Is gold a good hedge against inflation?

Uncategorised

Is gold a good hedge against inflation?

Thu 10 Jun 2021

Investors and consumers have spent the past two months inundated with news about resurging inflation. Any investor playbook worth its salt would almost instantaneously overweight gold in times of higher inflation. In theory, this should work. Inflation is supposed to be a consequence of excess money in the economy. People have more to spend, demand is higher and, with supply unchanged, prices go up. The antidote to excessive money is higher rates, which curb lending and restrict money creation. Until the new equilibrium takes place, consumers, the theory says, should rely on a more tangible asset to maintain wealth.

Throughout history, humanity has experimented with many tangible stores of wealth. From livestock and land to more exotic forms of ‘money’ such as knives (Zhou China), dolphin teeth (Solomon Islands), salt (Roman Empire), squirrel pelts (Russia) and seashells (North America). Desperate from the hyper-inflation in the early 1920’s, Germans used actual wooden money called ‘Notgelds’. However, since the Palaeolithic period, c 40,000 BC, 33 millennia before the appearance of the first cities, no asset has been a more reliable store of wealth than gold.

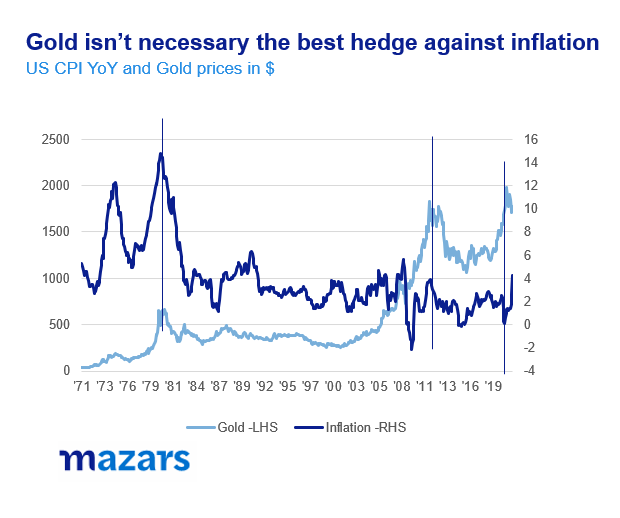

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise. In quiet inflationary periods gold prices rise and fall as a result of other fundamentals, such as central bank behaviour, investor and consumer demand. Additionally, its historical patterns were unequivocally affected after the introduction of Gold ETFs in the early ‘00s which made it more accessible to everyday investors who can now buy it without having to pay the transaction costs associated with buying gold from central banks or directly from exchanges.

A simple calculation from 1971 suggests a very small positive correlation (13%) between returns of gold and changes in US inflation. From 1986 to 1990, US consumer inflation rose from 1.1% to 6.3%. In the same period, gold lost 4% of its value.

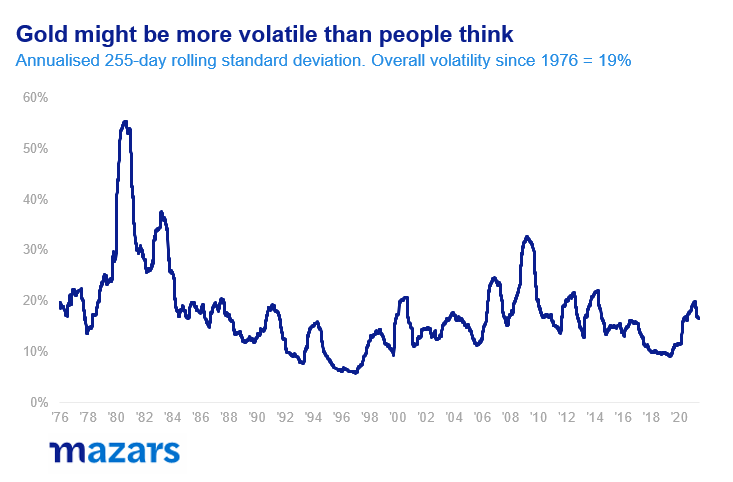

Its volatility may also surprise some investors. Annualised rolling 255-day standard deviation (a common measure of volatility) since 1976 is 19%, above that of equities (13%) and bonds (around 5%-7%).

