The UK's energy market and its broader implications

Thought Leadership

The UK’s energy market and its broader implications

Thu 23 Sep 2021

Much of the recent news in the UK has been devoted to the spike in household energy costs and the potential collapse of the number of providers in that market from around 50 to 10 by the end of winter. In fact, since writing this first draft of this piece 2 providers have gone bust, leaving more than 800,000 customers without a provider. Of itself this is an interesting topic: it seems remarkable that rising wholesale gas prices can rupture the UK energy market and reduce the number of energy providers by 80%. For us the more relevant question relates to the wider economy and how energy costs can impact consumer demand and inflation, which contributes to our discussions when deciding asset allocation. This blog post aims to explore the former and explain the Mazars Investment Team thinking on the latter.

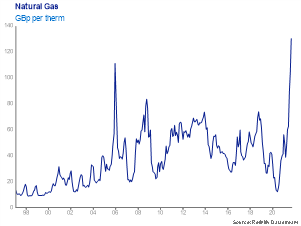

The factors leading to this situation are aptly described as a perfect storm, the first part of which relates to the rising cost of wholesale gas: Europe’s gas stocks were depleted after a long winter last year, Russia has been supplying the market with less gas, Asia has been taking up more of the gas available and supply from the North Sea is diminished while maintenance is performed that had been delayed due to the pandemic. These factors are not specific to the UK but led to an increase in gas prices which has affected all European countries.

In the UK rising gas prices have been felt particularly hard. The UK is more reliant on the spot market for gas supply than other gas-importing nations because it has significantly less gas storage capacity. Also, the UK’s renewable sources of energy have recently delivered less than would be expected normally due to lower levels of wind and nuclear energy production suffering outages. As a result, UK suppliers have bought more gas at the market rate than they have historically and more than other gas-importing countries have had to.

Regulatory interference over the last decade has also led the UK’s energy market to where it is now. The desire to reduce the hold of the so-called “Big 6” providers led to one of the world’s most fragmented markets which at one point consisted of as many as 70 energy providers. Within this crowded market firms competed aggressively on price and have not been able to achieve scale and the financial strength that accompanies scale. Therefore, not all gas supply was hedged because some companies simply could not afford the margin requirements to do so. A situation arose where customers who had previously purchased fixed rate energy contracts were being supplied with gas that was purchased at the market rate and some suppliers are incurring a loss equal to the difference between the lower price secured by customers and the current rising price of gas.

The final point is also regulatory in nature. The UK’s price cap that was introduced in 2019 to limit the profits made by energy providers is only reviewed twice per year, in October and April. As wholesale gas prices have risen in 2021 energy providers are still constrained by the price cap set last April which has squeezed the profits of an under-capitalised market.

This combination of factors is causing losses for energy providers and even triggering some to go out of business. The situation is causing much consternation among consumers as the UK government is being urged to step in to support the businesses in the sector and to protect consumer interests. For investors however the issue is larger and concerns the wider UK economy.

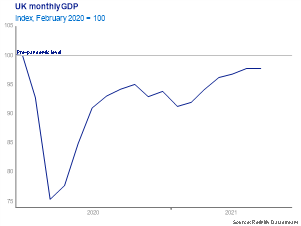

The first place that energy prices can impact the wider economy is consumer demand, particularly among low-income households. Larger energy bills reduce disposable income so money that could have gone into the economy is given up to higher commodity costs which is of no economic benefit. GDP data shows that the UK’s economy remained flat in July at 2% below its pre-pandemic level and August retail sales came in 0.9% lower than July, below the growth of +0.9% that was expected. For now, the impact on consumer spending across the economy is small but if gas prices were to continue to rise then this is something we will take into consideration.

