Is China facing an economic slowdown?

Thought Leadership

Is China facing an economic slowdown?

Thu 07 Apr 2022

China was the first country to successfully emerge from the initial Covid-19 wave. People were back to the office in 2020 itself, infection rates plummeted and as a result economic growth was stellar, beating all expectations. China emerged as the winner at a time when most western countries were still coming to terms with the Covid -19 pandemic and its repercussions. The last 12 months however, have been an absolute reversal for China.

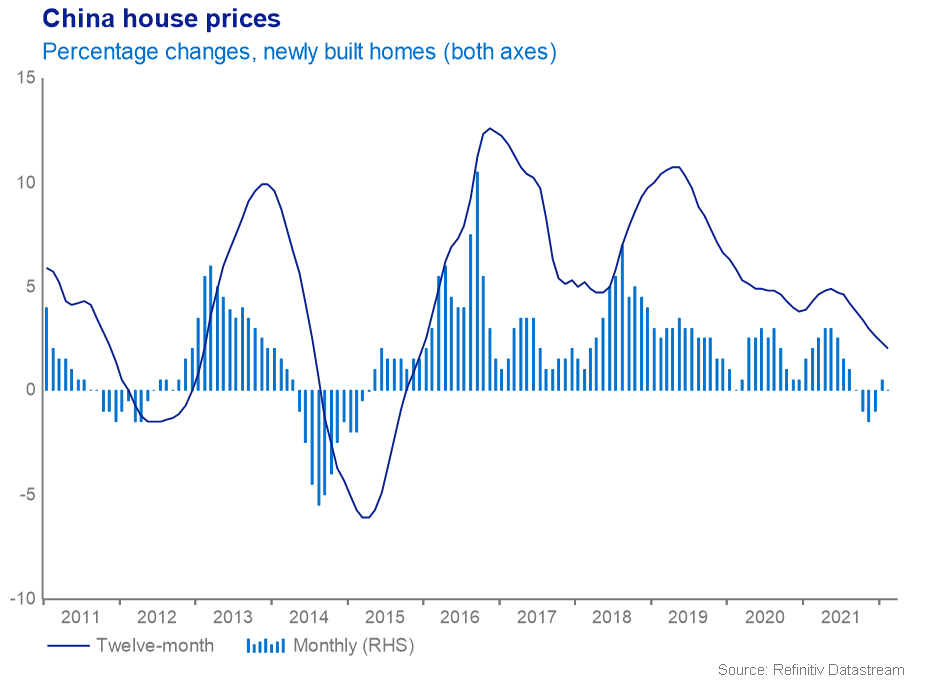

A real estate ‘bubble’ is showing concerning signs of bursting. China’s Evergrande Group has rapidly become Beijing’s biggest corporate threat as it wrestles with debts of more than $300 billion as a result of years of aggressive expansion. But that was just the tip of the iceberg. The total combined debt of China’s major property developers is now estimated at more than $5 trillion. To make matters worse, 20 of the top 30 property firms by sales have breached at least one of three debt limits set by the Chinese government to rein in real estate speculation, meaning they’re unsustainable. With property being a key driver of economic growth ― contributing about 29% to China’s GDP ― any major real estate crash could threaten the entire Chinese economy.

To make matters worse, the Chinese regulator launched a multi-pronged crackdown on its tech, gaming, gig economy, education and cloud computing companies, leaving start-ups and decades-old firms alike operating in a new, uncertain environment. New regulations tackled issues such as high borrowing levels, data privacy and ring fencing businesses to combat anti-competitive behavior by large umbrella corporations.

On the macro side of things, China’s manufacturing and trade heavy sectors have suffered a slowdown amid fallout of Ukraine war and new Covid-19 outbreaks and lockdowns. Factory activity slumped at fastest pace in two years.

There is no denying that a slowdown in China is likely to have knock-on effects across the region, much of which counts the world’s second-largest economy as the biggest source of trade. However, a few points worth mentioning:

- Macro metrics such as retail sales, industrial production and fixed asset investment are slowing down – but this is after a period of exceptional growth, which was never going to be sustainable.

- Most indicators are looming around their pre-Covid levels – signaling strong growth followed by normalization.

- Biggest risk to equities (over the last 6 months) has been regulation of sectors like education, banking, technology, data etc. However – this is bound to reduce investor concerns over the long term.

