Is market optimism justified?

Thought Leadership

Is market optimism justified?

Mon 04 May 2020

Douglas Adams once wrote: “This planet has a problem, which is this: most of the people living on it are unhappy for pretty much of the time. Many solutions were suggested for this problem, but most of these are largely concerned with the movement of small green pieces of paper, which is odd because on the whole it isn’t the small green pieces of paper that are unhappy.”

Last week, the S&P 500 jumped to nearly 3000 points on news that Remdesivir, an Ebola drug that may be used to fight Covid-19, passed some clinical trials with success. So far so good. Then I read the BBC article on the tests themselves. The clinical trials suggested that Remdesivir indeed helps, by cutting the symptoms from 15 days to 11, which is still important because this means it may stop it from developing into something really bad. However, 8% of the patients who received it lost their lives, as opposed to 11% in the control group, which is not statistically significant.

Now I am not a science expert. The US NIAID (National Institute of Allergy and Infectious Diseases) director Anthony Fauci said at an Oval Office meeting Wednesday, the study results were “a very important proof of concept.”, and Mr. Fauci is an honourable man.

Of course I am slightly worried that the Centre for Disease Control (the world famous CDC) is not taking point on this and that the pandemic has been wildly politicised in Washington. But Mr. Fauci is an honourable man.

I’m also generally skeptical of medical advice coming out of the Oval Office these days (DON’T…INJECT….BLEACH). But surely Mr. Fauci is an honourable man.

The conundrum

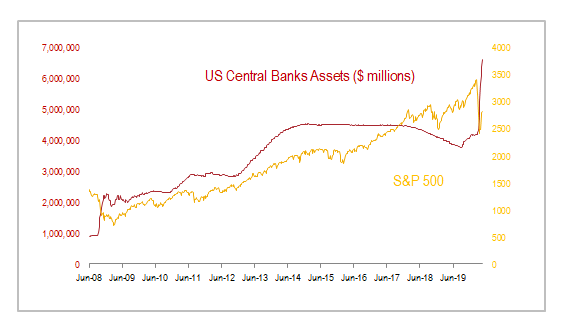

However, I struggle with the idea how news that nothing has changed in my chances of survival from a killer disease that was enough to lock the whole world down, is enough to send the world’s biggest companies trading at eye-watering 22.6x earnings (the average is around 15-16). It seems to me more credible that the market is running on excessive amounts of QE and looking for any good narrative to justify this. After all, the Federal Reserve alone has raised its asset base by $2.9tr since September, from $3.8 to $6.7tr, a 76% rise, and other central banks are following suite. Meanwhile, analysts have moved their FY2020 earnings predictions squarely into FY2021, an FY2021 into FY2022, so we treat 2020 as an aberration with no real long-term repercussions, especially for larger caps.

What investors need to know

And all that is ok, but let’s call a spade a spade, and think of what this means for portfolios and risk assets. So here’s what I do know, and the conversation I would have with my clients. When buying stocks, we are not participating in a company’s earnings any more, at least not this year. We are participating in a Pavlovian game of money printing where we are not trying to guess what will happen to the economy but rather when Pavlov (the central banker) will blow blow his whistle again and flood the market with money. Again, this is not a bad thing (except if one is studying for the CFA in which case my condolences for spending three years reading fat tomes of what is currently as relevant to investment as classical poetry). Since 2009 the MSCI World is up almost three times, beating real economic growth by a lot. Number 1, financial markets provide answers that real economy investments can’t and it’s good to participate in them. More than ever, financial investment is the only game in town.

However, there will be long term repercussions. It is evident that since 2008 Capitalism has gone into survival mode, and solutions aim at saving financial markets, not efficiently allocating assets, which is the purpose of any economic system. Inequalities have risen and are bound to rise more after this Covid episode has passed. The fact that the state will sponsor the real economy as much as it has been sponsoring the financial economy for the next few years, means that there will be less opportunities for new and bright companies to take the place of the redundant and failing ones. The liberal “creative destruction”, the saving grace of capitalism and its “raison d’etre” which helps spread the wealth to those more worthy, is being shut down by indiscriminate government aid to those in need, whether deserving or not. We are trying to solve a big problem by moving green pieces of paper around (money) and this is not a long term solution. If one is not found soon, then Liberal Capitalism will face the same existential problems Communism faced in the 80’s and permatransform to a China-like less efficient and liberal form, clashing with democratic principles and our way of life. So Number 2, know that more political upheaval may be at the end of this, especially by multitudes who don’t have many financial assets.