Having said that, correlations between gold and inflation tend to increase sharply in more acute inflationary episodes, like in 1981 and 2011. Does 2021 qualify as such an episode? We believe so, as numbers suggest the highest inflation figures in a decade with some uncertainty going forward as to whether it will continue.

Investors, however, should be mindful that while correlation increases during the acute phase, it tends to decrease dramatically as inflation decelerates. Currently, central banks are not expecting a long-term bout of inflation. By historical standards this could mean some de-correlation soon.

In terms of inflation, gold can be a good trade if someone predicts inflation in advance. However, buying and holding after the event may not be as successful.

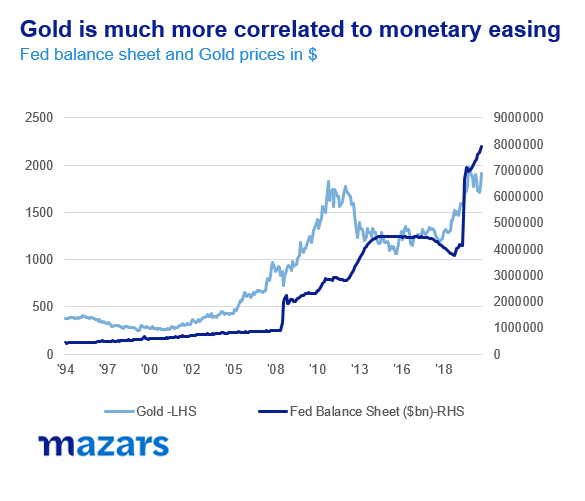

If anything, gold has proven itself to be a more effective hedge against the enormous sums being printed by central banks in reason times. The correlation between gold prices and the size of the Fed’s balance sheet is nearly 87%.

Gold prices involve central bank demand, quirky consumer preferences which different around the globe, speculation and investment heuristics. Instead of trying to time this extremely complex market with many different players, investors should consider gold as part of a wider long-term portfolio, to take advantage of all the reasons other would buy it and to protect some of their assets against unexpected changes in the inflation expectations of others.

Inflation momentum will recede. But prices may remain elevated.

There’s a strong possibility we may see the end of the episode soon. But supply chains could take long to mend and overall price levels could remain elevated versus pre-pandemic numbers.

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

European Risks Primer: Richlandia and Poorlandia

The article was originally published in the Money Observer on the 20th July 2018 The potential breakup of the Euro has been a permanently armed grenade under the bed of the global economy for almost two decades. The recent Italian elections driving yields up and the Euro down reminded allocators that European risks have never […]

Tinker, Tailor, Soldier… Huawei?

This is a multi-level chess game, touching politics, intelligence and trade, and a move in each field directly affects the other two.

Weekly Market Update: Bond yields rise, gold price declines

Read our full Market Update Week 45 Market Update Global stocks rose +0.8% in local currency terms and +2.1% in Sterling terms in yet another positive week for risk assets. Meanwhile yields rose sharply and Gold had its worst week in three years as there was a flight from defensive assets. In Sterling terms US […]

Q4 2019 Quarterly Outlook

Read our full MFP Quarterly Investment Outlook Q4 Ghosts of Japan Growth has been consistently slowing across the globe. In the past two issues, we dealt with the impact of China’s slowdown, as the world’s marginal buyer goes through the necessary pains of transformation and the impact of elongated cycles on growth. In this outlook […]

Weekly Market Update: Global stocks fall as economic data disappoints

Read our full Market Update Week 40 Global stock markets fell throughout the week, both in local currency terms and Sterling terms. UK assets led the decline, down -3.5% on the news of weaker economic data out from the services industry. US stocks were down up -0.4% in Sterling terms, with similar returns observed in local […]

Monthly Market Update – December 2018

Read our full Monthly Market Update December 2018 November data indicated that the global economy continues to slow, despite a pick up in the services sector, as trade conditions deteriorate. Risk asset divergence, a theme of the previous quarter, seems to have abated, as US risk asset underperformance closed part of the gap with Europe and […]

