2016/17 Employment-Related Securities (ERS) Filing - What you need to know and do re share plan returns 6 July deadline

2016/17 Employment-Related Securities (ERS) Filing – What you need to know and do re share plan returns 6 July deadline

2016/17 Employment-Related Securities (ERS) Filing – What you need to know and do re share plan returns 6 July deadline

Sun 19 Feb 2017

The online changes introduced from April 2014 relating to share plan registration and annual returns filing led to a number of ‘teething problems’, some of which remain a concern now for 2016/17.

Authorisation codes going astray in the post remain a problem for those new to the ERS online system. It is therefore imperative that preparation begins as soon as possible, especially in relation to any new share plan arrangements introduced in 2016/17 which require first registration.

Last year HMRC made changes to the reporting templates. However we are not expecting any fundamental changes to the templates for 2016/17.

From a risk perspective, HMRC’s focus has changed to enforcement of ERS filing compliance. Although the ERS filing may seem a mundane, administrative task, it provides HMRC with useful information for comparison purposes against payroll records, deductions claimed for Corporate Tax purposes and self-assessment filings. There are now automatic penalties for failures and so companies should ensure ERS filings are completed accurately and align with other associated reporting made to HMRC.

Recap on the online reporting process

From April 2014, all share plans (UK tax-advantaged and UK non-tax-advantaged, including overseas plans with UK participants) must be registered online with HMRC via an ERS online service. This includes both new and existing share plans, even if the plan had previously been approved by HMRC.

All tax-advantaged plans and other share arrangements with reportable events prior to 6 April 2016 should already be registered (and for SIP, CSOP an SAYE plans, also self-certified) by 6 July 2016. For 2016/17 reporting purposes it is not required to re-register those plans, however an annual compliance return needs to be filed.

Any new arrangements established after 5 April 2016 must be registered by 6 July 2017 and a compliance return also requires filing by that date. If a plan has ceased then a closure event needs to be reported and a final return filed.

What needs to be registered?

=> For new share plan arrangements for 2016/17:

1. Register the share plans online;

2. Self-certify certain plans online (SIP, CSOP and SAYE only); and

3. File annual returns online.

This applies to the following share plans:

- Enterprise Management Incentive (EMI) plan

- Share Incentive Plan (SIP)

- Save As You Earn (SAYE)

- Company Share Option Plan (CSOP)

- All other arrangements, previously reported on Form 42, including foreign plans

SIP, SAYE and CSOP have to be self-certified as meeting the requirements of the applicable tax legislation. HMRC are currently undertaking compliance checks nationally to verify such statements, so if you are in doubt about the position of your plan we can provide a proactive health-check review for assurance purposes.

EMI option grants also have to be notified online (this needs to take place within 92 days of grant or the tax advantages are lost).

Once a plan is registered, a unique reference number is issued online, which is required to then submit the annual filings. This unique reference number is usually issued 24-48 hours after the plan has been registered online. It is therefore important that any registration of new plans happens well ahead of the 6 July 2017 deadline as registering the plan on the deadline day will result in a late filing.

Additional time needs to be built in to the process if you are appointing an agent (or a new agent) to act for you as there is a separate agent authorisation process to complete.

=> For pre-existing share plans already registered (and certified where relevant):

A return filing is required.

The filing deadline for new and existing share plan arrangements (both UK tax-advantaged plans and non-tax-advantaged plans) is 6 July 2017.

What happens if you do not register your plan(s)?

If you do not register a new tax-advantaged CSOP, SIP or SAYE share plan before 6 July 2017, the plan may lose all tax advantages. To the extent that existing share plans in place prior to 6 April 2016 were not registered on a timely basis last year, tax advantages may already be lost. If this applies, please contact us and we can discuss your specific case.

Neither you, nor an agent acting for you can file an ERS compliance return for a plan until the registration process has been completed. A first registration plus ERS agent appointment can take 4-6 weeks to set up.