After mortally wounding Benjamin Graham and value investing (the idea that long term fundamentals will trample market inefficiencies), QE is taking a swing at Harry Markowitz and his portfolio investing principles. The basic idea of asset allocation is still intact of course (buy things that don’t move together to reduce volatility, and benefit from an underlying capitalistic trend which over time sends all risk assets up) which is why we tell clients that now more than ever it is a good thing to do. The problem with all the money printing is that it increases correlations between assets (stocks=up, bonds=up, gold=up) which makes it difficult to find decorrelated assets for portfolios to work better, except for cash and cash-like instruments. Upside volatility of course was never a concern, but we might see (cont.) more bouts of what we experienced in March. So, Number 3, on the one hand everything goes up with turbo-charged QE, which is good and why we should hold portfolios of financial assets, but on the other we are less protected by a spike in volatility, so it is more imperative than ever to have cash pots readily available for clients in drawdowns.

PS. Theory is all well and good, but theories need to change and adapt to our times. In the next few years I’d expect to see a new Graham, a new Markowitz and even a new Keynes and a Friedman if capitalism is to survive inequality, low growth and very high debt. All of us financial professionals should keep an eye on academia for new solutions and start clearing out our libraries…

Another Covid meltdown. What investors should know

For the first time since March, the Coronavirus narrative is truly gripping markets.

Weekly Market Update: Technology stocks push equity markets higher

Please read our full Market Update Market Update Stock markets closed up last week, with the technology-heavy NASDAQ 100 even reaching an all-time high. Cyclical sectors such as Oil and Financials lagged as economic conditions remain weak and second wave fears continue to build, with increased use of local lockdowns. The rally in risk assets […]

Monthly Market Update – December 2018

Read our full Monthly Market Update December 2018 November data indicated that the global economy continues to slow, despite a pick up in the services sector, as trade conditions deteriorate. Risk asset divergence, a theme of the previous quarter, seems to have abated, as US risk asset underperformance closed part of the gap with Europe and […]

Volatility, a guest star?

Read our full Monthly Market Update February 2020 The month in review: Coronavirus fears weigh on equity markets Despite a positive start to the year, January was a negative month for risk assets. Earnings marginally outperformed expectations in the US, with Amazon and Apple rallying on stronger than expected revenue growth and J.P. Morgan posting […]

Q1 2020 Outlook

Read our Full Quarterly Outlook The Power of the Cycle John Kenneth Galbraith, an irreverent but brilliant economist best known for his work on the Great Crash of 1929, famously lamented about his own profession: “the only function of economic forecasting is to make astrology look respectable”. As always, we toyed with the idea that […]

Mazars Wealth Management Investment Newsletter – Winter 2020

Read our full MWM Investment Newsletter Winter 2020 Following a flat third quarter, global equities rallied to the end of the year with the MSCI World index up over 7%. Returns for unhedged Sterling based investors were broadly flat as the Pound strengthened following the Conservatives’ decisive general election victory. The late final rally was […]

Weekly Market Update: Markets Rattled by Iran Tensions

Read our full Market Update Market Update U.S. stocks declined modestly last week, after a sharp rally at year-end and a new record high on the first trading day of the year, as tensions rose between the US and Iran following an airstrike in Iraq that killed a prominent Iranian general. US equities were down […]

Investment Team Holiday Reading List

With Christmas Day just around the corner the Investment Team have compiled a business/economics themed reading list for those looking for a quick stocking filler. Below is a book recommendation from each of us, and a few sentences explaining why you should rush out to your local bookshop, or if it is too cold out, add […]

Monthly Market Update: New Equity Highs as Economies Tread Water

Markets welcomed signs of an easing in geopolitical tensions in October, with risk assets generally outperforming traditional safe havens. The US and Chinese authorities moved closer to agreeing a partial deal on trade, while the UK once again edged back from the precipice of a no-deal Brexit. Global central banks reiterated their dovish stances and […]

Monthly Market Update:A recession nearing?

Read our full Monthly Market Blueprint Sept 2019 •Global economic data continue to indicate contraction in global manufacturing and a slowdown in services. The US has joined the cohort of large countries which now see their economy slow. Inflation remains at bay and unemployment in developed markets is near all-time lows. Yet consumption is dented […]

Quarterly Outlook: Sustainomics and a world without QE

2022 is the year where QE (conceivably) ends, and a decade-long Sustainability theme begins. Read our annual outlook.

