It's the worst start in 20 years. Here's why investors should feel fine.

Market Updates

It’s the worst start in 20 years. Here’s why investors should feel fine.

Tue 25 Jan 2022

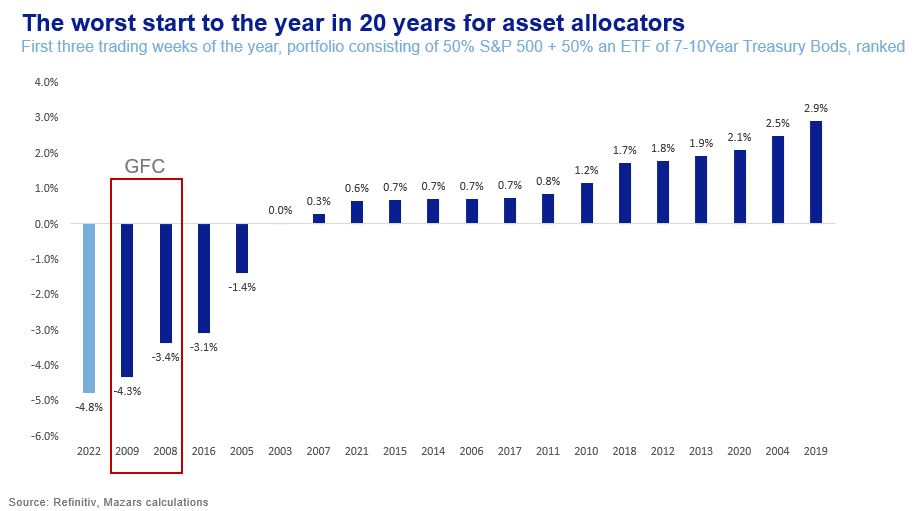

Entering their fourth week, financial markets have had the worst start in 20 years. A 50% Equity/ 50% Bond portfolio in the US, the world’s biggest market, has now lost nearly 5%, more even than it did during the 2008-2009 Global Financial Crisis.

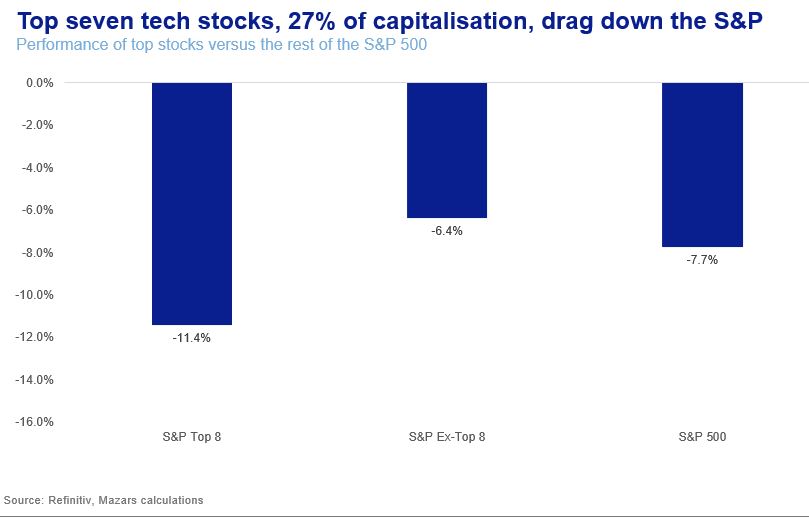

A lot of analysts cite that the retrenchment is really a growth-to-value rotation. Tempting as it may sound blaming big tech valuations, the truth is slightly more complex. The S&P 500 has lost 7.7% since the end of 2021. Excluding the top seven big tech stocks (Apple, Microsoft, Amazon, Google, Meta, Tesla, Nvidia), the rest of the world’s leading index is still down 6.4% for the year, which would individually constitute the fifth-worst opening since 1971.

It’s the end of the world as we know it…

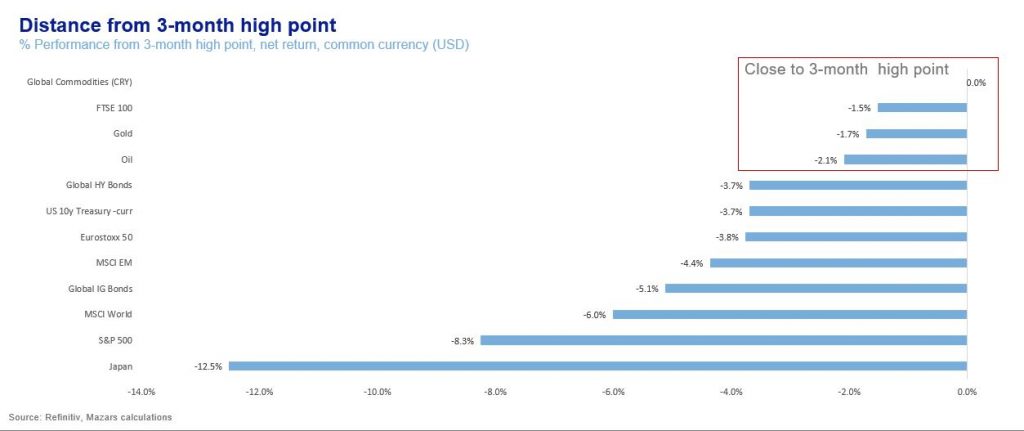

Ostensibly, the world has turned on its head. Global High Yield are outperforming US Treasuries during a sharp downturn and the FTSE 100 is outperforming all major global equities. What in fact is happening is a rotation out of some of the most overvalued securities, plus those who rallied near the end of last year, like Japan. This is a direct result of a more hawkish Fed, putting Quantitative Easing, the driving force behind asset prices for over a decade, into hiatus.