Angela’s long goodbye and what it means for investors

When Angela Dorothea Merkel became president of her party, the CDU, in 2000, her sights were set on the highest echelons of leadership in Germany. In 2005, she followed Helmut Kohl, her mentor, and Gerhard Schroder by becoming the third post-war leader of a united Germany. Furthermore, she was the the first who grew up […]

Monthly Market Update – October 2018

Read our full Monthly Market Update October 2018 September data continued to indicate global economic and risk asset divergence, consistent with a mature economic cycle, with USD assets rising as a result of Mr. Trump’s policies. The global economy is also diverging, with the US on a faster expansion path, while Europe and EM are […]

How British retailers “gamed” themselves into a corner

When my daughter was first born she had trouble sleeping and hated her cradle. So I used to hold her by to the kitchen fan (new parents take note, this works!) for about 10’, until she was fast asleep. It worked magic every time. Until it didn’t. A few weeks later she didn’t like it […]

Quarterly Investment Outlook: Is Globalisation Going in Reverse?

Globalisation is not inherently “good” or “bad”. It is the natural historic evolution of the nation-state, made possible by the internet and the potency of capitalism. But is it over?

Monthly Market Update: Markets unable to break out

Read our full Monthly Blueprint July 2018 Month In Review On the face of it, June has not been an exciting month for risk assets. Developed market stocks ended the month roughly in the same place as they started it, while long bond yields were little changed. However, beginning and end figures mask not only […]

Investing, “in the time of Cholera”

We can comfortably use a phrase that, under other circumstances, would surely risk bringing upon us financial anathema: “This time is different”.

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

Macro of the Week – Fed hikes rates, more expected

As widely expected the FOMC raised the Fed Funds Rate target by 0.25% to a range of 1.5% – 1.75%, in what was a unanimous decision by the committee. It was the sixth rate hike since the GFC as the central bank looks to ‘normalise’ interest rate policy and was the first major decision under […]

Macro of the Week – UK GDP slowing

The UK economy grew more slowly than previously estimated in Q4 2017, increasing by 0.4% quarter-on-quarter according to the second estimate by the ONS. This figure was a 0.1% downgrade from the original estimate. The downward revision was due to slower […]

Macroeconomic View – French unemployment down

French ILO unemployment dropped unexpectedly from 9.6% to 8.9%. It was further proof of the strength in the French, and subsequently, the European economy. European equities lost 1.5% briefly after the US inflation report was released, with figures higher than expected. The market recovered, but the move is indicative of the factors that affect traders. […]

Market Comment – Mind the earnings

Traders were worried again last week, as US inflation figures came in higher than expected, suggesting the possibility of steep interest rate hikes. With heightened volatility, a very good US earnings quarter went almost unnoticed. With the reporting season almost over, 75% of companies beat earnings estimates and 78% beat sales estimates. This is the […]

Macroeconomic View – German exports accelerating

German exports were weak for the month, up only 0.3%, but are still accelerating year-on-year. Chinese exports were stable, but imports picked up significantly, offsetting last month’s weak data. UK The Markit Services PMI dropped slightly to 53 from 54.2. The Halifax House Price Index year-on-year for the 3 months to January fell from 2.7% […]

Macro of the Week – US wages accelerate

US hiring picked up in January and wages rose at the fastest pace since the GFC. Hourly earnings increased 0.3%, resulting in an unexpected year-on-year increase of 2.9%, up from 2.7% in December (which was also revised up from 2.5%). This was on the back of a nonfarm payrolls increase of 200k, which was upwardly […]

The difference between a skirmish and a (trade) war

Why geopolitics now matter more In the past few years, investors and economies have grown somewhat insensitive to geopolitical surprises. Brexit, for example, did not cause the massive initial shock to either the economy or the stock markets that many analysts had predicted. Neither did Mr. Trump, whose election has sent stocks soaring by more […]

