumer discretionary and IT were the best performing sectors while financials and energy were the worst performing. The US 10Y Treasury yield was down 8bps finishing the week at 1.552%, while the UK 10Y yield was down 11.1bps reaching 1.034%. Sterling was down -0.5% against the US Dollar. In US Dollar terms gold was up +0.1%, while oil was down -0.6% to $84.2 per barrel.

Weekly Market Update: Was it a good idea for the BoE to surprise markets? Probably not.

Equities in most major markets posted gains last week with global stocks up +3.3% in Sterling terms, amid continued strong investor sentiment. US stocks were up +2.0% on the back of positive earnings surprises, a dovish Fed meeting and strong employment data. EU stocks were up +3.2%, with the ECB insisting that rates will stay low for the near future. UK stocks were up +1.0% as the BoE unexpectedly kept interest rates unchanged, which caused Sterling to fall -1.4% against the US Dollar. Globally, consumer discretionary and IT were the best performing sectors while financials and healthcare were the worst performing. The US 10Y Treasury yield was down 10.6bps finishing the week at 1.455%, while the UK 10Y yield was down 19.0bps reaching 0.845%. In US Dollar terms gold was up +3.4%, while oil was down -1.3% to $81.2 per barrel.

Weekly Market Update: Operations Managers are the new economists

Equities in most major markets posted minor gains last week with global stocks up +0.3% in Sterling terms, as inflation concerns seem to have stemmed a previously strong investor sentiment. US stocks were up +0.2% as multi-year high inflation data offset positive news on employment data. EU stocks were up +0.2%, despite Covid-19 cases surging in most countries in the region. UK stocks were up +0.7% while EM equities rose by +2.2%, driven by China’s announcement that it would propose easing measures to aid indebted real estate firms. The US 10Y Treasury yield was up 11.0bps finishing the week at 1.561%, while the UK 10Y yield was up 6.9bps reaching 0.914%. In US Dollar terms gold posted solid gains for the second week in a row, up +3.1%, while oil was down -0.1% to $80.4 per barrel.

Weekly Market Update: Inflationary pressures may be moderating. Supply chain pressures aren’t.

Equities in most major markets posted losses last week with global stocks down -0.4% in Sterling terms, as inflation concerns, supply chain issues and rising coronavirus cases dampened investor sentiment. US stocks were up +0.1% with growth stocks exhibiting solid gains, outweighing the losses in more cyclical firms. European stocks were down -1.8%, as countries within the region started imposing restrictions to curb rising Covid-19 cases. UK stocks were down -1.6% amid CPI inflation figures hitting a ten-year high, while EM equities fell by -1.7%. The US 10Y Treasury yield was down 2.2bps finishing the week at 1.548%, while the UK 10Y yield was down 3.5bps reaching 0.880%. In US Dollar terms gold lost some of its previous weeks’ gains, down -1.3%, while oil was heavily down -6.2% to $76 per barrel.

Weekly Market Update: A game of variants

Equities in most major markets posted large losses last week with global stocks down -1.8% in Sterling terms, driven by a sharp sell off on Friday after news that the new omicron coronavirus variant could be extremely contagious. US stocks were down -1.3% despite positive economic data being published earlier in the week, with weekly jobless claims hitting their lowest level since 1969. European stocks were down -3.8%, as certain countries continued to impose restrictions to curb rising Covid-19 cases. UK stocks were down -2.4%, while emerging market equities fell by -2.7%. The US 10Y Treasury yield was down 7.3bps finishing the week at 1.473%, while the UK 10Y yield was down 5.4bps reaching 0.825%. In US Dollar terms gold fell -1.3%, perhaps surprisingly given the perception it is a defensive asset, while oil was heavily down -10.2% to $68 per barrel.

Weekly Market Update: Increasing COVID-19 case count caps equity market rally

Read our full Market Update Market Update Global equities traded higher last week, up +0.5% in Sterling terms. US equities climbed +0.9% with housebuilders, buoyed by promising housing data, leading the way. Other developed markets did not fare as well. UK and European stocks were down -1.3% and -1.1% respectively, driven by both the negative […]

Weekly Market Update: Stock markets post mixed returns on virus fears

Please read our full Market Update Market Update Stocks posted mixed returns last week, with strong performance in the US as the NASDAQ 100 set new record highs, while UK and Japanese stocks closed down -0.9% and -1.8% in Sterling terms respectively. Emerging Market stocks performed well, gaining +2.4% for the week. Technology, Telecoms and […]

Weekly Market Update: Stocks gain globally, Sterling back below 1.30 vs Dollar

Read our full Market Update Week 43 Market Update Global stocks were up in both local currency and Sterling terms last week, however due to a fall in the currency versus other major currencies, Sterling-based investors enjoyed a greater gain; global equities were up +2.1% in Sterling terms and +1.3% in local terms. US stocks […]

Stocks fall across the globe as COVID-19 cases climb, Oil prices drop as Russia refuses supply cuts

Please check out our full Market Update Week 10 Market Update UK equities were down nearly 9% this morning, with the natural resource and banking heavy indices experiencing weakness for three prime reasons. First, coronavirus fears continued to rise as Italy quarantined 16 million residents, with investors fearful of this impact on the global economy […]

Investing in a world without QE

Inflation rising may upend a 12-year investment paradigm. Is there life after Quantitative Easing?

