Three Burning Questions for Investors

Thought Leadership

Three Burning Questions for Investors

Thu 09 Jul 2020

In the past few weeks, we have been experiencing a flurry of better-than-expected economic data, especially in the US, while global equities remained near the recent high levels they have been trading at for almost a month. A casual read of the situation could be that the markets had run ahead of themselves, and as the economy is now repairing stocks are taking their customary summer breather in anticipation of better data. However, we believe the situation is a bit different.

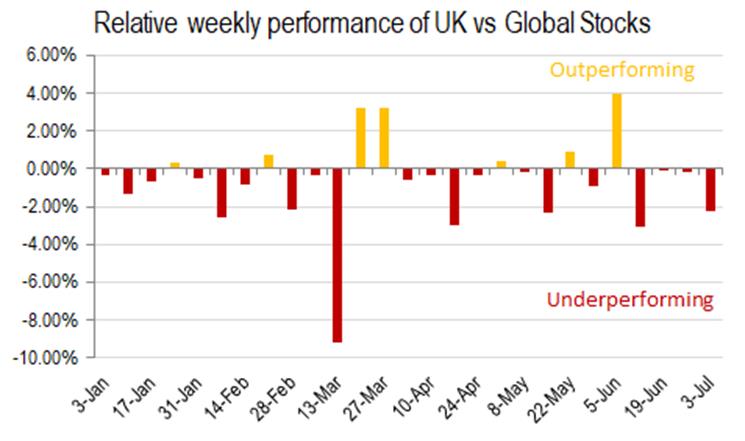

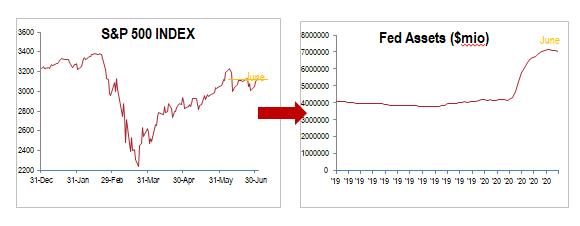

Global stocks peaked in the second week of June and are trading at roughly those levels for a month. Not incidentally, in the same week we observed that Fed balance sheet assets had peaked. Thereafter, the Fed, which had been buying mostly short-term securities it can easily let expire, has reduced its $7.16tr balance sheet by about $160 billion. Thus, as new money stopped flowing, stocks stopped climbing, in line with our longer-term view that asset reflation, not fundamentals, are driving this market. Meanwhile, we observed another bad week for UK risk assets, with UK large caps now 18% below the MSCI World since the beginning of the year – in same currency terms. UK stocks have underperformed their global counterparts in every week but seven, throughout the entire year so far.

We believe that now investors are faced with three key questions that need answering:

- Will the economic recovery happen faster than we expect?

- Have stocks peaked or will the Fed press on with purchases?

- Why are UK stocks underperforming so much?

The jury is still out on all three questions, so all we can offer is our own perspective.

Economy – No “V” just yet

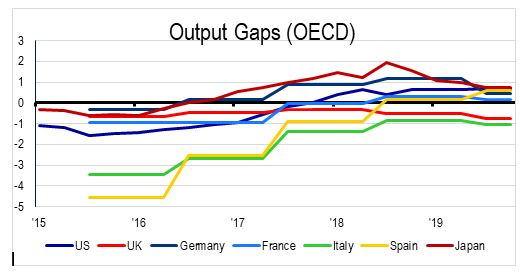

We believe that the economic rebound we saw in June is evidence of pent up demand, not a full swing back up. PMI data suggest that new orders are weak and companies are mostly working off their previous backlogs. Additionally, OECD data suggests a lot of slack in all economies, thus productivity is bound to remain low. Unemployment pressures are bound to increase as government funding for companies is scaled back. While China has performed admirably since the end of its lockdown, we see that production is tepid. Japan, which is China’s closest trading partner and a dependable gauge on the Chinese economy, continues to see a sharp contraction in factory output and orders, suggesting that demand pressures are bound to continue. Global trade conditions were tepid before we entered this crisis, and they are not expected to abate as the US Presidential Election season enters the final stretch. On top of all these, while we acknowledge that the virus narrative has changed for the better, we are also cognisant of the fact that where many policy decisions were made out of panic, now they are made out of Covid-fatigue. None of these can avert a second wave of massive infections, and thus renewed lockdowns. We would thus be very careful with the data, lest we see persisting evidence that the rebound has strong legs.