The ebb leaves those vessels forgotten by the rising tide unscathed, simply because investors have poured less fast money in them and don’t have as much to pull out. Thus, the FTSE 100 and Emerging Markets seem to be doing better than the rest of the equity world. Global High Yield have lost nearly as much as the US 10-year treasury, the bedrock asset of global allocators. Commodities also staying afloat are more a result of 40-year high inflation and rising geopolitical tensions.

The end of Quantitative Easing and the visible beginning of quantitative tightening, without the mitigating factor of a roaring economy are certainly enough to explain the ghastly experience investors have had since the beginning of the year.

…And I feel fine…

The fact that the state of the market can be fully explained, however, does not in itself give comfort. However, we believe long-term investors should not necessarily feel (too) anxious for two reasons: Ample liquidity and a receding pandemic.

We don’t really need the Fed

The Federal Reserve’s Quantitative Easing has served to heal collective trauma after the near-collapse of capitalism in 2008. When the ECB embraced the process, it managed to keep the Euro together after 2012. After more than a decade, however, investors noticed that the economic benefits, save from staving off financial collapse, have been minimal. If anything, persistent QE exacerbated global income and wealth inequalities to a political boiling point. From a financial asset standpoint, since 2008, major global central banks have added nearly $23tn in global financial markets. The number is formidable, but market capitalisation has increased by a lot more than that, nearly $43tn for equities and $73tn for bonds.

Residual liquidity is still plenty, and many are waiting to buy at better prices (and lower volatility). US corporates (ex-banks) have a record $3.3tn in their balance sheets to buy back their own shares. The top eight companies alone have more than half a trillion to spend. An expected 22% rise in earnings for Q4 should only be helpful. US households have a record 95% deposit- to-income ratio. They can afford to keep their pension accounts intact and add more at lower levels. Global Private Equity is sitting on nearly $2tn of dry powder. This unspent capital was not waiting for higher bank rates. It was waiting for more attractive valuations. And let us not forget the $1.6tn of just public money earmarked for ‘Green’ investments.

With inflation running above 5%, seasoned investors and corporates can ill-afford cash stockpiles. Simply put, there’s a lot of liquidity and powerful incentives for money to be put to work at lower prices. Central banks QE served as a reminder that powerful organisations will be buyers of the last resort, but institutional and individual investors have poured a lot more money into markets. And let us not forget that while central banks (ex-EU) are decidedly more hawkish, they do remain buyers of the last resort. Just not at the first sign of trouble. This is what letting the markets mature and overcome trauma would look like. The fact that central banks were forced to stop spoon-feeding markets due to inflation tells a story more about an overprotective parent than a needy child.

The pandemic may well be improving

Rising volatility has obscured the fact that, fundamentally, we are looking at the increasing possibility of pandemic economic disruptions ending sooner than anticipated. The Omicron variant peaked for a lot of the world almost simultaneously, which in and by itself should help re-harmonise some parts of the global value chain. The potential for the highly-transmissive but milder variant to remain dominant, coupled with higher vaccination rates and Covid-targeted medication in the pipeline, have left an increasing amount of analysts more optimistic that disruptive policy responses, like lockdowns, may become a thing of the past. Q1 economic performance may well be worst than originally expected, but the probability of a faster economic rebound thereafter is increasing. The problem for markets is that no one can be sure that we are indeed dealing with the final Covid-19 dominant variant. Therefore, an upside scenario hasn’t been priced in.

What it all means for investors

We believe that we are experiencing a Fed-driven asset rerating, not an existential threat to capitalism. If it holds true, then at the end of the process lie opportunities. With global stocks down 6% from their recent peak, we don’t have any evidence to say that we have seen the end of this correction. It could well last longer and go much deeper. Opportunistic retail buying has been rampant over the past two years and it looks like there is more to be shaken off. But we also see a lot of capital waiting for more attractive prices. More evidence that the pandemic may be near its end and an eventual plateauing of inflation pressures could be just the triggers global asset allocators are looking for to re-position at lower prices.

The outlier risk

We think that a key risk right now is geopolitical. The Crimean War (1853-1856) marked the rapid decline of the Ottoman and Russian empires, while consolidating Britain’s status as the global military superpower for decades. The same area is once again the focus of global powers. Tensions have been rising fast between the US, Russia and China. Further escalation could have unforeseen consequences for markets, especially commodities. Situations like this usually come down to last-minute decisions and/or deals, and there’s precious little investors can do, other than quickly recognise a change in the status quo when and if that happens.

Monthly Market Update – October 2018

Read our full Monthly Market Update October 2018 September data continued to indicate global economic and risk asset divergence, consistent with a mature economic cycle, with USD assets rising as a result of Mr. Trump’s policies. The global economy is also diverging, with the US on a faster expansion path, while Europe and EM are […]

Monthly Market Update – December 2018

Read our full Monthly Market Update December 2018 November data indicated that the global economy continues to slow, despite a pick up in the services sector, as trade conditions deteriorate. Risk asset divergence, a theme of the previous quarter, seems to have abated, as US risk asset underperformance closed part of the gap with Europe and […]

WEEKLY MARKET UPDATE: SECOND WAVE FEARS SEE MARKET JITTERS

Equity markets sold off across the board last week, declining initially amid fears of a secondary wave of infections and a pessimistic outlook from the Fed, although there was a sharp recovery later in the week on additional stimulus expectations. In local terms global equities fell -2.5%. However due to Sterling weakness, in part due […]

WEEKLY MARKET UPDATE: EQUITY STRENGTH DESPITE WEAK DATA

Hopes for a COVID-19 vaccine saw equity markets rally across the board last week, with global stocks up +2.8% in Sterling terms and +3.2% in local terms. EU equities led the way in Sterling terms, up +4.1%, with UK equities also experiencing strong returns of +3.4%. US equities gained +2.8%, although Emerging Market equities were […]

Weekly Market Update: Nobody Wants Your Oil

Aside from UK equities, major equity market regions were positive in local currencies, boosted on Friday by reports that suggested a drug had shown positive results against COVID-19 in a clinical trial, as well as some relaxing, both planned and enacted, of restrictions in several countries. Sterling strength meant that some returns for UK investors […]