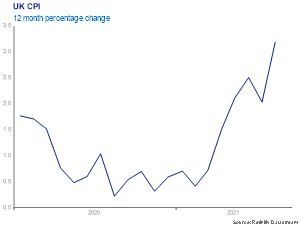

The second issue is the effect of energy prices on inflation and the decisions of the Bank of England’s Monetary Policy Committee (MPC). Price changes in the UK as measured by CPI were 3.2% higher in August than 12 months earlier. When the energy regulator, Ofgem, raises the price cap on energy bills by 12% in October that is expected to add approximately 0.7% to CPI and were there to be a similar lifting of the price cap in April that would have a similar effect on CPI, pushing CPI well above 4%, all else being equal. However, 12 months after the rises their effect will drop out of the CPI reading meaning that unless energy costs go on to rise year after year CPI will fall back again. For now the MPC is likely to look beyond such temporary factors when it decides on the next move for monetary policy and will be inclined to leave interest rates unchanged but if we see sustained wage increases to match the cost of living then it will be forced to choose between choking off economic growth or allowing inflation to run well above the 2% level mandated for the Bank of England.

The drag of rising prices, including rising energy prices, and potential interest rate rises by the MPC on economic growth mean that investors need to consider whether the 7% economic growth forecast by the IMF for the UK in 2021 is achievable or overoptimistic. We are aware that domestically focused UK mid-cap companies have rallied 15% in 2021 and 40% over 12 months reflecting the economic rebound. An important question is whether there is too much optimism in the post-pandemic recovery given that the elevated pace of growth post pandemic must moderate at some point and should we therefore reduce our allocation to the UK. For now, we are satisfied with our overweight position in UK equities, happy that valuations are below developed market peers and that UK companies provide exposure to the cyclical rebound in the global economy post-pandemic.

Related posts

Weekly Market Update: Port congestion isn’t dealt with interest rate hikes

Equities in most major markets edged higher last week, partly offsetting the previous week’s losses, with global stocks up +0.3% in GBP terms. US stocks were up +0.4% despite the disappointing jobs report published on Friday. European stocks were up +0.2% amid high volatility while UK stocks were up +1.0% despite the BoE’s new Chief Economist raising the alarms on inflation’s persistence in the coming months. Globally, energy stocks outperformed all sectors for a fifth week in a row, posting solid gains of +4.9%, followed by financials, utilities and materials. The US 10Y Treasury yield was up 15.0bps, finishing the week at 1.612%, while the UK 10Y yield was up 15.6bps reaching 1.158%. Sterling rose by +0.5% against the US Dollar. In USD terms gold pulled back by -0.6%, while oil was up by +4.1%, reaching $81 per barrel.

Inflation momentum will recede. But prices may remain elevated.

There’s a strong possibility we may see the end of the episode soon. But supply chains could take long to mend and overall price levels could remain elevated versus pre-pandemic numbers.

Weekly Market Update: Bonds Sell Off Spills Over to Wider Market

A significant rise in US Treasury yields unsettled markets last week. US equities fell -1.9% in Sterling terms, with Tech stocks suffering their worst week in nearly six months. UK equities fell -1.9%, with Energy and Financials the only two positive sectors for the week. Emerging Markets suffered the greatest sell-off, having led global equity markets so far this year. UK and Emerging Markets are the only major equity markets still positive for the year in Sterling terms. Globally the only positive sector was Energy which was supported by rising oil prices. Investors will keep a keen eye on the OPEC+ meeting this week for any indication of increased oil supply. Japanese equities fell -2.4% in Sterling terms, the worst performing region year-to-date for UK investors. The US 10Y yield continued its rise, up 6.9 bps to 1.4%, at one point hitting 1.6%, and the UK 10Y rose 12.2 bps to 0.8%. Long-term yields are now trading at their highest level since the pandemic. Gold fell -2.3% on the week, while Oil rose +4.4% to $62.7.