Stocks fall across the globe as COVID-19 cases climb, Oil prices drop as Russia refuses supply cuts

Please check out our full Market Update Week 10 Market Update UK equities were down nearly 9% this morning, with the natural resource and banking heavy indices experiencing weakness for three prime reasons. First, coronavirus fears continued to rise as Italy quarantined 16 million residents, with investors fearful of this impact on the global economy […]

Monthly Market Update – October 2018

Read our full Monthly Market Update October 2018 September data continued to indicate global economic and risk asset divergence, consistent with a mature economic cycle, with USD assets rising as a result of Mr. Trump’s policies. The global economy is also diverging, with the US on a faster expansion path, while Europe and EM are […]

Monthly Market Update: EM’s Dollar Turmoil

Read our full Blueprint Sept 2018 August data continued to indicate global economic and risk asset divergence, consistent with a mature economic cycle, with USD assets rising as a result of Mr. Trump’s policies. The global economy is also diverging, with the US on a faster expansion path, while Europe and EM are slowing down. […]

Monthly Market Update, June: Volatile Europe

Read our full Monthly Market Update June 2018 May, a month of European volatility Global stocks were mixed last month. A combination of slower global growth, negative trade news and political volatility in Italy and Spain weighed with investors, many of whom chose to reduce their risk levels from more volatile regions. Performance was greatly affected […]

Weekly Market Update: Markets unfazed by US withdrawal from Iran Deal

Read our full Market Update Week 18 Market Update Last week saw equity markets across the board in positive territory in both local and GBP terms. Emerging markets lead the way with a +2.5% gain (+2.4% in local), followed by both US (+2.5% in Dollars) and UK large caps at +2.4% in Sterling. Japanese and […]

Gender pay and the changing face of the workforce

The gender pay gap is a hot topic in offices across the country as the April deadline for companies to report their pay gap has recently passed. The gender pay gap helps to highlight major demographic changes, in terms of the age and gender, affecting the UK’s labour force. The gender pay gap In an […]

Are higher interest rates a necessary evil?

“An economist is an expert who will know tomorrow why the things he predicted yesterday didn’t happen today.” Laurence J. Peter When I was studying economics at university (not that long ago) I was taught under ‘neo-classical’ thinking, which had come to pre-eminence in response to the period of ‘stagflation’ in the 1970s. Under stagflation […]

Black Swans are not so Black (or rare)

A “Black Swan” is a very popular notion in modern stock market commentary, yet the phrase originates from a time before the public listing of stocks. In 16th century London, people used an old Latin quote : “a rare bird in the lands and very much like a black swan“, based on the presumption that […]

Market Comment- Storm in a (bond) Teacup

Last week saw a 3.5% pullback for global equity markets, the first since 2016. One reason is a deterioration in global economic data. The second factor is the Federal Reserve, who’s stronger language on inflation and growth, driven by the corporate tax cuts, has made investors realise that its consensus opinion of 2 rate hikes […]

Markets sell-off at fastest pace since 2011

By David Baker, Chief Investment Officer After a strong start of the year for equity markets, global stocks shed almost 5% of their value on Friday and Monday. US equities are now 6.2% below their highs, turning negative for the year, as are global equities (-6.5% from their highs). The S&P 500 is now trading […]

Weekly Market Update: Stocks decline on COVID-19 fears, Bonds and Gold rally

Read our full Market Update Week 8 Market Update Fears that COVID-19 could weigh on consumption and global growth increased last week as the number of cases spiked in both Iran and Italy. Concerns that the virus could impact critical global supply chains have increased, with tech titan Apple widening their earnings estimates given the […]

Monthly Market Blueprint April 2020

The month in review: March Market Meltdown Q1 2020 saw the worst quarter for risk assets since the Global Financial Crisis as the dual shock of the COVID-19 pandemic and the Saudi Arabia-Russia oil price war wiped out equity markets and pushed credit spreads higher. Capital fled to the sovereign bond market with Treasury yields […]

The Great Lockdown – In Perspective

what goals cannot be achieved within the former, might be achieved by investing in stocks and bonds, whose growth is concomitant with the survival of capitalism.

