The Election Paradox

Thought Leadership

The Election Paradox

Wed 11 Dec 2019

The election tomorrow is somewhat of a paradox. On the one hand, it has been dubbed “The most important election in decades”, one that can “shape the next generation”. On the other hand, however, it offers little visibility when it comes to UK portfolios.

Strange as it may seem, both statements might hold true.

Throughout the past few years, the British electorate has been steadfast in its request that the status quo should change. The parties have listened and have placed unconventional leaders at their helms. Both Conservative and Labour leaders can credibly promise that the United Kingdom of Great Britain and Northern Ireland will be a different place after December 13th.

The next government will oversee the biggest change in status quo the UK has seen in decades. The only question, for citizens and investors alike is what does this really mean, and how it addresses their uncertainties.

A Conservative win would mean more certainty about the structure of the economy, but uncertainty over trade with the EU, the country’s largest trading partner. A Labour win could mean more certainty over Europe (could is the operative word) but less certainty over the overall economy. The only thing the two parties agree on is willingness to incur higher deficits to spend money on the economy.

Investments, especially in real assets, such as factories or homes, tend to be illiquid and time-binding, which means that a certain degree of forward visibility is required. If one does not know either what one’s market is, or what the business climate will be, neither of which will be convincingly answered on the day after the election whatever the outcome, then one may defer of even cancel a big spending decision. Predictably, underinvestment has been a significant headwind for economic growth, especially in the past three years.

Nevertheless, one might argue, what if investors chose to believe and buy in early on electoral promises, hoping that either Conservatives will deliver the “Brexit dividend” and achieve a record-time trade deal with the EU, without compromising the UK’s integrity, or Labour will successfully demolish income and wealth inequalities that hamstring real growth and usher in an era of inclusive growth..

Even if that were the case, it would still leave long term investors in a bind. The UK economy is one of the most open systems in the world, its trajectory concomitant with the global economy. The world has been suffering from a slowdown mostly induced by the traumatic 2008 experience which has reduced demand for investments and consumption. Coupled with miserable demographics, surging trade tensions, crushing debt levels and a significant Chinese slowdown, it is no wonder why our time is often called “secular stagnation”, a pseudonym, for “Japanification”. Before 2008, the world was growing by 5%. Now, on a good year global growth is slightly above 3%. Add Brexit and business climate uncertainties into the mix and one can see how investors may only trust the strongest of investment cases. Any chink, or even potential chink in the armour is big enough doubt for portfolios facing a world that has barely been growing for a decade.

Even if the outcome of the election was certain, which we feel that due to tactical Remain voting and shifting electoral demographics (a third of British citizenship applications now come from EU nationals, as opposed to 12% before the election) is far from the case, fact remains that UK risk assets lack the forward visibility which would make them an iron-clad investment case for international portfolios. We thus feel that investors will stay on the sidelines until a comprehensive and realistic view of what the UK will look like in 10 years has emerged. Can this take place in January 2020? Maybe. But chances are the process, and thus the uncertainty, might be a bit longer than that.

Weekly Market Update: Sterling rallies on UK general election result

Read our full Market Update Market Update Sterling rallied last week after the Conservative Party won 365 seats in the UK general election, securing a majority of over 80. The Pound was up +1.5% vs the US Dollar and +0.9% vs the Euro, with the result being that although global stocks were up in local […]

Weekly Market Update: Major indices end the year on a positive note

Market Update Most major equity market indices ended the year on a positive note. Global stocks gained +0.2% in Sterling terms over the last two weeks of trading to close the year up +12.4% in Sterling terms. Over the year, due in large part to a Tech rally following the early pandemic crisis, US stocks […]

Weekly Market Update: Weak Week for Sterling

Market Update Major developed market equities gained in Sterling terms this week, due in large part to currency effects. Many of these indices actually fell in local currency. UK equities grew by +1.1% led by utilities and healthcare sectors. US stocks were up +0.4% in Sterling terms but had fallen -1.0% in local currency, this […]

Weekly Market Overview – Markets fear Taylorisation of Fed and trade wars

Markets continued their recent rocky period, with two separate events causing unease for investors. The first was Jay Powell’s first congressional testimony on Tuesday where he hinted at a faster pace of interest rate rises and stated a preference for rules based interest rate decisions. For example the Taylor Rule proscribes an interest rate for […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

Monthly Market Update: Markets unable to break out

Read our full Monthly Blueprint July 2018 Month In Review On the face of it, June has not been an exciting month for risk assets. Developed market stocks ended the month roughly in the same place as they started it, while long bond yields were little changed. However, beginning and end figures mask not only […]

Brexit Update: What now?