Weekly Market Update: Bond yields rise, gold price declines

Read our full Market Update Week 45 Market Update Global stocks rose +0.8% in local currency terms and +2.1% in Sterling terms in yet another positive week for risk assets. Meanwhile yields rose sharply and Gold had its worst week in three years as there was a flight from defensive assets. In Sterling terms US […]

Monthly Market Update: New Equity Highs as Economies Tread Water

Markets welcomed signs of an easing in geopolitical tensions in October, with risk assets generally outperforming traditional safe havens. The US and Chinese authorities moved closer to agreeing a partial deal on trade, while the UK once again edged back from the precipice of a no-deal Brexit. Global central banks reiterated their dovish stances and […]

Weekly Market Update: Stocks trade higher on US jobs numbers, Sterling gains versus Dollar and Euro

Read our full Market Update Market Update A second straight week of strong performance for Sterling, up +1.7% vs the US Dollar and +1.2% vs the Euro as markets further priced in a Conservative victory at the coming General Election, once again mean that although global stocks were up in local terms, UK investors experienced […]

Weekly Market Update: Stocks rebound as US-Iran fears fade

Read our full Market Update Market Update Global stocks were up +0.8% last week, recovering part of the losses observed after the US-Iran conflict sent investors fleeing from risk assets; tensions have however faded slightly, and it appears that a solution may be reached that does not involve further military intervention. The best performing region […]

Mazars Wealth Management Investment Newsletter – Winter 2020

Read our full MWM Investment Newsletter Winter 2020 Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7%. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservatives’ decisive general election victory. The late final rally was […]

Weekly Market Update: Oil and stocks sell-off on coronavirus fears

Read our full Market Update Week 4 Market Update Equities closed the week lower as an outbreak of the coronavirus in China made global headlines. Global stocks fell -0.8% in local terms, which translated into -1.2% in Sterling terms. UK markets fell -1.2% with Financials and Energy the worst performers. Oil has been particularly affected […]

Weekly Market Update: Stocks hit record highs on earnings data, bond yields rise

Read our full Market Update Week 6 Market Update Global stocks saw strong gains last week, returning +2.7% in local currency terms and +5.0% in Sterling terms after the Pound depreciated versus most major currencies. The rally was driven by hopes that coronavirus fears had been overstated and US earnings coming in ahead of expectations. […]

Weekly Market Update: Stocks Steady on US Earnings Growth

Market Update Despite concerns about coronavirus continuing to dominate headlines, markets on the whole edged up last week, with global equities gaining +1.2% in local terms, which translated into a +0.1% gain for UK investors. The resignation of UK Chancellor Sajid Javid saw Sterling rise along with gilt yields. Javid’s replacement, Rishi Sunak, is expected […]

Q1 Quarterly Investment Outlook: 2020: The Power of the Cycle

Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7% in local currency terms. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservative’s decisive general election victory. The late final rally was primarily driven by renewed optimism for a ‘phase one’ trade deal between the US and China, and left global equities up 25% for the year. It is of course important to note that, by contrast, markets ended 2018 in very pessimistic mood as the Fed continued to raise interest rates, and therefore a global equity return figure of around 8% from September 2018 is a more useful measure of equity returns.

Weekly Market Update: Stocks decline on COVID-19 fears, Bonds and Gold rally

Read our full Market Update Week 8 Market Update Fears that COVID-19 could weigh on consumption and global growth increased last week as the number of cases spiked in both Iran and Italy. Concerns that the virus could impact critical global supply chains have increased, with tech titan Apple widening their earnings estimates given the […]

US 10 Year Yield at all time low in response to Coronavirus fears

Download our Full Market Update here Market Update Global stocks saw a sharp sell-off last week after COVID-19 cases spiked in Italy, Iran and South Korea, pushing recession fears higher and expected corporate earnings lower for 2020. Global stocks fell -9.4% in Sterling terms, with US equities experiencing the quickest correction since the Great Depression, […]

Weekly Market Update: Stock markets suffer record daily falls, central banks cut interest rates to combat coronavirus induced slowdown

Read our full Market Update Week 11 Market Update UK equities were down over 8% this morning, with the FTSE 100 down -32% over the last month as markets are now starting to price in a coronavirus induced global recession. Oil prices continued to slip, down nearly 50% YTD in USD terms. This fall has […]

Why it pays to be a long term investor

Please read the full article here: In the current investment climate where central bank activity and algorithmic trading strategies are two primary driving forces of asset prices, enabling rapid losses and even faster gains as momentum funds then push winners higher and losers lower, we are reminded how important it is to follow a long […]