Weekly Market Update: Lockdowns and US Election Raise Market Volatility

Market Update Global equities suffered their worst week since March, with the sell-off attributed to renewed virus related lockdowns across most of Europe and the final stretch of the hotly contested US presidential campaign. Global and US equities were both down -5.0%. This was despite the fact that Tech giants Alphabet, Amazon, Apple and Facebook […]

Weekly Market Update: China’s ‘LTCM moment’ may be the least of its problems, and ours.

Global stocks were relatively unchanged in Sterling terms (down -0.7% in USD terms) last week amid investors’ skepticism around supply chain issues hampering growth, elevated valuations and future monetary policy. Japanese stocks posted gains for a consecutive week, rising by +1.1%, as campaigning began for the next president of Japan’s ruling LDP. UK stocks fell by -0.9% amid higher than expected inflation, while US stocks were up +0.2% driven by a strengthened US Dollar. Globally, all sectors exhibited losses apart from energy stocks which posted solid gains of +2.8%. The US 10Y Treasury yield was up 2.1bps finishing the week at 1.363%, while the UK 10Y yield was up 8.9bps reaching 0.848%. Sterling fell against the US Dollar by -0.7% and remained flat against the Euro. In US Dollar terms gold lost -1.2%, while oil was up by +4.0%.

Weekly Market Update: Consumer-Led Recovery at Close to Fastest Pace in Modern History

Once again many major equity markets finished the week not far from where they started. Market attention was squarely focused on the Federal Reserve, where chairman Jerome Powell promised not to raise rates in the near term; as a consequence, markets did not sharply react in either direction. US equities were flat in US Dollar terms, but up +0.2% in Sterling terms. UK equities were the best performing region, up +0.5% last week. European equities fell for the second consecutive week, down -0.8% in Sterling terms. Emerging markets fell -0.2% in Sterling terms. Japan was the clear laggard, where earnings failed to meet expectations and the Bank of Japan kept policy unchanged. Japanese equities fell -1.9% in Sterling terms. The US 10Y yield rose on improved economic data, up 6.8bps to 1.6%, while the UK 10Y rose 9.8bps to 0.8%. Gold fell -0.3% on the week. The better than expected economic data helped oil to rise +2.4% last week to $64.4.

Weekly Market Update: Indian Covid Crisis Captures Attention of Markets

Equity markets ended the week largely unchanged, with the largest movements seen in Japanese and UK stocks. UK equities fell -1.1%, driven in part by a falling oil price, as the global economic outlook increasingly uncertain, with clear inequality in the vaccination progress between regions, dampening expected demand for oil. US equities fell -0.3% in Sterling terms, with plans to raise capital gains tax only making a slight impact on US markets. European equities rose +0.2% in Sterling terms due to currency effects, having fallen -0.4% in local currency terms. Emerging markets were the only risers in local currency terms, and were up +0.1% in Sterling terms. Globally the best performing sector was healthcare, whilst energy was the worst performing. The US 10Y yield fell slightly by 2.2 bps to 1.6%, while the UK 10Y fell 2 bps to 0.7%. Gold fell -0.2% on the week. Oil fell as the economic outlook deteriorated, down -1.7% on the week to $62.1.

Quarterly Outlook: Inflation: What is it good for?

Inflation expectations rising scared lethargic bond markets and became the most contentious subject of debate in the first three months of the year. Read our outlook to find our position on inflation and the impact on risk assets

What is the difference between a Mazars CIO and a boiling frog?

As an analyst I hate metaphors. While they are a very useful tool to turn my thorough -but often thoroughly boring- analyses into actual readable pieces, they also almost always convey a false sense of proportion. One of the most successful, yet dangerously misleading narratives I’ve read lately is one that equates investors to slowly […]

Weekly Market Update: Brexit Tempers Vaccine Regulatory Headwinds

Market Update Like clockwork positive vaccine news, this time FDA confirmation of Pfizer/BioNTech results, buoyed markets in the early part of last week. However some of these gains were reversed due to the worsening condition of both Brexit and Covid-19 cases. UK equities were flat for the week, however more domestically exposed mid-caps fell as […]

Weekly Market Update: UK Equities on Track for Second-Best Month on Vaccine Rally

Market Update Once again vaccine optimism supported global equity markets; this time it was the turn of the AstraZeneca vaccine, which can be more readily stored and transported. Global equities rose +2.1% for the week in Sterling terms. Financials and Energy were the two best performing sectors, as both sectors would benefit greatly from a […]

Monthly Market Blueprint: If you are looking at the election, you might be looking in the wrong place.