How British retailers “gamed” themselves into a corner

When my daughter was first born she had trouble sleeping and hated her cradle. So I used to hold her by to the kitchen fan (new parents take note, this works!) for about 10’, until she was fast asleep. It worked magic every time. Until it didn’t. A few weeks later she didn’t like it […]

Weekly Market Update: Markets fall after record low US GDP data

Read our full Market Update Week 31 Market Update Major indices closed down for a second week running, with investors reacting to a flood of quarterly earnings reports and some prominent economic data. US corporate earnings were in the spotlight during the week, with tech giants Facebook, Amazon, Apple, and Alphabet reporting mostly healthy gains […]

Monthly Market Update: Positive markets and slow recovery

For the better part of the last three years the core of our investment policy has been simple: “Don’t fight the Fed”. As accomplished economist Mohammed El-Erian put it, Quantitative Easing is not the biggest game in town, it is rather the only game in town. Prices for risk assets are almost completely dependent on […]

Weekly Market Update: Oil and stocks sell-off on coronavirus fears

Read our full Market Update Week 4 Market Update Equities closed the week lower as an outbreak of the coronavirus in China made global headlines. Global stocks fell -0.8% in local terms, which translated into -1.2% in Sterling terms. UK markets fell -1.2% with Financials and Energy the worst performers. Oil has been particularly affected […]

Weekly Market Update: Stocks Steady on US Earnings Growth

Market Update Despite concerns about coronavirus continuing to dominate headlines, markets on the whole edged up last week, with global equities gaining +1.2% in local terms, which translated into a +0.1% gain for UK investors. The resignation of UK Chancellor Sajid Javid saw Sterling rise along with gilt yields. Javid’s replacement, Rishi Sunak, is expected […]

WEEKLY MARKET UPDATE: EASING OF LOCKDOWN RESTRICTIONS BOOSTS EQUITIES

Equity markets continued to steadily recover last week, with all regions positive or flat in Sterling terms and only Emerging Market Equities down in local terms. Markets have been reacting positively to the gradual opening up of economies across the world, even with some signs that the Coronavirus is re-emerging in areas such as Wuhan […]

Quarterly Update: Will the Post-Covid Labour Market ever be the same?

'Work' may never be the same after the pandemic. How might things play out? What do businesses need to know to prepare? Read our quarterly economic update

Inflation momentum will recede. But prices may remain elevated.

There’s a strong possibility we may see the end of the episode soon. But supply chains could take long to mend and overall price levels could remain elevated versus pre-pandemic numbers.

Weekly Market Update: Bank of England and ECB keep rates unchanged

Read our full Market Update Week 37 Market Update Equities rose across the board last week, both in local and Sterling terms. UK stocks gained +0.4% with US and Global stocks up +0.1% and +0.3% in GBP terms. Other areas fared even better, as European and Japanese equities rose +0.8% and +0.6% respectively. However, Emerging […]

Weekly Market Update: BoE raises rates to highest level since 2009

Read our full Market Update Week 31 Market Update In local terms, equity markets fell across the board, aside from US equities which made a +0.8% return in USD (+1.5% in GBP). Global equities were flat in local terms but up +0.7% in Sterling as the Pound hit its lowest level since last September amid […]

Reflections in Inflections: Our Q3 Economic Outlook

After a decade of unprecedented monetary stimulus, we have failed to see global growth rates anywhere near their pre-crisis levels. At the same time, however, we have not seen a recession. The world seems to be ‘chugging along’ as output is pressured on all sides. So is it the Fed that killed economic cycles? Read our […]

Risks are climbing, so let’s buy…stocks?

Check out our new article on recession risk and thoughts on asset allocation: Is it time again for another crash? The US economy, the engine of global growth, has been expanding for 121 months, a historical record. As investors peer into the future, a case of acrophobia (fear of the extremes) is taking hold. “We […]

Weekly Market Update: US sanctions further Turkish instability

Read our full Market Update Week 32 Market Update As the pound continued its decline into last week, in local terms equity markets fell across the board aside from UK equities which made a +0.6% return. In Sterling all markets were up bar European equities, with US and global equities gaining the most with +1.9% […]

Weekly Market Update: US growth powered by strong retail sales

Read our full Market Update Week 33 Market Update Returns were mixed for equities in local terms as, aside from US equities which made a +0.7% return, all major regions fell. Similarly in Sterling all markets were down bar US and global equities which gained +0.8% and +0.1% respectively. Both European and Japanese markets returned […]

Weekly Market Update: Markets rally, Tesla delisting cancelled

Read our full Market Update Week 34 Market Update Last week and Monday was a positive period for risk assets, with global stocks returning +0.7%. EM equities gained the most, up +3.2% in Sterling terms and 4.6% in local terms, buoyed by Donald Trump’s announcement that he is prepared to resume talks with China (although […]

Weekly Market Update: Markets correct on NAFTA and Tech concerns

Read our full Market Update Week 36 Market Update Equities saw sizeable falls across the board last week, both in local and Sterling terms. UK stocks fell -2.0% with US and Global stocks down -0.7% and -1.5% in GBP. Other areas fared even worse, as European, Japanese and EM equities lost -2.3%, -2.6% and -2.8% […]

Angela’s long goodbye and what it means for investors

When Angela Dorothea Merkel became president of her party, the CDU, in 2000, her sights were set on the highest echelons of leadership in Germany. In 2005, she followed Helmut Kohl, her mentor, and Gerhard Schroder by becoming the third post-war leader of a united Germany. Furthermore, she was the the first who grew up […]

Mazars Quarterly Investment Outlook: Whatever Happened to the Global Synchronised Cycle?