WEEKLY MARKET UPDATE: SECOND WAVE FEARS SEE MARKET JITTERS

Equity markets sold off across the board last week, declining initially amid fears of a secondary wave of infections and a pessimistic outlook from the Fed, although there was a sharp recovery later in the week on additional stimulus expectations. In local terms global equities fell -2.5%. However due to Sterling weakness, in part due […]

Weekly Market Update: Fiscal stimulus plans revive global equities, bond yields fall on additional QE measures

Read our full Market Update Stock markets ended their losing streak with many major indices posting their largest daily gains since 1933, or indeed for many on record, on the Tuesday of last week. Reasons for the rally include investors rebalancing multi-asset portfolios, short positions being covered and the US fiscal strategy offering downside protection […]

Weekly Market Update: US Inflation Unnerves Equity Markets

Global economies are reopening, and moving into the recovery phase, this pickup in activity has lead investors to question the potential impact on inflation. Investors are cautious of whether inflationary effects will be transitory or long-lasting. The US inflation reading unnerved markets and all major equity markets fell last week. US equities fell -2.2% in Sterling terms, partly driven by currency effects, markets had sold off sharply at the start of the week before recovering in the latter half. UK equities, which typically move inversely to Sterling, due to high levels of overseas earnings, fell -1.2%. Japanese equities fared worst last week, caught in global equity volatility and increased lockdowns, falling -4.0% last week. Despite strong Chinese equity performance, emerging market equities fell -3.8% in Sterling terms. The US 10Y yield rose 5.1bps to 1.6%, while the UK 10Y rose 8.2bps to 0.9%. Both gold and oil were nearly unchanged, falling -0.2% and -0.1% on the week respectively.

It’s the worst start in 20 years. Here’s why investors should feel fine.

The worst start to the year inn 20 years leaves investors confused. Here's why we are more relaxed about it.

Investing in a world without QE

Inflation rising may upend a 12-year investment paradigm. Is there life after Quantitative Easing?

Weekly Market Update: Inflationary pressures may be moderating. Supply chain pressures aren’t.

Equities in most major markets posted losses last week with global stocks down -0.4% in Sterling terms, as inflation concerns, supply chain issues and rising coronavirus cases dampened investor sentiment. US stocks were up +0.1% with growth stocks exhibiting solid gains, outweighing the losses in more cyclical firms. European stocks were down -1.8%, as countries within the region started imposing restrictions to curb rising Covid-19 cases. UK stocks were down -1.6% amid CPI inflation figures hitting a ten-year high, while EM equities fell by -1.7%. The US 10Y Treasury yield was down 2.2bps finishing the week at 1.548%, while the UK 10Y yield was down 3.5bps reaching 0.880%. In US Dollar terms gold lost some of its previous weeks’ gains, down -1.3%, while oil was heavily down -6.2% to $76 per barrel.

Weekly Market Update: Operations Managers are the new economists

Equities in most major markets posted minor gains last week with global stocks up +0.3% in Sterling terms, as inflation concerns seem to have stemmed a previously strong investor sentiment. US stocks were up +0.2% as multi-year high inflation data offset positive news on employment data. EU stocks were up +0.2%, despite Covid-19 cases surging in most countries in the region. UK stocks were up +0.7% while EM equities rose by +2.2%, driven by China’s announcement that it would propose easing measures to aid indebted real estate firms. The US 10Y Treasury yield was up 11.0bps finishing the week at 1.561%, while the UK 10Y yield was up 6.9bps reaching 0.914%. In US Dollar terms gold posted solid gains for the second week in a row, up +3.1%, while oil was down -0.1% to $80.4 per barrel.

Quarterly Update: Will the Post-Covid Labour Market ever be the same?