Fed Takes a Breather – So Do Stocks

For the better part of the last decade, the main driver of demand for risk assets had been cheap money lowering risks and opportunity costs for investors. It is natural for the Federal Reserve to taper purchases at this point. After all, we just witnessed the fastest hike in Fed assets in history. At this point, we see no evidence of a sharp contraction in asset purchases, and neither do the markets, or else we would have certainly witnessed a rout in global stocks. The Fed is very careful to communicate its intentions, and the current message is that “we can do a lot more than this”, an equivalent to the more historic “whatever it takes”. As long as markets don’t see evidence of a “stealth” quantitative tightening, a huge surprise right now, we believe that the drawdown in asset purchases will be short lived. If, by this time next year, company profitability has been restored to long-term trends, it is then that the markets could possibly countenance some further reductions in the Fed Balance Sheet. The $7trm mark, to which we are very close, could be a trigger for traders to watch.

UK Underperformance

There’s no clear narrative or consensus why UK risk assets are shunned by investors. We could be, thus, looking at a confluence of factors. We believe that the two biggest factors are:

a) an aversion to high dividend stocks

b) renewed Brexit worries

Despite low bond yields, investors have been shunning high dividend stocks, mainly due to concerns about dividend viability in 2020. Yields are calculated on last year’s dividend. With many UK companies having taken government furlough money, it stands to reason that a lot of dividends for shareholders may be partly or wholly slashed.

As far as Brexit is concerned, it was in the beginning of the crisis the expectation of investors that it would again be deferred until the European continent was stabilised. Investors, who are now more risk averse than in January are extra careful.

There are of course additional factors in play. The UK has seen the highest Covid infection rate in the world, with policy subject to a lot of criticism. Additionally, UK indices are heavily weighed by industries that haven’t really performed well during this downturn, like oil, banks and insurance. Finally, the UK economy seems to be suffering a bit more than its global counterparts, partly because it’s more sensitive to the global trade breakdown and partly –or maybe due to trade issues- because it has been experiencing more intense supply chain pressures.

A lot of these factors are transitory, but there are some legitimate long term worries for markets. While Covid will eventually pass, some cyclicals will inevitably rebound at some point, as will the currency when the road to Brexit becomes again clearer and dividends may well be reinstated in 2021, we need to acknowledge that the extent of the damage of this period to the British economy is yet to be accounted for, and thus those more long-term investors could wait for a significant period before they decide to up their weights in the UK again.

Weekly Market Update: Brexit Tempers Vaccine Regulatory Headwinds

Market Update Like clockwork positive vaccine news, this time FDA confirmation of Pfizer/BioNTech results, buoyed markets in the early part of last week. However some of these gains were reversed due to the worsening condition of both Brexit and Covid-19 cases. UK equities were flat for the week, however more domestically exposed mid-caps fell as […]

Weekly Market Update: Stock markets post mixed returns on virus fears

Please read our full Market Update Market Update Stocks posted mixed returns last week, with strong performance in the US as the NASDAQ 100 set new record highs, while UK and Japanese stocks closed down -0.9% and -1.8% in Sterling terms respectively. Emerging Market stocks performed well, gaining +2.4% for the week. Technology, Telecoms and […]

Weekly Market Update: Consumer-Led Recovery at Close to Fastest Pace in Modern History