Macroeconomic View – German exports accelerating

German exports were weak for the month, up only 0.3%, but are still accelerating year-on-year. Chinese exports were stable, but imports picked up significantly, offsetting last month’s weak data. UK The Markit Services PMI dropped slightly to 53 from 54.2. The Halifax House Price Index year-on-year for the 3 months to January fell from 2.7% […]

Macroeconomic View – French unemployment down

French ILO unemployment dropped unexpectedly from 9.6% to 8.9%. It was further proof of the strength in the French, and subsequently, the European economy. European equities lost 1.5% briefly after the US inflation report was released, with figures higher than expected. The market recovered, but the move is indicative of the factors that affect traders. […]

Macro of the Week – UK GDP slowing

The UK economy grew more slowly than previously estimated in Q4 2017, increasing by 0.4% quarter-on-quarter according to the second estimate by the ONS. This figure was a 0.1% downgrade from the original estimate. The downward revision was due to slower […]

Macro of the Week – Fed hikes rates, more expected

As widely expected the FOMC raised the Fed Funds Rate target by 0.25% to a range of 1.5% – 1.75%, in what was a unanimous decision by the committee. It was the sixth rate hike since the GFC as the central bank looks to ‘normalise’ interest rate policy and was the first major decision under […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

Weekly Market Update: Flexible Federal Reserve Sends Cable and Yields Higher

Read our full Market Update Market Update US equities climbed +1.4% last week with, major indices setting new record highs, as US Federal Reserve Chairman Jerome Powell announced a shift in how the Fed views inflation, saying it won’t increase interest rates to respond to low unemployment levels and also won’t worry as much about […]

Weekly Market Update: Markets Rally for Second Week as Inflation Expectations Return

Global equities continued last week’s gains, rising +0.7% in Sterling terms. UK equities, amongst the top performing major markets, rose by +1.6%. They were supported by rising oil prices and positive returns from energy companies, as the domestic market is overweight to the Energy sector. European equities, amid high volatility, were up +0.8%, due to improved coronavirus infection rates and hopes of a large U.S. economic stimulus. US equities rose +0.4%, the worst performing major region. Globally, Energy was the best performing sector whilst Utilities and Cons. Discretionary were the only sectors to finish the week down. Emerging Markets maintained their strong performance since the start of the year, posting gains of +1.5%. Sterling rose +0.8% and +0.3% against the US Dollar and Euro respectively, continuing its strengthening trend this year. The US 10Y yield rose 4.5bps to 1.2% and the UK 10Y rose 3.5bps to 0.52%. Gold fell -2.0% on the week, while Oil rose +3.7%.

Weekly Market Update: The Yield, Not “Inflation” Will Determine the Rotation

Equity market gains early last week were, broadly speaking, eroded as bond yields continued to rise, reaching one-year highs. Amid falling oil prices and rising political uncertainty caused by potential bans on vaccine exports coming out of the EU, many major equity markets fell last week. US equities fell -0.5% from record highs in Sterling terms, despite the country surpassing 100 million vaccinations on Friday. UK equities fell -0.7%, now down -2.4% from their 52-week highs in January. Globally the best performing sector was healthcare, whilst energy, due to oil prices, was the worst performing. Japanese equities rose +3.6% and are the best performing major equity markets this year. The US 10Y yield continued its rise up 9.6bps to 1.7%, while the UK 10Y rose 1.6bps to 0.8%. Gold rose +1.3% on the week. Oil has seen back-to-back weekly declines, down -6.1% to $61.2 a barrel, due to a glut of supply and weakening demand forecasts.

Weekly Market Update: Investors dilemma: Cheaper bonds or returning dividends?

Markets returned to positive territory this week, supported in part by progress on the Biden stimulus bill. However, chair of the Federal Reserve Jerome Powell’s speech, with a lack of updates to current policy, disappointed investors leading to a sell-off on Thursday afternoon. US equities rose +1.7% in Sterling terms. UK equities rose +2.5%, with UK equity markets benefiting from rising oil prices. Emerging Markets grew +0.9% in Sterling terms, although this was a more moderate +0.1% in local currency terms. Globally the best performing sector was Energy, whilst IT was the worst performing, as the rising yield environment impacted valuations. Japanese equities rose +1.0%. The US 10Y yield continued its rise, up 16.1 bps to 1.6%, while the UK 10Y fell 6.4bps to 0.8%. Gold fell -1.1% on the week. Oil rose sharply, up +8.4% on the week to $66.5 following the OPEC meeting where it was decided to hold production at current levels, when a rise in production had been anticipated.