'Work' may never be the same after the pandemic. How might things play out? What do businesses need to know to prepare? Read our quarterly economic update

Weekly Market Update: Port congestion isn’t dealt with interest rate hikes

Equities in most major markets edged higher last week, partly offsetting the previous week’s losses, with global stocks up +0.3% in GBP terms. US stocks were up +0.4% despite the disappointing jobs report published on Friday. European stocks were up +0.2% amid high volatility while UK stocks were up +1.0% despite the BoE’s new Chief Economist raising the alarms on inflation’s persistence in the coming months. Globally, energy stocks outperformed all sectors for a fifth week in a row, posting solid gains of +4.9%, followed by financials, utilities and materials. The US 10Y Treasury yield was up 15.0bps, finishing the week at 1.612%, while the UK 10Y yield was up 15.6bps reaching 1.158%. Sterling rose by +0.5% against the US Dollar. In USD terms gold pulled back by -0.6%, while oil was up by +4.1%, reaching $81 per barrel.

The UK’s energy market and its broader implications

Much of the recent news in the UK has been devoted to the spike in household energy costs and the potential collapse of the number of providers in that market from around 50 to 10 by the end of winter. In fact, since writing this first draft of this piece 2 providers have gone bust, leaving more than 800,000 customers without a provider. Of itself this is an interesting topic: it seems remarkable that rising wholesale gas prices can rupture the UK energy market and reduce the number of energy providers by 80%. For us the more relevant question relates to the wider economy and how energy costs can impact consumer demand and inflation, which contributes to our discussions when deciding asset allocation. This blog post aims to explore the former and explain the Mazars Investment Team thinking on the latter.

Quarterly Outlook: An investor’s inflation and growth playbook

Investing during the past twelve years has been underpinned by a basic principle: market participants have been encouraged to take risks, mainly to offset the trust shock that came with the 2008 financial crisis (GFC). Each time equity prices have fallen significantly, the Federal Reserve, the world’s de facto central bank, would suggest an increase in money printing, or actually go ahead with it if volatility persisted. Bond prices, meanwhile, kept going up, as central banks and pension funds were all too happy to relieve private investors of their bond holdings even at negative yields. Market risk was all but underwritten.

Will the rotation into value continue?

While it remains to be seen how long value leadership will last, many of the drivers that led investors to flock to growth stocks have reversed and now favour value stocks.

Monthly Market Blueprint June 2020

The “right” fundamentals Often the first thing we are taught about something, especially if it comes from someone with authority, like a parent, a teacher or our experienced financial adviser, is taken as a “fundamental” truth. In psychology, this is called the “primacy effect”. Any other “truths” that contradict or seek to modify that first […]

Weekly Market Update: The Yield, Not “Inflation” Will Determine the Rotation

Equity market gains early last week were, broadly speaking, eroded as bond yields continued to rise, reaching one-year highs. Amid falling oil prices and rising political uncertainty caused by potential bans on vaccine exports coming out of the EU, many major equity markets fell last week. US equities fell -0.5% from record highs in Sterling terms, despite the country surpassing 100 million vaccinations on Friday. UK equities fell -0.7%, now down -2.4% from their 52-week highs in January. Globally the best performing sector was healthcare, whilst energy, due to oil prices, was the worst performing. Japanese equities rose +3.6% and are the best performing major equity markets this year. The US 10Y yield continued its rise up 9.6bps to 1.7%, while the UK 10Y rose 1.6bps to 0.8%. Gold rose +1.3% on the week. Oil has seen back-to-back weekly declines, down -6.1% to $61.2 a barrel, due to a glut of supply and weakening demand forecasts.

Weekly Market Update: Investors dilemma: Cheaper bonds or returning dividends?

Markets returned to positive territory this week, supported in part by progress on the Biden stimulus bill. However, chair of the Federal Reserve Jerome Powell’s speech, with a lack of updates to current policy, disappointed investors leading to a sell-off on Thursday afternoon. US equities rose +1.7% in Sterling terms. UK equities rose +2.5%, with UK equity markets benefiting from rising oil prices. Emerging Markets grew +0.9% in Sterling terms, although this was a more moderate +0.1% in local currency terms. Globally the best performing sector was Energy, whilst IT was the worst performing, as the rising yield environment impacted valuations. Japanese equities rose +1.0%. The US 10Y yield continued its rise, up 16.1 bps to 1.6%, while the UK 10Y fell 6.4bps to 0.8%. Gold fell -1.1% on the week. Oil rose sharply, up +8.4% on the week to $66.5 following the OPEC meeting where it was decided to hold production at current levels, when a rise in production had been anticipated.