Once again many major equity markets finished the week not far from where they started. Market attention was squarely focused on the Federal Reserve, where chairman Jerome Powell promised not to raise rates in the near term; as a consequence, markets did not sharply react in either direction. US equities were flat in US Dollar terms, but up +0.2% in Sterling terms. UK equities were the best performing region, up +0.5% last week. European equities fell for the second consecutive week, down -0.8% in Sterling terms. Emerging markets fell -0.2% in Sterling terms. Japan was the clear laggard, where earnings failed to meet expectations and the Bank of Japan kept policy unchanged. Japanese equities fell -1.9% in Sterling terms. The US 10Y yield rose on improved economic data, up 6.8bps to 1.6%, while the UK 10Y rose 9.8bps to 0.8%. Gold fell -0.3% on the week. The better than expected economic data helped oil to rise +2.4% last week to $64.4.

Weekly Market Update: Global stocks continue their rebound while Oil prices drop further and Brexit uncertainty heightens

Read our full Market Update Week 46 Market Update Global stocks continued their rebound this week, with both Global and European equities up +0.3%. Emerging Market equities led the pack, returning +2.5% as the slide in oil prices gave a boost to emerging market currencies. UK Stocks were hit by further Brexit volatility, hardest hit stocks […]

Weekly Market Update: Bond yields rise, Pound rallies on potential Brexit “pathway”

Read our full Market Update Week 40 Global stocks gained throughout the week in local terms, however they fell in Sterling terms after the Pound rallied on news of a potential “pathway” to a Brexit deal. Global stocks fell -1.5% in Sterling terms, with the decline led by weak performance from US and Japanese equities; […]

Weekly Market Update: Weak Week for Sterling

Market Update Major developed market equities gained in Sterling terms this week, due in large part to currency effects. Many of these indices actually fell in local currency. UK equities grew by +1.1% led by utilities and healthcare sectors. US stocks were up +0.4% in Sterling terms but had fallen -1.0% in local currency, this […]

Weekly Market Update: Global stocks gain in local currency terms, Oil rallies on drone attack

Read our full Market Update Week 37 Market Update Global stocks were down -0.2% last week in Sterling terms and up +1.3% in local currency terms as Sterling appreciated versus other major currencies as Boris Johnson adopted a softer stance on the Irish border; increasing the likelihood of a deal being reached before the October […]

Weekly Market Update: Global markets rally amid Brexit uncertainty

Read our full Market Update Week 36 Market Update Global stocks were up last week, gaining +1.9% in local terms and +0.9% in Sterling terms as the Pound appreciated after the House of Lords passed a bill giving parliament the power to, in theory, prevent a no-deal Brexit. In addition to this, the Prime Minister […]

Are UK risk assets pricing in the possibility of political realignment?

UK assets continue to trade at a discount to the rest of the world, however, with so much political uncertainty facing the UK this may be justified. Boris Johnson’s new special adviser Dominic Cummings is by all means unorthodox. Mr. Cummings was the Campaign Director for Vote Leave in 2016, and used machine learning and data […]

Weekly Market Update: Global equities rally, Sterling depreciates as likelihood of a no-deal increases

Market Analysis This week saw strong equity market returns, with global stocks up +2.0% in Sterling terms. US equities were up +2.6% for the week, with returns enhanced by Sterling depreciation versus the US Dollar and earnings outperformance from both Google and Starbucks. UK, European and Japanese equities were up +0.6%, +1.1%, and +0.5% respectively. […]

Weekly Market Update: China concerns see market volatility

Read our full Market Update Week 50 Market Update Last week the main driver for UK investor returns was the weakness in Sterling, which fell -1.1% vs USD and -0.5% vs EUR. The majority of the drop came on Friday as Theresa May’s inability to win concessions from the EU created further uncertainty about the future […]

Weekly Market Update: Equities sell off on renewed trade war fears

Read our full Market Update Week 49 Market Update US equities sold off significantly last week, down -4.4% in Sterling terms, as trade war concerns weighed on American stocks, erasing the gains made in the previous week. Global equities were down -3.5% in Sterling terms, with all sectors apart from utilities experiencing negative returns. Emerging Market […]

Monthly Market Update: Markets unable to break out

Read our full Monthly Blueprint July 2018 Month In Review On the face of it, June has not been an exciting month for risk assets. Developed market stocks ended the month roughly in the same place as they started it, while long bond yields were little changed. However, beginning and end figures mask not only […]

Brexit Update: What now?