How to register and self-certify using the ERS online service

To register your plans and arrangements, you need access to HMRC Online Services and PAYE for Employers and it can take 7-10 days to obtain login details. Login details are returned by HMRC using the post (this will take longer if HMRC are posting the information to an overseas address). Once you have obtained access:

1. Login to HMRC Online Services;

2. Continue past the security message;

3. Click on ‘Services you can use’ in the left-hand menu;

4. Click on ‘PAYE for Employers’;

5. At the bottom of the page on the right-hand side there is a section called ‘employment- related securities’. Click on ‘Register a scheme or arrangement’ and follow the on-screen instructions.

Action to consider prior to April 2017:

Frustratingly, it is the very first step in the above process which often causes problems. It is therefore very important that you check now that you can access the ERS online portal even if you want an agent to file the return for you. Things to be aware of:

- Even though you are being asked to report online, much of the process is dependent upon authorisation codes sent by post. HMRC will send ERS information by post to the address shown in its records for the company for UK PAYE purposes. You should check now that the address records are up to date.

- You may have outsourced your payroll and therefore there may currently only be a payroll agent PAYE access set up. You will need to contact HMRC to set up a separate employer PAYE access to enable you to report ERS matters.

- You may have a legacy employer PAYE login set up but perhaps have since outsourced payroll and no longer have a record of the previous log in details. This is proving a particularly difficult situation to resolve with HMRC so if you think you might need to request a new login you should contact HMRC as soon as possible as it is likely to take several weeks for you to gain access to the ERS portal.

- An ERS agent cannot register a plan or enter a plan termination event. Only the company login provides this functionality. An agent can view what has been registered and file returns.

Why is it advisable to register your new share plan(s) well before 6th July 2017?

As much of the process still relies on information being sent by post and problems with the online system still arise from time to time, we recommend that registration is undertaken as soon as possible.

Despite lobbying efforts, HMRC have not yet made any movement towards the use of e-mail communication or online authorisation code confirmation. This has led to cases where registration and agent authorisation code letters have been sent to incorrect or unmonitored addresses leading to delays and duplicate requests for codes.

ERS correspondence from HMRC is usually marked for the attention of the Company Secretary even where the company does not have such an officer or where the Company Secretary is not the ERS reporting officer for the company. This all increases the risk that such post will not be directed appropriately within a large organisation.

Additional care to be taken with Internationally Mobile Employees (IMEs).

The reporting requirement extends to non-UK based employees who have carried out work duties in the UK during the earning period (generally between award and vest/exercise). Companies must have visibility of overseas employees carrying out work duties in the UK where they participate in equity awards to ensure relevant transactions are reported for ERS purposes.

This is a complex area and one where we can provide expert guidance to ensure compliance and avoid potentially significant penalties for materially inaccurate returns (see below).

Automatic penalties apply for late filing and incorrectly completed/formatted returns as follows:

- 7 July 2017 – an immediate £100 penalty

- 3 months late – additional £300 penalty

- 6 months late – additional £300 penalty

- 9 months late – additional £10 penalty for each day the return remains outstanding

There is a penalty of up to £5,000 for a material inaccuracy in a return which is not immediately addressed.

Due to the significant issues with the online system for the 2014/15 tax year, HMRC began to apply automatic late filing penalties for the 2015/16 filing only. For 2016/17, automatic penalties will be issued by HMRC and a “reasonable excuse” will be required to appeal any penalty.

In some cases penalties have been issued for incorrectly registered plans where returns have not been filed. Any incorrect plan registrations require a nil return to be filed and the plan then deregistered online. Penalties will be issued where returns are not filed (even where this would be a nil return). The situation is similar for plans registered online in advance of any award being made. Once the plan is registered there is an obligation to file returns online each year.

If you wish Mazars to assist with your annual ERS return reporting for 2016/17 then we request that you have registered your plan(s) by 30 April 2017. Only the company can register the plan. An ERS agent cannot register a plan for you. We can provide guidance on the registration process as part of our assistance.