Read our full Mazars Quarterly Investment Outlook – Q4 2018 Global Divergence In an early 2010 report Morgan Stanley warned that the biggest consequence of the 2008 global financial crisis could be isolationism and the reversal of a 50 year old trend which saw increasingly open borders, open trade and freedom of movement. As each […]

Weekly Markets Update: US Equities reach highs; May’s Chequers plans ambushed

Read our full Market Update Week 38 Market Update UK stocks traded higher with the FTSE 100 edging closer to the 7500 level, closing at 7472 point, up +2.65% for the week. In the US the S&P 500 reached new highs, returning +0.8% in GBP terms. Global stocks were up +1.5% in local terms and +1.6% […]

Weekly Market Update: Equities sell off on renewed trade war fears

Read our full Market Update Week 49 Market Update US equities sold off significantly last week, down -4.4% in Sterling terms, as trade war concerns weighed on American stocks, erasing the gains made in the previous week. Global equities were down -3.5% in Sterling terms, with all sectors apart from utilities experiencing negative returns. Emerging Market […]

Weekly Market Update: US treasury yields hit 7-year highs; European risk renewed

Read our full Market Update Week 40 Market Update US indices ended the week lower, with S&P 500 holding up more compared to the technology rich Nasdaq, as giants such as Amazon slipped. Financials stocks performed well given rising yields. The US 10-year Treasury yield closed the week at 3.23%, a 7-year high. UK stocks […]

Weekly Market Update: Equities rally despite no one liking Facebook’s outlook

Read our full Market Update Week 30 Market Update Japanese and Emerging Market equities lead markets higher last week, gaining +2.6% and +2.2% respectively in Sterling terms. These regions had their best week in more than two months, as China’s stimulus measures buoyed the region. News of an agreement reached between President of the European Commission […]

Weekly Market Update: Stocks sell off globally on rising bond yields

Read our full Market Update Week 41 Market Update Global indices suffered significant falls last week, down -4.1% in local terms and -4.5% in Sterling terms. US equities led the weak performance, experiencing their biggest losses in 8 months on Wednesday. Technology stocks were particularly affected as market participants reacted badly to rising bond yields. […]

Weekly Market Update: Global stocks continue their rebound while Oil prices drop further and Brexit uncertainty heightens

Read our full Market Update Week 46 Market Update Global stocks continued their rebound this week, with both Global and European equities up +0.3%. Emerging Market equities led the pack, returning +2.5% as the slide in oil prices gave a boost to emerging market currencies. UK Stocks were hit by further Brexit volatility, hardest hit stocks […]

Brexit Update: What now?

New Update! Monday 19 November 2018 After Friday’s dramatic cabinet session, which saw a third Brexit Secretary, Dominic Raab and Work & Pensions Secretary Esther McVeigh resign, there are several possible options on the table: 1) The deal might still go through parliament. Although divisions in the conservative party are high and it is unlikely that other […]

Mazars Wealth Management Investment Newsletter October 2018

Read our full MWM Newsletter October 2018 The global economy continued to grow in the third quarter of 2018 despite a backdrop of concerns over the continued imposition of trade tariffs primarily by the United States. It is apparent that any optimism a compromise between the US and its trading partners (China in particular) can […]

Monthly Market Update: EM’s Dollar Turmoil

Read our full Blueprint Sept 2018 August data continued to indicate global economic and risk asset divergence, consistent with a mature economic cycle, with USD assets rising as a result of Mr. Trump’s policies. The global economy is also diverging, with the US on a faster expansion path, while Europe and EM are slowing down. […]

Quarterly Investment Outlook: Is Globalisation Going in Reverse?

Globalisation is not inherently “good” or “bad”. It is the natural historic evolution of the nation-state, made possible by the internet and the potency of capitalism. But is it over?

Weekly Market Update: Trump questions Fed policy

Read our full Market Update Week 29 Market Update Sterling took another hit last week as lack of government unity surrounding Brexit saw the currency fall -0.7% vs USD, -1.1% vs EUR and -1.5% vs JPY. These moves increased returns on overseas equities for UK investors, with Japanese equities leading the way with +2.3% and […]

Mazars Wealth Management Investment Newsletter April 2018

Read our full MWM Newsletter April 2018 The first quarter of 2018 saw a return of market volatility and a reversal of gains from the end of 2017. Despite a strong January, global equities finished the quarter down 2.1% in local currency terms, but down 4.7% for UK investors as the Pound continued to strengthen, […]

Weekly Market Overview – Nervous equity markets continue to slide

Concerns over US Government debt levels, softening global macro data and a potentially hawkish Federal Reserve once again lead to negative equity returns after a significant sell-off in the previous 2 weeks. All global equity markets are now in negative territory for the year in both local and Sterling terms. Last week US markets were […]

Weekly Market Overview – Equity markets bounce despite inflation scare

Despite a brief panic on Wednesday when US inflation figures came in higher than expected, stoking fears of accelerated interest rate rises, markets had a strong week across the board following 2 weeks of significant market weakness. US markets were up 4.4% in USD terms, however weakness in the currency meant the return in Sterling […]

Market Comment – Mind the earnings

Traders were worried again last week, as US inflation figures came in higher than expected, suggesting the possibility of steep interest rate hikes. With heightened volatility, a very good US earnings quarter went almost unnoticed. With the reporting season almost over, 75% of companies beat earnings estimates and 78% beat sales estimates. This is the […]

Weekly Market Overview – Recovery continues despite rates normalisation talk by Fed

The market sell-off at the start of February was largely attributed to fears of rising interest rates in the US, with concerns that planned increases in fiscal stimulus to an already strong economy meant the Fed was getting behind the curve. Last week various members of the FOMC, although notably not the Chair Jay Powell, […]

Weekly Market Overview – Markets fear Taylorisation of Fed and trade wars

Markets continued their recent rocky period, with two separate events causing unease for investors. The first was Jay Powell’s first congressional testimony on Tuesday where he hinted at a faster pace of interest rate rises and stated a preference for rules based interest rate decisions. For example the Taylor Rule proscribes an interest rate for […]