New Update! Monday 19 November 2018 After Friday’s dramatic cabinet session, which saw a third Brexit Secretary, Dominic Raab and Work & Pensions Secretary Esther McVeigh resign, there are several possible options on the table: 1) The deal might still go through parliament. Although divisions in the conservative party are high and it is unlikely that other […]

Monthly Market Update: New Equity Highs as Economies Tread Water

Markets welcomed signs of an easing in geopolitical tensions in October, with risk assets generally outperforming traditional safe havens. The US and Chinese authorities moved closer to agreeing a partial deal on trade, while the UK once again edged back from the precipice of a no-deal Brexit. Global central banks reiterated their dovish stances and […]

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

Monthly Market Outlook: May 2018

Read our full Monthly Market Update Following two months of negative returns for risk assets, equities rallied in April as trade war fears were downplayed and positive earnings, especially in the US, continued to come through. The month was also notable in that markets sold off over fears of an escalation of the Syria conflict, […]

Monthly Market Outlook: April 2018

Read our Monthly Market Update After February ended a run of 11 consecutive months of positive, less volatile returns for equities, March saw risk assets continue to suffer as US bond yields peaked near 3% and fears of a global trade war came closer to fruition, with President Trump placing tariffs on Chinese imports of steel […]

Monthly Market Outlook: March 2018

Read our Monthly Market Update February saw the return of volatility for stocks after nearly two years, as a confluence of catalysts affected equity markets: US Bond yields breaking critical levels above 2.55%, a new more hawkish and uncertain Fed, the deterioration of the global trade climate and renewed political uncertainty in Europe and the UK. […]

Weekly Market Overview – Markets fear Taylorisation of Fed and trade wars

Markets continued their recent rocky period, with two separate events causing unease for investors. The first was Jay Powell’s first congressional testimony on Tuesday where he hinted at a faster pace of interest rate rises and stated a preference for rules based interest rate decisions. For example the Taylor Rule proscribes an interest rate for […]

Bargain Basement Britain

Over the last month global equity markets have sold off; since the 15th of January the MSCI AC World Index has fallen -4.12%, the S&P 500 -4.22% and the Japanese Nikkei -6.0%. The UK market similarly has tumbled with the FTSE 100 plummeting -6.36% over the last 4 weeks1. With stocks cheaper compared to a […]

Monthly Market Outlook: February 2018

Read our Monthly Market Update Global equity markets were positive again, registering a 5.3% performance in January, benefiting from the positive sentiment and the passing of the US tax reform at the end of 2017. The macroeconomic environment was less supportive, however, as some key indicators suggested that global economic momentum was slowing down in […]

Weekly Market Update: Stocks gain globally, Sterling back below 1.30 vs Dollar

Read our full Market Update Week 43 Market Update Global stocks were up in both local currency and Sterling terms last week, however due to a fall in the currency versus other major currencies, Sterling-based investors enjoyed a greater gain; global equities were up +2.1% in Sterling terms and +1.3% in local terms. US stocks […]

The Election Paradox

The election tomorrow is somewhat of a paradox. On the one hand, it has been dubbed “The most important election in decades”, one that can “shape the next generation”. On the other hand, however, it offers little visibility when it comes to UK portfolios. Strange as it may seem, both statements might hold true. Throughout […]

Weekly Market Update: Sterling depreciation buoys Global Equities, bond yields fall

Global stocks were down -0.4% in local currency terms last week, however returns for UK investors were +0.3% after Sterling depreciated versus major global currencies, down -0.5% and -0.3% versus the US Dollar and the Euro respectively. US, UK and European stocks returned +0.3%, +0.4% and -0.3% over the week, whilst Emerging Markets equities posted […]