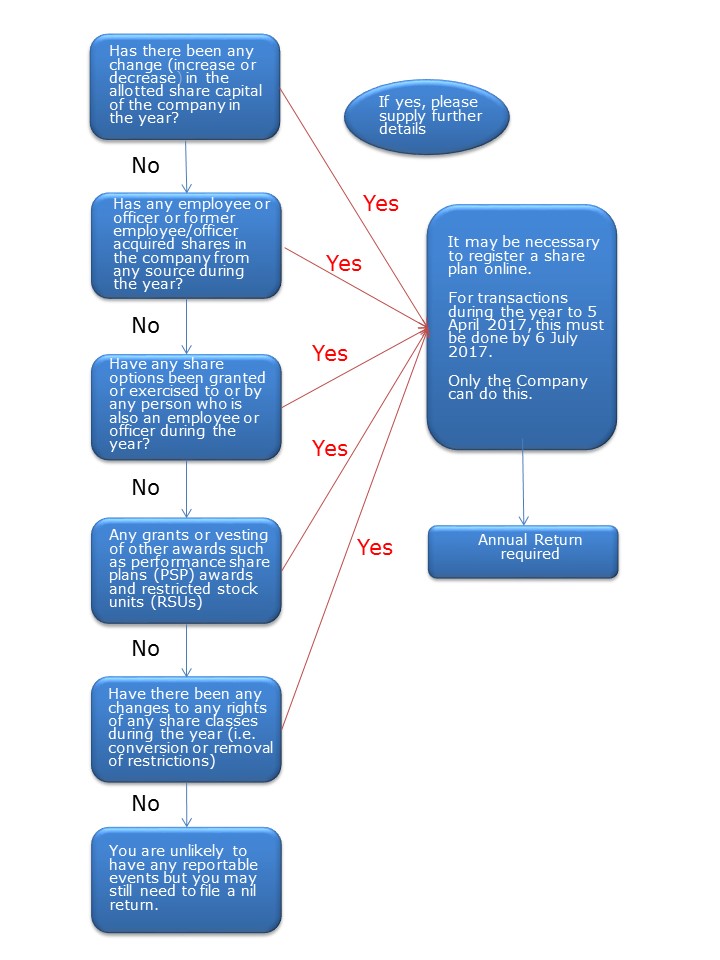

What is a reportable share transaction?

Please see below a flow chart of possible reportable events. If you have any doubts on whether there is a reportable event, please let us know so that we can advise you.

ERS Guidance FAQ

HMRC has released a series of Employment-Related Securities Bulletins which provide information and updates on developments relating to employment-related securities. In the 16th bulletin released in May 2014, HMRC outlines a number of common questions (with accompanying solutions) regarding the ERS online service:

1. Can I use any PAYE reference number?

2. I have two or more non-tax-advantaged share plans do I have to register each separately?

3. How do I correct an error made in naming a scheme?

If you experience any glitches and/or problems when registering a share plan or submitting annual returns, then please refer to HMRC’s ERS FAQs contained in the link below:

https://online.hmrc.gov.uk/information/faqs/ers or call HMRC ERS enquiries on tel: 03000 585 213 or for IT errors with the online system call 0300 200 3600.

How can we help you?

If you would like to appoint Mazars to act as your ERS agent please contact your usual Mazars relationship manager or one of our specialist share scheme experts:

Contact details:

Nationally: Liz Hunter, Head of Share Schemes

Tel: 020 7063 4489 or email Liz.Hunter@mazars.co.uk

London & South: David Lavelle, Manager, Scheme Schemes

Tel: 020 7063 4338 or email David.Lavelle@mazars.co.uk

Midlands & North: Ritchie Tout, Tax Director, Share Schemes

Tel: 0121 232 9627 or email Ritchie.Tout@mazars.co.uk

Please note that Mazars can only assist with the filing of returns and not with plan registration, and HMRC will not be sending out any reminders to companies.

Comments