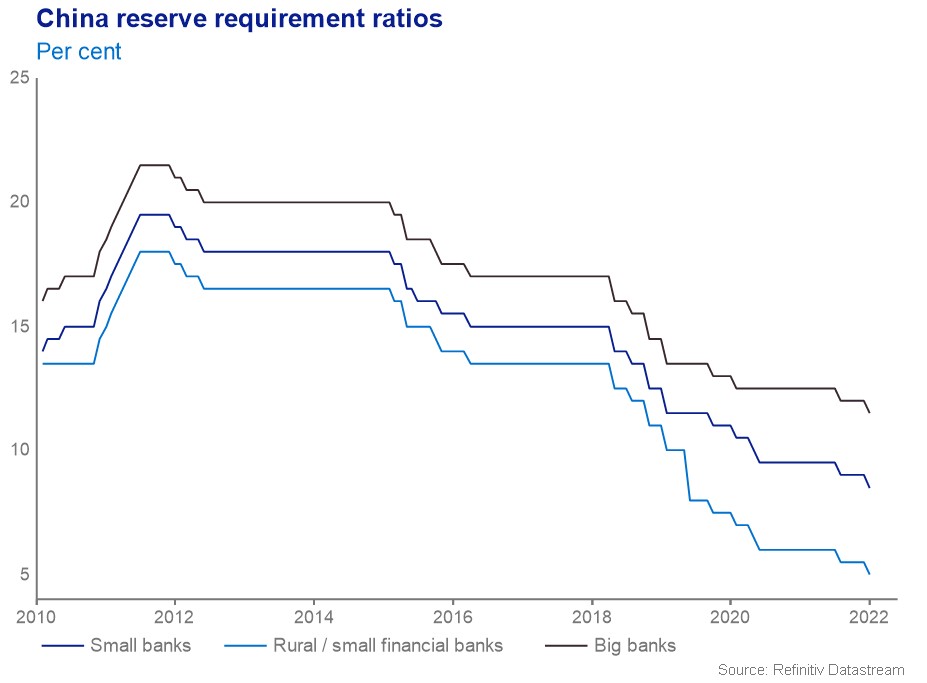

- China’s central bank remains uber accommodative – while the west raises interest rates and tightens policy overall, China is focused on solving its economic issues.

China has faced a slew of challenges to growth in 2021, including a power shortage, shipping delay, Covid-19 outbreaks and a crisis in the real estate sector. The central bank’s rate cuts sends a signal that policy will turn accommodative if need be.

China’s property sector woes

China’s Evergrande Group has rapidly become Beijing's biggest corporate threat as it wrestles with debts of more than $300 billion as a result of years of aggressive expansion. But that was just the tip of the iceberg.

Xi Jinping’s Infinite Rule

Things have been looking up for China recently, as market sentiment towards the world’s second largest economy has finally started to take a positive turn. Since 2015, when the country’s stock market sold-off sharply and the Shanghai Composite Index crashed 45% in under two months, investors have understandably been wary of China. Redemptions in Chinese […]

Quarterly Investment Outlook: Is Globalisation Going in Reverse?

Globalisation is not inherently “good” or “bad”. It is the natural historic evolution of the nation-state, made possible by the internet and the potency of capitalism. But is it over?

The difference between a skirmish and a (trade) war

Why geopolitics now matter more In the past few years, investors and economies have grown somewhat insensitive to geopolitical surprises. Brexit, for example, did not cause the massive initial shock to either the economy or the stock markets that many analysts had predicted. Neither did Mr. Trump, whose election has sent stocks soaring by more […]

Weekly Market Update: BoE’s Chief Economist dissents to put 2018 rate hike on table

Read our full Market Update Week 25 Market Update Global stocks turned negative last week following two weeks of positive performance. Emerging Market equities were the worst hit, falling -2.0% in Sterling terms, as rising trade war fears also weighed on global equities, which were down -0.7%. Japan was also badly hit due to its […]

Weekly Market Update: S&P 500 hits all-time high, Chinese economic growth slows to multi-decade lows

Read our full Market Update Week 28 Market Update Despite a mixed week for equities, the S&P 500 set new records on Friday, closing above 3,000 for the first time at 3,013.77. US equities gained +0.4% in Sterling terms, with all other major regions down. Emerging Market equities fell the most, down -1.2%, European equities […]

Risks are climbing, so let’s buy…stocks?