New Update! Monday 19 November 2018 After Friday’s dramatic cabinet session, which saw a third Brexit Secretary, Dominic Raab and Work & Pensions Secretary Esther McVeigh resign, there are several possible options on the table: 1) The deal might still go through parliament. Although divisions in the conservative party are high and it is unlikely that other […]

Weekly Market Update: Global stocks continue their rebound while Oil prices drop further and Brexit uncertainty heightens

Read our full Market Update Week 46 Market Update Global stocks continued their rebound this week, with both Global and European equities up +0.3%. Emerging Market equities led the pack, returning +2.5% as the slide in oil prices gave a boost to emerging market currencies. UK Stocks were hit by further Brexit volatility, hardest hit stocks […]

Weekly Market Update: Equities sell off on renewed trade war fears

Read our full Market Update Week 49 Market Update US equities sold off significantly last week, down -4.4% in Sterling terms, as trade war concerns weighed on American stocks, erasing the gains made in the previous week. Global equities were down -3.5% in Sterling terms, with all sectors apart from utilities experiencing negative returns. Emerging Market […]

Weekly Market Update: China concerns see market volatility

Read our full Market Update Week 50 Market Update Last week the main driver for UK investor returns was the weakness in Sterling, which fell -1.1% vs USD and -0.5% vs EUR. The majority of the drop came on Friday as Theresa May’s inability to win concessions from the EU created further uncertainty about the future […]

Weekly Market Update: Global equities rally, Sterling depreciates as likelihood of a no-deal increases

Market Analysis This week saw strong equity market returns, with global stocks up +2.0% in Sterling terms. US equities were up +2.6% for the week, with returns enhanced by Sterling depreciation versus the US Dollar and earnings outperformance from both Google and Starbucks. UK, European and Japanese equities were up +0.6%, +1.1%, and +0.5% respectively. […]

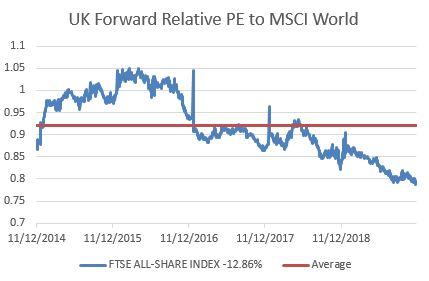

Are UK risk assets pricing in the possibility of political realignment?

UK assets continue to trade at a discount to the rest of the world, however, with so much political uncertainty facing the UK this may be justified. Boris Johnson’s new special adviser Dominic Cummings is by all means unorthodox. Mr. Cummings was the Campaign Director for Vote Leave in 2016, and used machine learning and data […]

Weekly Market Update: Global markets rally amid Brexit uncertainty

Read our full Market Update Week 36 Market Update Global stocks were up last week, gaining +1.9% in local terms and +0.9% in Sterling terms as the Pound appreciated after the House of Lords passed a bill giving parliament the power to, in theory, prevent a no-deal Brexit. In addition to this, the Prime Minister […]

Weekly Market Update: Global stocks gain in local currency terms, Oil rallies on drone attack

Read our full Market Update Week 37 Market Update Global stocks were down -0.2% last week in Sterling terms and up +1.3% in local currency terms as Sterling appreciated versus other major currencies as Boris Johnson adopted a softer stance on the Irish border; increasing the likelihood of a deal being reached before the October […]

Weekly Market Update: Bond yields rise, Pound rallies on potential Brexit “pathway”

Read our full Market Update Week 40 Global stocks gained throughout the week in local terms, however they fell in Sterling terms after the Pound rallied on news of a potential “pathway” to a Brexit deal. Global stocks fell -1.5% in Sterling terms, with the decline led by weak performance from US and Japanese equities; […]

Weekly Market Update: Sterling Strength Erodes Equity Gains

Market Update A generally positive week for equities in local currency terms was slightly negative in Sterling terms as markets became increasingly optimistic about a UK trade deal with the EU, sending the Pound higher. UK equities were the notable exception for the week, though down only -0.1%. Overall, global stocks gained +1.7% in local […]

Weekly Market Update: Stocks gain globally, Sterling back below 1.30 vs Dollar

Read our full Market Update Week 43 Market Update Global stocks were up in both local currency and Sterling terms last week, however due to a fall in the currency versus other major currencies, Sterling-based investors enjoyed a greater gain; global equities were up +2.1% in Sterling terms and +1.3% in local terms. US stocks […]