Weekly Market Overview – US jobs report eases inflation fears

Markets had a strong run last week with all major equity markets posting gains in both local and GBP terms, except for Japan which suffered a loss in Sterling. The market seems to have fully rebounded following the sell–off at the beginning of February, with the Nasdaq back at a record high. US equities led […]

Weekly Market Overview – Trade war concerns weigh on markets

Both US equities and the US Dollar fell last week when multinational companies such as Boeing were hit as Donald Trump sought to impose new tariffs on China, pressing China to cut its trade surplus with the US by $10bn. As a result, there is an increased likelihood of a trade war between the worlds […]

Weekly Market Overview – Despite scheduled talks, looming trade war roils markets

Donald Trump’s announcement of around $60bn of tariffs against China due to intellectual property violations saw markets experience large losses, as participants feared an escalating trade war. China is expected to hit back with levies aimed at industries and states where Mr Trump’s supporters are concentrated. Equity falls came despite Congress agreeing a $1.3tn spending […]

Weekly Market Overview – Despite US assurances, trade war fears still weigh on markets

With the continued escalation of threats of tariffs between the US and China, markets suffered another week of negative returns. Global equities were down -1.0% in Sterling terms, dragged lower by US equities which returned -1.8%. Emerging Market and Japanese equities also suffered, down -1.1% and -1.0% respectively. European equities were relatively unscathed with a […]

Weekly Market Overview – Markets shrug off US strikes on Syria

Markets were volatile last week due to the possibility of air strikes on Syria, however opened slightly up on Monday morning after the US took action over the weekend. Equity markets were positive across the board in local terms last week, however Emerging Market and Japanese equities posted losses in GBP terms as the Pound […]

Mazars Wealth Management Quarterly Investment Outlook Q2 2018: The new “new normal”

Read our full MWM Quarterly Investment Outlook Q2 2018 The first quarter of 2018 saw a return of market volatility and a reversal of gains from the end of 2017. Despite a strong January, global equities finished the quarter down 2.1% in local currency terms, but 4.7% for UK investors as the Pound continue to […]

Mazars Weekly Market Update: Apple sours market recovery

Read our full Market Update Week 16 Market Update Equity markets saw another week of recovery with positive returns across all regions. Returns for UK investors were boosted by a weak return from Sterling, which sold off 1.75% on a trade weighted basis as Mark Carney, the Governor of the Bank of England, made comments […]

Weekly Market Update: Sterling continues to depreciate, global yields

Market Update This week saw mixed equity returns, with global stocks down -0.3% in Sterling terms. Emerging Markets posted a strong gain of +1.3%, which was supported by the Sterling depreciation observed across the period, while US stocks were down -0.7% for the week. Japanese equities fell -0.8% in local currency, however, the GBP/JPY rate […]

Mazars Weekly Market Update: Weak UK growth sees Sterling sell-off

Read our full Market Update Week 17 Market Update Global equity markets were flat to positive in local terms last week, however a large sell-off in Sterling due to fading expectations for a rate hike at the next MPC meeting in May meant that returns were positive for UK investors. Global equities returned 1.6%, US […]

Weekly Market Update: Italian populist government calms markets, US populist tariffs re-ignite concerns

Read our full Market Update Week 22 Market Update Markets sold off and yields rose in the first half of the week on fears about repercussions of the Italian President rejecting the populist coalition’s choice of finance minister and attempting to install a technocrat government. There were concerns that a new set of elections would […]

Weekly Market Update: Markets shrug off US G7 communique snub

Read our full Market Update Week 23 Market Update Last week markets were back in risk-on mode, as Global equities gained +0.9% in Sterling terms, led by US stocks which were up +1.2%. The gains were fairly evenly dispersed amongst sectors, although Utilities were the main loser as Treasury yields crept higher. Japanese equities were […]

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

The difference between a skirmish and a (trade) war

Why geopolitics now matter more In the past few years, investors and economies have grown somewhat insensitive to geopolitical surprises. Brexit, for example, did not cause the massive initial shock to either the economy or the stock markets that many analysts had predicted. Neither did Mr. Trump, whose election has sent stocks soaring by more […]

Weekly Market Update: Oil spikes as US inflation hits Fed target

Read our full Market Update Week 26 Market Update Global equities saw a second straight week of negative performance, down -0.7% in Sterling terms, with all major indices experiencing falls in both local and GBP terms. Once again escalating trade tensions were the prime reason for weak performance, although for the second week running UK stocks […]

Mazars Wealth Management Investment Newsletter July 2018

Read our full MWM Newsletter July 2018 Global economic growth continued in the second quarter of 2018, albeit in a much less broad based fashion than in Q1. The US economy led the way buoyed by high levels of business and consumer optimism, whilst Europe, and in particular France grew more slowly. Growth in the […]

Monthly Market Update: Markets unable to break out

Read our full Monthly Blueprint July 2018 Month In Review On the face of it, June has not been an exciting month for risk assets. Developed market stocks ended the month roughly in the same place as they started it, while long bond yields were little changed. However, beginning and end figures mask not only […]

Mazars Quarterly Investment Outlook: Mind The Liquidity

Read our full Mazars Quarterly Investment Outlook-Mind the liquidity A cautionary tale There’s an old story about a man who was marooned on a deserted island. Searching for food and water, he instead found a cave hiding a chest of pirate treasure. No water in sight though. He spent his last few days, next to […]

Weekly Market Update: Global stocks up heading into earnings season

Read our full Market Update Week 28 Market Update Global markets were up last week by +1.4%, despite a mid-week blip as once again Donald Trump increased the stakes against China, threatening tariffs on $200bn worth of exports. US stocks were up +1.9% in Sterling terms, however Emerging Market equities gained the most, up +2.0%. […]

European Risks Primer: Richlandia and Poorlandia

The article was originally published in the Money Observer on the 20th July 2018 The potential breakup of the Euro has been a permanently armed grenade under the bed of the global economy for almost two decades. The recent Italian elections driving yields up and the Euro down reminded allocators that European risks have never […]

Mazars Wealth Management Investment Newsletter Summer

Global equity markets continued to rise during the second quarter of the year, with global equities now returning over 20% in Sterling terms year to date. Similarly to the previous quarter, this market rally occurred despite any real optimism about the state of the global economy although some caution could be observed in the price […]

Recessions. Remember them?