Check out our new article on recession risk and thoughts on asset allocation: Is it time again for another crash? The US economy, the engine of global growth, has been expanding for 121 months, a historical record. As investors peer into the future, a case of acrophobia (fear of the extremes) is taking hold. “We […]

Market Volatility: This dance we have danced before (and shall again)

Financial market turmoil continues for the second straight week, plunging the S&P 500 close up to 7% from its peak, in a bout of volatility similar to last December’s. The reasons behind the recent tumult are rather straightforward: 1) A stock re-rating, after Fed Chair Powell last week suggested that the central bank is not entering […]

The Current (Trade) War

In the past weeks we saw markets react negatively to fresh tariffs on China. However, it is more likely that traders were simply responding to the Federal Reserve’s attempts to maintain its independence against the US President by taking a more staunch view on the cost of money. The Fed’s independence might just be an […]

Monthly Market Update:A recession nearing?

Read our full Monthly Market Blueprint Sept 2019 •Global economic data continue to indicate contraction in global manufacturing and a slowdown in services. The US has joined the cohort of large countries which now see their economy slow. Inflation remains at bay and unemployment in developed markets is near all-time lows. Yet consumption is dented […]

Weekly Market Update: Weak Week for Sterling

Market Update Major developed market equities gained in Sterling terms this week, due in large part to currency effects. Many of these indices actually fell in local currency. UK equities grew by +1.1% led by utilities and healthcare sectors. US stocks were up +0.4% in Sterling terms but had fallen -1.0% in local currency, this […]

When the black swan visits

Since 2018, a key concern of financial markets has been the increasing trade tensions between the United States and China, more commonly referred to as the ‘trade war’. With delays and failed negotiations lasting over a year, markets finally breathed a sigh of relief on the 15th of January, as the US President Donald Trump […]

Weekly Market Update: Markets Mixed As Lockdowns Reimposed Over Second Wave Concerns

Market Update Global equities were narrowly down -0.3% on the week in local terms, however Sterling weakness once again boosted returns to British investors. The US was the best performing region, up +1.0% in Sterling terms. This coming week will kickstart earnings season in the US, where earnings are expected to fall sharply relative to […]

Weekly Market Update: Major indices end the year on a positive note

Market Update Most major equity market indices ended the year on a positive note. Global stocks gained +0.2% in Sterling terms over the last two weeks of trading to close the year up +12.4% in Sterling terms. Over the year, due in large part to a Tech rally following the early pandemic crisis, US stocks […]

What is the difference between a Mazars CIO and a boiling frog?

As an analyst I hate metaphors. While they are a very useful tool to turn my thorough -but often thoroughly boring- analyses into actual readable pieces, they also almost always convey a false sense of proportion. One of the most successful, yet dangerously misleading narratives I’ve read lately is one that equates investors to slowly […]

Weekly Market Update: China’s ‘LTCM moment’ may be the least of its problems, and ours.

Global stocks were relatively unchanged in Sterling terms (down -0.7% in USD terms) last week amid investors’ skepticism around supply chain issues hampering growth, elevated valuations and future monetary policy. Japanese stocks posted gains for a consecutive week, rising by +1.1%, as campaigning began for the next president of Japan’s ruling LDP. UK stocks fell by -0.9% amid higher than expected inflation, while US stocks were up +0.2% driven by a strengthened US Dollar. Globally, all sectors exhibited losses apart from energy stocks which posted solid gains of +2.8%. The US 10Y Treasury yield was up 2.1bps finishing the week at 1.363%, while the UK 10Y yield was up 8.9bps reaching 0.848%. Sterling fell against the US Dollar by -0.7% and remained flat against the Euro. In US Dollar terms gold lost -1.2%, while oil was up by +4.0%.

Weekly Market Update: Operations Managers are the new economists

Equities in most major markets posted minor gains last week with global stocks up +0.3% in Sterling terms, as inflation concerns seem to have stemmed a previously strong investor sentiment. US stocks were up +0.2% as multi-year high inflation data offset positive news on employment data. EU stocks were up +0.2%, despite Covid-19 cases surging in most countries in the region. UK stocks were up +0.7% while EM equities rose by +2.2%, driven by China’s announcement that it would propose easing measures to aid indebted real estate firms. The US 10Y Treasury yield was up 11.0bps finishing the week at 1.561%, while the UK 10Y yield was up 6.9bps reaching 0.914%. In US Dollar terms gold posted solid gains for the second week in a row, up +3.1%, while oil was down -0.1% to $80.4 per barrel.

Market Comment – Macro headwinds

Last year was very positive, both in terms of stock market and macroeconomic volatility (the volatility of macroeconomic releases). In recent weeks, however, we have noticed a deterioration in macroeconomic releases, especially in the US. Lower inventories and higher imports took a toll on GDP. More detailed data on capital expenditure also shows weakness in […]