Weekly Market Update: Bonds Sell Off Spills Over to Wider Market

A significant rise in US Treasury yields unsettled markets last week. US equities fell -1.9% in Sterling terms, with Tech stocks suffering their worst week in nearly six months. UK equities fell -1.9%, with Energy and Financials the only two positive sectors for the week. Emerging Markets suffered the greatest sell-off, having led global equity markets so far this year. UK and Emerging Markets are the only major equity markets still positive for the year in Sterling terms. Globally the only positive sector was Energy which was supported by rising oil prices. Investors will keep a keen eye on the OPEC+ meeting this week for any indication of increased oil supply. Japanese equities fell -2.4% in Sterling terms, the worst performing region year-to-date for UK investors. The US 10Y yield continued its rise, up 6.9 bps to 1.4%, at one point hitting 1.6%, and the UK 10Y rose 12.2 bps to 0.8%. Long-term yields are now trading at their highest level since the pandemic. Gold fell -2.3% on the week, while Oil rose +4.4% to $62.7.

Weekly Market Update: Markets Rally for Second Week as Inflation Expectations Return

Global equities continued last week’s gains, rising +0.7% in Sterling terms. UK equities, amongst the top performing major markets, rose by +1.6%. They were supported by rising oil prices and positive returns from energy companies, as the domestic market is overweight to the Energy sector. European equities, amid high volatility, were up +0.8%, due to improved coronavirus infection rates and hopes of a large U.S. economic stimulus. US equities rose +0.4%, the worst performing major region. Globally, Energy was the best performing sector whilst Utilities and Cons. Discretionary were the only sectors to finish the week down. Emerging Markets maintained their strong performance since the start of the year, posting gains of +1.5%. Sterling rose +0.8% and +0.3% against the US Dollar and Euro respectively, continuing its strengthening trend this year. The US 10Y yield rose 4.5bps to 1.2% and the UK 10Y rose 3.5bps to 0.52%. Gold fell -2.0% on the week, while Oil rose +3.7%.

Quarterly Outlook: Beyond Covid

The persistent dichotomy between stock market performance and economic performance has been a particularly hard puzzle for investors. While it is very clear that the previous 12-year economic cycle has undoubtedly come at an end, the financial cycle, thanks to central banks, has survived a five standard-deviation event (1 in 3.5 million probability), and continues unabated. With the global economy in turmoil, can stock and bonds be trusted to create or even maintain wealth?

Weekly Market Update: Flexible Federal Reserve Sends Cable and Yields Higher

Read our full Market Update Market Update US equities climbed +1.4% last week with, major indices setting new record highs, as US Federal Reserve Chairman Jerome Powell announced a shift in how the Fed views inflation, saying it won’t increase interest rates to respond to low unemployment levels and also won’t worry as much about […]

Weekly Market Update: Equity Markets Rebound, Gold continues to soar

Read our Full Market Update Market Update Bucking the trend of two consecutive weeks of falling equity markets, all major indices were positive last week. Global equities gained +2.7% in Sterling terms, with the Nasdaq Composite reaching new highs, and the S&P 500 now close to its February peak. After a poor week last week, […]

Quarterly Investment Outlook Q3 2020: Covid Recovery and Anxiety

A quarterly report is not normally a difficult document to put together. Usually it consists of an account of the trending state of affairs, the more possible outcomes and risks to those outcomes. In the past few years, these reports were actually made easier. The US Federal Reserve was underwriting risk at such an unprecedented scale, nearly unwavering for more than a decade, in a manner which suppressed all major hazards to the economy and financial markets. Ever since 2010 the question, repeatedly, had been: “With opportunity costs driven down so much for so long, whatever can bring markets down?”

Market Comment – Macro headwinds

Last year was very positive, both in terms of stock market and macroeconomic volatility (the volatility of macroeconomic releases). In recent weeks, however, we have noticed a deterioration in macroeconomic releases, especially in the US. Lower inventories and higher imports took a toll on GDP. More detailed data on capital expenditure also shows weakness in […]

Comments