Recent conversations with our clients have often begun with them expressing concern about the possible effects of Brexit on investment portfolios. Given the lack of clarity on how the situation will unfold or what the impacts might be, this is perfectly understandable. But, whilst the near term prospects for the UK economy are undeniably intertwined […]

Who will be the leaders of Artificial Intelligence? How should “big tech” be regulated

We are at an inflection point. Technological innovation drives our economy, and ultimately, our standard of living. From rail roads to the Internet, technological progress has pushed our productivity levels to new heights, and we are now on the brink of the next step of this evolution. Artificial Intelligence. Once just the topic of sci-fi […]

Quarterly Outlook: Beyond Covid

The persistent dichotomy between stock market performance and economic performance has been a particularly hard puzzle for investors. While it is very clear that the previous 12-year economic cycle has undoubtedly come at an end, the financial cycle, thanks to central banks, has survived a five standard-deviation event (1 in 3.5 million probability), and continues unabated. With the global economy in turmoil, can stock and bonds be trusted to create or even maintain wealth?

WEEKLY MARKET UPDATE: Markets fall on second wave fears, gloomy Fed

Read our full Market Update Market Update The rally in risk assets came to a grinding halt last week on fears of a second wave of infections in the US, with virus rates up in many states, and the Federal Reserve offering up a gloomy economic outlook. Stocks are also down this morning on news […]

Why it pays to be a long term investor

Please read the full article here: In the current investment climate where central bank activity and algorithmic trading strategies are two primary driving forces of asset prices, enabling rapid losses and even faster gains as momentum funds then push winners higher and losers lower, we are reminded how important it is to follow a long […]

Quarterly Investment Outlook Q3 2020: Covid Recovery and Anxiety

A quarterly report is not normally a difficult document to put together. Usually it consists of an account of the trending state of affairs, the more possible outcomes and risks to those outcomes. In the past few years, these reports were actually made easier. The US Federal Reserve was underwriting risk at such an unprecedented scale, nearly unwavering for more than a decade, in a manner which suppressed all major hazards to the economy and financial markets. Ever since 2010 the question, repeatedly, had been: “With opportunity costs driven down so much for so long, whatever can bring markets down?”

Weekly Market Update: Stock markets post mixed returns on virus fears

Please read our full Market Update Market Update Stocks posted mixed returns last week, with strong performance in the US as the NASDAQ 100 set new record highs, while UK and Japanese stocks closed down -0.9% and -1.8% in Sterling terms respectively. Emerging Market stocks performed well, gaining +2.4% for the week. Technology, Telecoms and […]

WEEKLY MARKET UPDATE: MARKETS SLIDE ON US-CHINA CONSULATE CLOSINGS

MARKET UPDATED Despite recent strength, equities closed lower last week as tensions between the US and China were ratcheted up, with the forced closure of the Chinese consulate in Houston and the arrest by the US of a Singapore national who has admitted spying for China. In response China has ordered the US consulate in […]

Weekly Market Update: Equity Markets Rebound, Gold continues to soar

Read our Full Market Update Market Update Bucking the trend of two consecutive weeks of falling equity markets, all major indices were positive last week. Global equities gained +2.7% in Sterling terms, with the Nasdaq Composite reaching new highs, and the S&P 500 now close to its February peak. After a poor week last week, […]

Weekly Market Update: Increasing COVID-19 case count caps equity market rally

Read our full Market Update Market Update Global equities traded higher last week, up +0.5% in Sterling terms. US equities climbed +0.9% with housebuilders, buoyed by promising housing data, leading the way. Other developed markets did not fare as well. UK and European stocks were down -1.3% and -1.1% respectively, driven by both the negative […]

Weekly Market Update: Stocks edge higher, bolstered by stumbling sterling

Read our full Market Update Week 37 Market Update Globally stocks were negative in local terms, losing -1.3% for the week. However Sterling weakness, which saw it worst week since March, saw global stocks rise +2.2% in Sterling terms. UK stocks performed well gaining +4.0% for the week, with Housebuilders and Healthcare both rising by […]

Weekly market update: stocks decline on fears of a second wave of covid and stimulus uncertainty

Read our full Market Update Week 39 Market Update Major global markets were negative in local currency terms, whilst a weaker Sterling which was down -1.3% for the week against the US Dollar and -0.4% against the Yen ensured some pockets of growth for British investors. US stocks moved into correction territory (down 10% from […]

Monthly Market Blueprint: If you are looking at the election, you might be looking in the wrong place.

Dear reader,This note was written mid-day on 3 November, just a few hours before the US presidential election result. Naturally, we were tempted to delay, to get a clearer view of the earth-shattering events surrounding the world’s biggest economy and longest standing democracy. However, we decided to consider that the US presidential election could be […]

WEEKLY MARKET UPDATE: UPBEAT US JOBS FIGURES BOOST EQUITIES

Equities saw a third straight week of strong returns, with Japan the only region experiencing losses in Sterling terms (down -1.6%), although it was also positive in local terms (up +3.1%). US ADP National Employment figures showed fewer job losses, causing an initial spike in equities, which continued later in the week as it was […]

Weekly Market Update: Covid-19 vaccine breakthrough fuels global equity rally

Market Update Global equities rallied strongly last week on news that early data shows Pfizer’s Covid-19 vaccine, one of many in development, is effective in 90% of cases. Equities rallied sharply in the first half of the week before ceding some of their gains later on as attention turned back to the near-term, where Covid-19 […]

Weekly Market Update: Major indices end the year on a positive note

Market Update Most major equity market indices ended the year on a positive note. Global stocks gained +0.2% in Sterling terms over the last two weeks of trading to close the year up +12.4% in Sterling terms. Over the year, due in large part to a Tech rally following the early pandemic crisis, US stocks […]

Is gold a good hedge against inflation?