Dear reader,This note was written mid-day on 3 November, just a few hours before the US presidential election result. Naturally, we were tempted to delay, to get a clearer view of the earth-shattering events surrounding the world’s biggest economy and longest standing democracy. However, we decided to consider that the US presidential election could be […]

Weekly Market Update: Increasing Likelihood of US Government Trifecta Lifts Equity Markets

Read our Full Weekly Market Update Market Update A reduction in uncertainty in the United States helped US equities to their best week in three months, up +3.2% in Sterling terms, as investors begin to price in a Biden presidential victory. UK stocks looked past weaker than anticipated GDP growth to rally +2.0%. Investors appeared […]

Monthly Market Update: Policy Challenges

Seen from a bird’s eye view, the Fed has turned more hawkish in preparation to taper asset purchases. As a result, markets are now more prone to respond with volatility to rising risks, of which there’s no shortage: From soaring natural gas prices to impaired supply chains threatening consumers and businesses; from a new status […]

Weekly Market Update: Increasing COVID-19 case count caps equity market rally

Read our full Market Update Market Update Global equities traded higher last week, up +0.5% in Sterling terms. US equities climbed +0.9% with housebuilders, buoyed by promising housing data, leading the way. Other developed markets did not fare as well. UK and European stocks were down -1.3% and -1.1% respectively, driven by both the negative […]

Weekly Market Update: Equity Markets Rebound, Gold continues to soar

Read our Full Market Update Market Update Bucking the trend of two consecutive weeks of falling equity markets, all major indices were positive last week. Global equities gained +2.7% in Sterling terms, with the Nasdaq Composite reaching new highs, and the S&P 500 now close to its February peak. After a poor week last week, […]

Weekly Market Update: Stock markets post mixed returns on virus fears

Please read our full Market Update Market Update Stocks posted mixed returns last week, with strong performance in the US as the NASDAQ 100 set new record highs, while UK and Japanese stocks closed down -0.9% and -1.8% in Sterling terms respectively. Emerging Market stocks performed well, gaining +2.4% for the week. Technology, Telecoms and […]

Quarterly Investment Outlook Q3 2020: Covid Recovery and Anxiety

A quarterly report is not normally a difficult document to put together. Usually it consists of an account of the trending state of affairs, the more possible outcomes and risks to those outcomes. In the past few years, these reports were actually made easier. The US Federal Reserve was underwriting risk at such an unprecedented scale, nearly unwavering for more than a decade, in a manner which suppressed all major hazards to the economy and financial markets. Ever since 2010 the question, repeatedly, had been: “With opportunity costs driven down so much for so long, whatever can bring markets down?”

Three Burning Questions for Investors

In the past few weeks, we have been experiencing a flurry of better-than-expected economic data, especially in the US, while global equities remained near the recent high levels they have been trading at for almost a month. A casual read of the situation could be that the markets had run ahead of themselves, and as […]

Weekly Market Update: Stocks climb on promising economic data

Read our full Market Update Market Update Stock markets rebounded last week, posting gains in both local currency and Sterling terms, with news that the Fed will be expanding its corporate bond buying programme sending stocks higher. The move from ETF purchases to individual bond issues by the Fed has been viewed as a significant […]

WEEKLY MARKET UPDATE: Markets fall on second wave fears, gloomy Fed

Read our full Market Update Market Update The rally in risk assets came to a grinding halt last week on fears of a second wave of infections in the US, with virus rates up in many states, and the Federal Reserve offering up a gloomy economic outlook. Stocks are also down this morning on news […]

Monthly Market Blueprint June 2020

The “right” fundamentals Often the first thing we are taught about something, especially if it comes from someone with authority, like a parent, a teacher or our experienced financial adviser, is taken as a “fundamental” truth. In psychology, this is called the “primacy effect”. Any other “truths” that contradict or seek to modify that first […]

Equity Storm in a (Bond) Teacup

Last week marked a 3.5% pullback for global equity markets, the first since 2016. The move comes after a very good month, January, during which equities rose to fresh highs, gaining 5.2%, prompted by exuberance related to the US tax reform. However, the arrival of February marked fresh concerns for investors. First and foremost, economists […]

Great post. It is interesting to read what others

thought and how it relates to them or their clients, as their view could

possibly assist you in the future.

Best regards,

Thomassen Hessellund