Investing in a world without QE

Inflation rising may upend a 12-year investment paradigm. Is there life after Quantitative Easing?

Will the rotation into value continue?

While it remains to be seen how long value leadership will last, many of the drivers that led investors to flock to growth stocks have reversed and now favour value stocks.

Weekly Market Update: US Inflation Unnerves Equity Markets

Global economies are reopening, and moving into the recovery phase, this pickup in activity has lead investors to question the potential impact on inflation. Investors are cautious of whether inflationary effects will be transitory or long-lasting. The US inflation reading unnerved markets and all major equity markets fell last week. US equities fell -2.2% in Sterling terms, partly driven by currency effects, markets had sold off sharply at the start of the week before recovering in the latter half. UK equities, which typically move inversely to Sterling, due to high levels of overseas earnings, fell -1.2%. Japanese equities fared worst last week, caught in global equity volatility and increased lockdowns, falling -4.0% last week. Despite strong Chinese equity performance, emerging market equities fell -3.8% in Sterling terms. The US 10Y yield rose 5.1bps to 1.6%, while the UK 10Y rose 8.2bps to 0.9%. Both gold and oil were nearly unchanged, falling -0.2% and -0.1% on the week respectively.

Is gold a good hedge against inflation?

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise.

Quarterly Outlook: An investor’s inflation and growth playbook

Investing during the past twelve years has been underpinned by a basic principle: market participants have been encouraged to take risks, mainly to offset the trust shock that came with the 2008 financial crisis (GFC). Each time equity prices have fallen significantly, the Federal Reserve, the world’s de facto central bank, would suggest an increase in money printing, or actually go ahead with it if volatility persisted. Bond prices, meanwhile, kept going up, as central banks and pension funds were all too happy to relieve private investors of their bond holdings even at negative yields. Market risk was all but underwritten.

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

Weekly Market Update: Operations Managers are the new economists

Equities in most major markets posted minor gains last week with global stocks up +0.3% in Sterling terms, as inflation concerns seem to have stemmed a previously strong investor sentiment. US stocks were up +0.2% as multi-year high inflation data offset positive news on employment data. EU stocks were up +0.2%, despite Covid-19 cases surging in most countries in the region. UK stocks were up +0.7% while EM equities rose by +2.2%, driven by China’s announcement that it would propose easing measures to aid indebted real estate firms. The US 10Y Treasury yield was up 11.0bps finishing the week at 1.561%, while the UK 10Y yield was up 6.9bps reaching 0.914%. In US Dollar terms gold posted solid gains for the second week in a row, up +3.1%, while oil was down -0.1% to $80.4 per barrel.

Weekly Market Update: Inflationary pressures may be moderating. Supply chain pressures aren’t.

Equities in most major markets posted losses last week with global stocks down -0.4% in Sterling terms, as inflation concerns, supply chain issues and rising coronavirus cases dampened investor sentiment. US stocks were up +0.1% with growth stocks exhibiting solid gains, outweighing the losses in more cyclical firms. European stocks were down -1.8%, as countries within the region started imposing restrictions to curb rising Covid-19 cases. UK stocks were down -1.6% amid CPI inflation figures hitting a ten-year high, while EM equities fell by -1.7%. The US 10Y Treasury yield was down 2.2bps finishing the week at 1.548%, while the UK 10Y yield was down 3.5bps reaching 0.880%. In US Dollar terms gold lost some of its previous weeks’ gains, down -1.3%, while oil was heavily down -6.2% to $76 per barrel.

Macro of the Week – US wages accelerate

US hiring picked up in January and wages rose at the fastest pace since the GFC. Hourly earnings increased 0.3%, resulting in an unexpected year-on-year increase of 2.9%, up from 2.7% in December (which was also revised up from 2.5%). This was on the back of a nonfarm payrolls increase of 200k, which was upwardly […]

Comments