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise.

The latest position of the ECB

Christine Lagarde, President of the ECB, gave a press conference on 10 June following a meeting of the ECB’s governing council. Her speech contained some unequivocally positive observations about the European economy, lamenting a bounce back in services activity, continued strong manufacturing activity and improving consumer spending, all against a backdrop of strong global demand. […]

Weekly Market Update: Stocks Shrug Off Higher Inflation

Market Update Global markets were again positive for the week, although with global yields falling markedly, it was the growth and bond-proxy sectors which were positive, with healthcare and IT the standout gainers. Meanwhile cyclical stocks, which have seen upturned performance since the positive vaccine news in November, had a poor week. Financials, materials and […]

Shariah Investing: the growth of the Islamic Finance gives private clients more options than ever before

This article is the first in a series about Islamic investing Most investment advisers have encountered investors looking for Shariah compliant portfolios at some point. My own experience has previously been one of frustration as the universe of investable funds did not offer enough options to be able to construct portfolios which satisfied clients’ risk […]

Weekly Market Update: US equities near all time highs as earning beat expectations

Market Update Global equities rallied last week, with US equities leading the way, up +1.4% in Sterling terms, boosted by 87% of US firms beating earnings expectations. European equities were up a similar amount in local terms, however up only +0.4% in Sterling terms. UK equities were up +0.2%, however Japanese equities fell -1.3%. With […]

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

It’s not inflation that will transition. It’s everything else.

A new, more transmissible variant, and a surprisingly hawkish Fed brought some of the most volatile trading days in months.

Quarterly Outlook: Sustainomics and a world without QE

2022 is the year where QE (conceivably) ends, and a decade-long Sustainability theme begins. Read our annual outlook.

Monthly Market Blueprint June 2020

The “right” fundamentals Often the first thing we are taught about something, especially if it comes from someone with authority, like a parent, a teacher or our experienced financial adviser, is taken as a “fundamental” truth. In psychology, this is called the “primacy effect”. Any other “truths” that contradict or seek to modify that first […]

Weekly Market Update: Equity Momentum Continues

For a second week in a row it was green across the board for equities, as global stocks gained +2.4% in Sterling terms and +3.7% in local terms. European stocks were amongst the best performers for a second week, with Japanese equities performing equally well. Early in the week markets focused on the US returning […]

Weekly Market Update: Stocks sink as the Fed disappoints traders

Market Analysis This week saw stocks suffer globally, with global stocks down -1.1% in Sterling terms. US equities suffered their worst week thus far in 2019 as market sentiment was dealt twin blows by disappointing signals from the Fed and the announcement of new tariffs on imports from china. US equities were down -1.2% for […]

Tinker, Tailor, Soldier… Huawei?

This is a multi-level chess game, touching politics, intelligence and trade, and a move in each field directly affects the other two.

Weekly Market Update: Yield curve inversion spooks markets

Read our full Market Update Week 33 Market Analysis Last week saw equities decline globally, both in local and Sterling terms. US stocks recorded a third straight week of losses as trade and growth worries unsettled investors, down -1.6% in Sterling. The typically defensive consumer staples and utilities sectors performed best within the S&P 500 […]

Why are investors paying to lend to governments?

It seems we should all be taking on debt. After all, about 30% of the global tradeable universe of bonds is negatively yielding, amounting to around $16.7trn. With bonds that are negatively yielding, holding to maturity guarantees a loss, at least in nominal terms. In other words, it seems you are being paid to borrow. […]

Weekly Market Update: Global equities decline as trade war escalates

Read our Full Market Update Week 34 Market Analysis Last week equities continued to decline, both in local and Sterling terms. Emerging Markets led the decline, falling -1.5% in Sterling terms. US, UK and Japanese stocks fell -0.9%, -0.2% and -0.9% respectively. European stocks were flat in Sterling terms. Globally, the best performing sectors were […]

Weekly Market Update: Sterling depreciates as no-deal probability increases

Read our full Market Update Week 35 Market Analysis There were gains across the board last week, as China indicated it had no immediate plans to retaliate to the latest round of US tariffs. In Sterling terms, global equities were up +3.0%, led by US equities which were up +3.7%, as trade-sensitive technology and industrial […]

The World in 2024

Recently, we were asked by our management committee to answer a deceptively simple question: what will the world look like in 2024 from an economic perspective? The task was daunting: articulating a cohesive world view, years ahead. To do that, we need to step back and look at the world we created at the dawn […]

Q4 2019 Quarterly Outlook

Read our full MFP Quarterly Investment Outlook Q4 Ghosts of Japan Growth has been consistently slowing across the globe. In the past two issues, we dealt with the impact of China’s slowdown, as the world’s marginal buyer goes through the necessary pains of transformation and the impact of elongated cycles on growth. In this outlook […]

The Trillion Dollar Question – Can We Lose Faith in Central Banks

Trillion Dollar Question – Can We Lose Faith in Central Banks However, we would only be touching the surface, inadvertently veering into the sphere of gossip, were we to dismiss such disagreements as mere power plays. In fact, we do not think that investors should care much about ‘who controls the ECB’. Stereotyping, where northern […]

Weekly Market Update: Bond yields rise, gold price declines

Read our full Market Update Week 45 Market Update Global stocks rose +0.8% in local currency terms and +2.1% in Sterling terms in yet another positive week for risk assets. Meanwhile yields rose sharply and Gold had its worst week in three years as there was a flight from defensive assets. In Sterling terms US […]