Weekly Market Update: Fiscal stimulus plans revive global equities, bond yields fall on additional QE measures

Read our full Market Update Stock markets ended their losing streak with many major indices posting their largest daily gains since 1933, or indeed for many on record, on the Tuesday of last week. Reasons for the rally include investors rebalancing multi-asset portfolios, short positions being covered and the US fiscal strategy offering downside protection […]

WEEKLY MARKET UPDATE: A MORE SANGUINE WEEK FOR MARKETS

By regular standards it was a rocky week for equities, which rallied 2-3% in the first few days, but fell 4-5% later on. However in comparison to preceding weeks market moves were somewhat muted, perhaps because the news-flow has provided little further clarity as to the time-scale and magnitude of the COVID-19 crisis – markets […]

WEEKLY MARKET UPDATE: IS THIS RALLY A “HEAD FAKE”?

Last week (Friday 3 to Monday 13 April) global stocks rose on the back of an improved narrative regarding the Coronavirus pandemic, as markets see a ‘flattening of the curves’ and a reduced pace of new infections, while many countries weigh reopening their economies. Boris Johnson’s survival helped improve the narrative both for the UK […]

Weekly Market Update: Nobody Wants Your Oil

Aside from UK equities, major equity market regions were positive in local currencies, boosted on Friday by reports that suggested a drug had shown positive results against COVID-19 in a clinical trial, as well as some relaxing, both planned and enacted, of restrictions in several countries. Sterling strength meant that some returns for UK investors […]

WEEKLY MARKET UPDATE: US-CHINA RHETORIC UNNERVES MARKETS

Markets rallied throughout last week, however US equities closed lower on Friday and down -1.6% in Sterling terms for the week, with other regions following suit this morning, on concerns that tensions between the US and China could escalate due to accusations from the US administration over the origins of the Coronavirus. For the week, […]

WEEKLY MARKET UPDATE: EASING OF LOCKDOWN RESTRICTIONS BOOSTS EQUITIES

Equity markets continued to steadily recover last week, with all regions positive or flat in Sterling terms and only Emerging Market Equities down in local terms. Markets have been reacting positively to the gradual opening up of economies across the world, even with some signs that the Coronavirus is re-emerging in areas such as Wuhan […]

WEEKLY MARKET UPDATE: EQUITY STRENGTH DESPITE WEAK DATA

Hopes for a COVID-19 vaccine saw equity markets rally across the board last week, with global stocks up +2.8% in Sterling terms and +3.2% in local terms. EU equities led the way in Sterling terms, up +4.1%, with UK equities also experiencing strong returns of +3.4%. US equities gained +2.8%, although Emerging Market equities were […]

Weekly Market Update: Equity Momentum Continues

For a second week in a row it was green across the board for equities, as global stocks gained +2.4% in Sterling terms and +3.7% in local terms. European stocks were amongst the best performers for a second week, with Japanese equities performing equally well. Early in the week markets focused on the US returning […]

WEEKLY MARKET UPDATE: UPBEAT US JOBS FIGURES BOOST EQUITIES

Equities saw a third straight week of strong returns, with Japan the only region experiencing losses in Sterling terms (down -1.6%), although it was also positive in local terms (up +3.1%). US ADP National Employment figures showed fewer job losses, causing an initial spike in equities, which continued later in the week as it was […]

WEEKLY MARKET UPDATE: Markets fall on second wave fears, gloomy Fed

Read our full Market Update Market Update The rally in risk assets came to a grinding halt last week on fears of a second wave of infections in the US, with virus rates up in many states, and the Federal Reserve offering up a gloomy economic outlook. Stocks are also down this morning on news […]

Weekly Market Update: Stocks climb on promising economic data

Read our full Market Update Market Update Stock markets rebounded last week, posting gains in both local currency and Sterling terms, with news that the Fed will be expanding its corporate bond buying programme sending stocks higher. The move from ETF purchases to individual bond issues by the Fed has been viewed as a significant […]

Weekly Market Update: Stocks sell-off on COVID-19 second wave fears

Read our full Market Update Market Update Stock markets closed down last week on the back of a COVID-19 case count resurgence. Growth stocks outperformed value stocks as fears of a second wave of the virus caused market participants to raise their expectations of a second lockdown. Banking stocks were particularly volatile as news that […]

Weekly Market Update: Technology stocks push equity markets higher

Please read our full Market Update Market Update Stock markets closed up last week, with the technology-heavy NASDAQ 100 even reaching an all-time high. Cyclical sectors such as Oil and Financials lagged as economic conditions remain weak and second wave fears continue to build, with increased use of local lockdowns. The rally in risk assets […]

Weekly Market Overview – US Dollar slide sees negative equity returns for UK investors

Global equities were mostly positive in local terms last week, however a fall in the US Dollar, combined with Sterling appreciating, meant that returns for UK investors were generally negative. Weak US Dollar performance was largely due to a statement at Davos by US Treasury Secretary Steve Mnuchin being interpreted as suggesting that the US […]

Comments