Quarterly Investment Outlook Q3 2020: Covid Recovery and Anxiety

A quarterly report is not normally a difficult document to put together. Usually it consists of an account of the trending state of affairs, the more possible outcomes and risks to those outcomes. In the past few years, these reports were actually made easier. The US Federal Reserve was underwriting risk at such an unprecedented scale, nearly unwavering for more than a decade, in a manner which suppressed all major hazards to the economy and financial markets. Ever since 2010 the question, repeatedly, had been: “With opportunity costs driven down so much for so long, whatever can bring markets down?”

Weekly Market Update: Major indices end the year on a positive note

Market Update Most major equity market indices ended the year on a positive note. Global stocks gained +0.2% in Sterling terms over the last two weeks of trading to close the year up +12.4% in Sterling terms. Over the year, due in large part to a Tech rally following the early pandemic crisis, US stocks […]

Weekly Market Update: Sterling Strength Erodes Equity Gains

Market Update A generally positive week for equities in local currency terms was slightly negative in Sterling terms as markets became increasingly optimistic about a UK trade deal with the EU, sending the Pound higher. UK equities were the notable exception for the week, though down only -0.1%. Overall, global stocks gained +1.7% in local […]

Weekly Market Update: UK Equities on Track for Second-Best Month on Vaccine Rally

Market Update Once again vaccine optimism supported global equity markets; this time it was the turn of the AstraZeneca vaccine, which can be more readily stored and transported. Global equities rose +2.1% for the week in Sterling terms. Financials and Energy were the two best performing sectors, as both sectors would benefit greatly from a […]

Weekly Market Update: Lockdowns and US Election Raise Market Volatility

Market Update Global equities suffered their worst week since March, with the sell-off attributed to renewed virus related lockdowns across most of Europe and the final stretch of the hotly contested US presidential campaign. Global and US equities were both down -5.0%. This was despite the fact that Tech giants Alphabet, Amazon, Apple and Facebook […]

Another Covid meltdown. What investors should know

For the first time since March, the Coronavirus narrative is truly gripping markets.

Weekly Market Update: Increasing Likelihood of US Government Trifecta Lifts Equity Markets

Read our Full Weekly Market Update Market Update A reduction in uncertainty in the United States helped US equities to their best week in three months, up +3.2% in Sterling terms, as investors begin to price in a Biden presidential victory. UK stocks looked past weaker than anticipated GDP growth to rally +2.0%. Investors appeared […]

Weekly Market Update: Increasing COVID-19 case count caps equity market rally

Read our full Market Update Market Update Global equities traded higher last week, up +0.5% in Sterling terms. US equities climbed +0.9% with housebuilders, buoyed by promising housing data, leading the way. Other developed markets did not fare as well. UK and European stocks were down -1.3% and -1.1% respectively, driven by both the negative […]

Weekly Market Update: Equity Markets Rebound, Gold continues to soar

Read our Full Market Update Market Update Bucking the trend of two consecutive weeks of falling equity markets, all major indices were positive last week. Global equities gained +2.7% in Sterling terms, with the Nasdaq Composite reaching new highs, and the S&P 500 now close to its February peak. After a poor week last week, […]

Weekly Market Update: Technology stocks push equity markets higher

Please read our full Market Update Market Update Stock markets closed up last week, with the technology-heavy NASDAQ 100 even reaching an all-time high. Cyclical sectors such as Oil and Financials lagged as economic conditions remain weak and second wave fears continue to build, with increased use of local lockdowns. The rally in risk assets […]