Weekly Market Update: Global Equities Rise, but Sterling Rallies More

Market Update Global stocks rose +0.7% in local currency terms, which translated into a -0.4% fall in Sterling terms. Returns were mixed in local terms, however were universally down in Sterling term as the currency rose +1.0% vs the US Dollar to just short of the $1.30 mark. Emerging Markets had a challenging week falling […]

Mazars Wealth Management Investment Newsletter – Winter 2020

Read our full MWM Investment Newsletter Winter 2020 Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7%. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservatives’ decisive general election victory. The late final rally was […]

Q1 Quarterly Investment Outlook: 2020: The Power of the Cycle

Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7% in local currency terms. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservative’s decisive general election victory. The late final rally was primarily driven by renewed optimism for a ‘phase one’ trade deal between the US and China, and left global equities up 25% for the year. It is of course important to note that, by contrast, markets ended 2018 in very pessimistic mood as the Fed continued to raise interest rates, and therefore a global equity return figure of around 8% from September 2018 is a more useful measure of equity returns.

WEEKLY MARKET UPDATE: US-CHINA RHETORIC UNNERVES MARKETS

Markets rallied throughout last week, however US equities closed lower on Friday and down -1.6% in Sterling terms for the week, with other regions following suit this morning, on concerns that tensions between the US and China could escalate due to accusations from the US administration over the origins of the Coronavirus. For the week, […]

Volatility in global stock markets continued last week, but with little direction and significant swings between positive and negative daily returns

Figure 1. US stock market returns in the last two weeks. The most significant development last week (other than the continued spread of the Covid 19 virus itself) was the 0.5% emergency rate cut announced by the US Federal Reserve which received a luke warm reception from markets. Over the last ten years we have […]

Stocks fall across the globe as COVID-19 cases climb, Oil prices drop as Russia refuses supply cuts

Please check out our full Market Update Week 10 Market Update UK equities were down nearly 9% this morning, with the natural resource and banking heavy indices experiencing weakness for three prime reasons. First, coronavirus fears continued to rise as Italy quarantined 16 million residents, with investors fearful of this impact on the global economy […]

Weekly Market Update: Stock markets suffer record daily falls, central banks cut interest rates to combat coronavirus induced slowdown

Read our full Market Update Week 11 Market Update UK equities were down over 8% this morning, with the FTSE 100 down -32% over the last month as markets are now starting to price in a coronavirus induced global recession. Oil prices continued to slip, down nearly 50% YTD in USD terms. This fall has […]

Investing, “in the time of Cholera”

We can comfortably use a phrase that, under other circumstances, would surely risk bringing upon us financial anathema: “This time is different”.

WEEKLY MARKET UPDATE: A MORE SANGUINE WEEK FOR MARKETS

By regular standards it was a rocky week for equities, which rallied 2-3% in the first few days, but fell 4-5% later on. However in comparison to preceding weeks market moves were somewhat muted, perhaps because the news-flow has provided little further clarity as to the time-scale and magnitude of the COVID-19 crisis – markets […]

WEEKLY MARKET UPDATE: IS THIS RALLY A “HEAD FAKE”?

Last week (Friday 3 to Monday 13 April) global stocks rose on the back of an improved narrative regarding the Coronavirus pandemic, as markets see a ‘flattening of the curves’ and a reduced pace of new infections, while many countries weigh reopening their economies. Boris Johnson’s survival helped improve the narrative both for the UK […]

Quarterly Investment Outlook Q2 2020

At our Investment Committee meeting in the first week of January we discussed amongst other things the heralded resolution of the trade war between the US and China, the fact that the US Federal Reserve was printing more money, and the renewed optimism that came from a stable government here in the UK. Cautious bullishness on risk assets was the tone of the meeting. Looking back at our discussion documents from that meeting, our ‘Wall of worry’ chart which details the things which we consider to be possibly obstructive to stock market gains, did not even mention Coronavirus. In other words, we have experienced a true ‘Black Swan’ event. Global stock markets fell by 20% over the first quarter (around 15% for a Sterling based investor) having lost as much as 32% by mid-March. Gold performed its role as a safe haven rising 12% in Sterling terms, whilst Gilts rose by over 6%.

Quarterly Investment Newsletter Spring 2020

At our Investment Committee meeting in the first week of January we discussed amongst other things the heralded resolution of the trade war between the US and China, the fact that the US Federal Reserve was printing more money, and the renewed optimism that came from a stable government here in the UK. Cautious bullishness on risk assets was the tone of the meeting. Looking back at our discussion documents from that meeting, our ‘Wall of worry’ chart which details the things which we consider to be possibly obstructive to stock market gains, did not even mention coronavirus. In other words, we have experienced a true ‘Black Swan’ event. Global stock markets fell by 20% over the first quarter (around 15% for a Sterling based investor) having lost as much as 32% by mid-March. Gold performed its role as a safe haven rising 12% in Sterling terms, whilst Gilts rose by over 6%.

Monthly Market Blueprint April 2020

The month in review: March Market Meltdown Q1 2020 saw the worst quarter for risk assets since the Global Financial Crisis as the dual shock of the COVID-19 pandemic and the Saudi Arabia-Russia oil price war wiped out equity markets and pushed credit spreads higher. Capital fled to the sovereign bond market with Treasury yields […]

WEEKLY MARKET UPDATE: VALUATIONS REMAIN HIGH

After several weeks of recovery, equities fell in all major regions last week. Due to weak Sterling, both US and Japanese equities were flat for UK investors. However European (-0.5%), UK (-0.5%) and Emerging Market (-1.1%) equities were all negative in Sterling terms. The Energy sector was the best performing globally, even though the outlook […]

Weekly Market Overview – US Dollar slide sees negative equity returns for UK investors

Global equities were mostly positive in local terms last week, however a fall in the US Dollar, combined with Sterling appreciating, meant that returns for UK investors were generally negative. Weak US Dollar performance was largely due to a statement at Davos by US Treasury Secretary Steve Mnuchin being interpreted as suggesting that the US […]