Monthly Market Update: New Equity Highs as Economies Tread Water

Markets welcomed signs of an easing in geopolitical tensions in October, with risk assets generally outperforming traditional safe havens. The US and Chinese authorities moved closer to agreeing a partial deal on trade, while the UK once again edged back from the precipice of a no-deal Brexit. Global central banks reiterated their dovish stances and […]

Weekly Market Update: Sterling depreciation buoys Global Equities, bond yields fall

Global stocks were down -0.4% in local currency terms last week, however returns for UK investors were +0.3% after Sterling depreciated versus major global currencies, down -0.5% and -0.3% versus the US Dollar and the Euro respectively. US, UK and European stocks returned +0.3%, +0.4% and -0.3% over the week, whilst Emerging Markets equities posted […]

Weekly Market Update: Stocks trade higher on US jobs numbers, Sterling gains versus Dollar and Euro

Read our full Market Update Market Update A second straight week of strong performance for Sterling, up +1.7% vs the US Dollar and +1.2% vs the Euro as markets further priced in a Conservative victory at the coming General Election, once again mean that although global stocks were up in local terms, UK investors experienced […]

Weekly Market Update: Global stocks continue their climb, Sterling declines

Read our full Market Update Market Update Global stocks posted strong gains last week, up +1.3% in local currency terms and +3.7% in Sterling terms after the Pound depreciated versus other major currencies. Sterling fell shortly after the UK general election when Boris Johnson signalled the UK will leave the EU with or without a […]

Q1 2020 Outlook

Read our Full Quarterly Outlook The Power of the Cycle John Kenneth Galbraith, an irreverent but brilliant economist best known for his work on the Great Crash of 1929, famously lamented about his own profession: “the only function of economic forecasting is to make astrology look respectable”. As always, we toyed with the idea that […]

Tinker, Tailor, Soldier… Huawei?

This is a multi-level chess game, touching politics, intelligence and trade, and a move in each field directly affects the other two.

Q1 Quarterly Investment Outlook: 2020: The Power of the Cycle

Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7% in local currency terms. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservative’s decisive general election victory. The late final rally was primarily driven by renewed optimism for a ‘phase one’ trade deal between the US and China, and left global equities up 25% for the year. It is of course important to note that, by contrast, markets ended 2018 in very pessimistic mood as the Fed continued to raise interest rates, and therefore a global equity return figure of around 8% from September 2018 is a more useful measure of equity returns.

Three Burning Questions for Investors

In the past few weeks, we have been experiencing a flurry of better-than-expected economic data, especially in the US, while global equities remained near the recent high levels they have been trading at for almost a month. A casual read of the situation could be that the markets had run ahead of themselves, and as […]

Quarterly Investment Outlook Q3 2020: Covid Recovery and Anxiety

A quarterly report is not normally a difficult document to put together. Usually it consists of an account of the trending state of affairs, the more possible outcomes and risks to those outcomes. In the past few years, these reports were actually made easier. The US Federal Reserve was underwriting risk at such an unprecedented scale, nearly unwavering for more than a decade, in a manner which suppressed all major hazards to the economy and financial markets. Ever since 2010 the question, repeatedly, had been: “With opportunity costs driven down so much for so long, whatever can bring markets down?”

Weekly Market Update: Stock markets post mixed returns on virus fears

Please read our full Market Update Market Update Stocks posted mixed returns last week, with strong performance in the US as the NASDAQ 100 set new record highs, while UK and Japanese stocks closed down -0.9% and -1.8% in Sterling terms respectively. Emerging Market stocks performed well, gaining +2.4% for the week. Technology, Telecoms and […]

Weekly Market Update: Brexit Tempers Vaccine Regulatory Headwinds

Market Update Like clockwork positive vaccine news, this time FDA confirmation of Pfizer/BioNTech results, buoyed markets in the early part of last week. However some of these gains were reversed due to the worsening condition of both Brexit and Covid-19 cases. UK equities were flat for the week, however more domestically exposed mid-caps fell as […]

Bargain Basement Britain

Over the last month global equity markets have sold off; since the 15th of January the MSCI AC World Index has fallen -4.12%, the S&P 500 -4.22% and the Japanese Nikkei -6.0%. The UK market similarly has tumbled with the FTSE 100 plummeting -6.36% over the last 4 weeks1. With stocks cheaper compared to a […]

Comments