Weekly Market Update: Indian Covid Crisis Captures Attention of Markets

Equity markets ended the week largely unchanged, with the largest movements seen in Japanese and UK stocks. UK equities fell -1.1%, driven in part by a falling oil price, as the global economic outlook increasingly uncertain, with clear inequality in the vaccination progress between regions, dampening expected demand for oil. US equities fell -0.3% in Sterling terms, with plans to raise capital gains tax only making a slight impact on US markets. European equities rose +0.2% in Sterling terms due to currency effects, having fallen -0.4% in local currency terms. Emerging markets were the only risers in local currency terms, and were up +0.1% in Sterling terms. Globally the best performing sector was healthcare, whilst energy was the worst performing. The US 10Y yield fell slightly by 2.2 bps to 1.6%, while the UK 10Y fell 2 bps to 0.7%. Gold fell -0.2% on the week. Oil fell as the economic outlook deteriorated, down -1.7% on the week to $62.1.

WEEKLY MARKET UPDATE: Markets fall on second wave fears, gloomy Fed

Read our full Market Update Market Update The rally in risk assets came to a grinding halt last week on fears of a second wave of infections in the US, with virus rates up in many states, and the Federal Reserve offering up a gloomy economic outlook. Stocks are also down this morning on news […]

Is market optimism justified?

I struggle with the idea how news that nothing has changed in my chances of survival from a killer disease that was enough to lock the whole world down, is enough to send the world’s biggest companies trading at eye-watering 22.6x earnings (the average is around 15-16). It seems to me more credible that the market is running on excessive amounts of QE

Stocks fall across the globe as COVID-19 cases climb, Oil prices drop as Russia refuses supply cuts

Please check out our full Market Update Week 10 Market Update UK equities were down nearly 9% this morning, with the natural resource and banking heavy indices experiencing weakness for three prime reasons. First, coronavirus fears continued to rise as Italy quarantined 16 million residents, with investors fearful of this impact on the global economy […]

Weekly Market Update: Stocks decline on COVID-19 fears, Bonds and Gold rally

Read our full Market Update Week 8 Market Update Fears that COVID-19 could weigh on consumption and global growth increased last week as the number of cases spiked in both Iran and Italy. Concerns that the virus could impact critical global supply chains have increased, with tech titan Apple widening their earnings estimates given the […]

Q1 Quarterly Investment Outlook: 2020: The Power of the Cycle

Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7% in local currency terms. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservative’s decisive general election victory. The late final rally was primarily driven by renewed optimism for a ‘phase one’ trade deal between the US and China, and left global equities up 25% for the year. It is of course important to note that, by contrast, markets ended 2018 in very pessimistic mood as the Fed continued to raise interest rates, and therefore a global equity return figure of around 8% from September 2018 is a more useful measure of equity returns.

Tinker, Tailor, Soldier… Huawei?

This is a multi-level chess game, touching politics, intelligence and trade, and a move in each field directly affects the other two.

Q1 2020 Outlook

Read our Full Quarterly Outlook The Power of the Cycle John Kenneth Galbraith, an irreverent but brilliant economist best known for his work on the Great Crash of 1929, famously lamented about his own profession: “the only function of economic forecasting is to make astrology look respectable”. As always, we toyed with the idea that […]

Weekly Market Update: Global stocks continue their climb, Sterling declines

Read our full Market Update Market Update Global stocks posted strong gains last week, up +1.3% in local currency terms and +3.7% in Sterling terms after the Pound depreciated versus other major currencies. Sterling fell shortly after the UK general election when Boris Johnson signalled the UK will leave the EU with or without a […]

Weekly Market Update: Sterling rallies on UK general election result

Read our full Market Update Market Update Sterling rallied last week after the Conservative Party won 365 seats in the UK general election, securing a majority of over 80. The Pound was up +1.5% vs the US Dollar and +0.9% vs the Euro, with the result being that although global stocks were up in local […]

Markets sell-off at fastest pace since 2011

By David Baker, Chief Investment Officer After a strong start of the year for equity markets, global stocks shed almost 5% of their value on Friday and Monday. US equities are now 6.2% below their highs, turning negative for the year, as are global equities (-6.5% from their highs). The S&P 500 is now trading […]

Comments