IAS accounting requirements for Pillar 2: GloBE for periods ending 31 December 2023

Tax compliance

IAS accounting requirements for Pillar 2: GloBE for periods ending 31 December 2023

Thu 11 Jan 2024

Background to Pillar 2 (GloBE)

Part of the ongoing work of the OECD to combat tax avoidance and targeted at low tax jurisdictions, the Pillar 2 – GloBE rules will apply to large organisations (>€750m of global revenue) with each country having its own rules implementing some form of 15% minimum tax, or otherwise risking that an equivalent amount will be charged by other group entities in respect of that country’s profit.

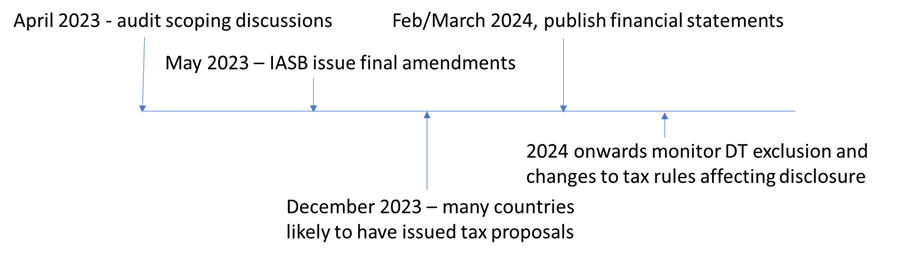

Each country will have a different version of legislation all based on a Model text. Implementation dates start from as early as accounting periods beginning 1 January 2024 and although the first reporting for Pillar 2 – GloBE is not until 30 June 2026, there are accounting disclosures that will be required in IAS reporting accounts for periods ending 31 December 2023 for many jurisdictions.

IASB consultation on IAS 12

The IASB has now completed a consultation on proposals for disclosure of the effects of Pillar 2 – GloBE and has agreed to finalise amendments to IAS 12 by the end of May 2023.

As countries look to finalise changes to their tax rules in response to Pillar 2 – GloBE, it is worth considering what the IASB proposals would mean given the different ways in which local country rules may change.

IASB proposals in a nutshell

- Calculate an IAS 12 effective tax rate (“IAS 12 ETR”) by country and disclose this.

- Comment, to the extent possible on where this ETR may differ from the Pillar 2 – GloBE ETR

- If the country has an IAS 12 ETR of less than 15% but no top-up tax is expected

- If the country has an IAS 12 ETR of greater than 15% but top-up tax is expected

- Provide a “temporary” exclusion from reporting deferred tax on tax changes designed to implement Pillar 2.

Groups will need new procedures and controls to manage the new reporting requirements.

An example of IASB proposals

It looks likely that it will be necessary to disclose the IAS 12 effective tax rate, including movements in deferred tax except any movements relating to Pillar 2 implementation rules.

This is the key area of uncertainty remaining. The notes on tax law to which the exclusion requires (Note 2 to the consultation on p.15 states):

“This Basis for Conclusions refers to tax law enacted or substantively enacted to implement the Pillar Two model rules, including tax law that implements qualified domestic minimum top-up taxes, and the income taxes arising from it, as ‘Pillar Two legislation’ and ‘Pillar Two income taxes’.

In the example below, we have assumed Singapore make changes which do not meet the definition, and so deferred tax is required, and Bermuda substantively enact changes which do meet the requirements and so no deferred tax is required.

| US | UK | Germany | Singapore | Bermuda | |

| Profit | 1 000 | 500 | 300 | 400 | 600 |

| Current tax | (280) | (125) | (90) | (20) | 0 |

| Deferred tax | 50 | 60 | (40) | (50) | 0 |

| Tax | (230) | (65) | (130) | (70) | 0 |

| IAS 12 effective tax rate | 23% | 13% | 43% | 18% | 0% |

Notes

- US proposed 28% tax rate and a small utilisation of deferred tax liability

- UK current tax rate of 25% with utilisation of deferred tax liability

- German current tax rate of 30% and setup of a deferred tax liability

- Singapore incentive rate of 5% for 2023 and 2024 and setup of deferred tax liability assuming a 2025 rate enacted of 15%, assuming not a Pillar 2 tax and so deferred tax is set up at the new rate

- Bermuda current rate of 0% and setup of deferred tax liability assuming 2024 rate enacted of 15% but as a Pillar 2 tax and therefore deferred tax is not required to be set up

Additional disclosure

It is not clear yet how much work would need to have been done on assessment of the Pillar 2 – GloBE ETR for these jurisdictions before it is necessary to comment on which:

- IAS 12 ETR below 15% will probably not have top-up tax in 2024 – in our example, the UK

- IAS 12 ETR above 15% will probably have top-up tax in 2024 – in our example, Singapore.

Given that some of the analysis will depend upon whether deferred tax is required, or if the exclusion applies, we anticipate there will be further guidance from IASB on what exactly constitutes a tax that needs to be ignored for deferred tax purposes vs a rate change which needs to be reflected. Groups impacted would need to make sure they are comfortable with their application of this guidance.

We expect many groups to be reviewing their Country by Country Reporting tax returns in 2023 to determine readiness for Pillar 2 – GloBE with this work feeding into the disclosures required.

Want to get notified when new blog posts are published?

Subscribe

Neil Rolfe Partner - Head of Insurance Tax - UK

Donay Viljoen Manager - Financial Services Tax - Bermuda

The benefits of having a tax control framework

Tax control frameworks are becoming increasingly common as companies seek to manage their taxation, compliance, and risk management obligations more effectively and efficiently. So, what is a tax control framework, and what are the benefits? A tax control framework is a set of processes and internal control procedures that ensure a company’s tax risks are […]

UK Spring Budget 2024

The UK Spring Budget on 6 March 2024 was relatively measured in its tax policy decisions, despite a background of falling inflation and rising tax receipts. Below are some areas of interest for globally mobile individuals, those with UK staff, and those with business and investment interests. Main measures affecting individuals Main measures affecting those […]

The right tax approach: why companies need a tax control framework

Across the globe, an increasing number of companies are developing tax control frameworks to help them stay on top of their taxation, compliance and risk management obligations and objectives. These obligations are continually evolving, driven by a combination of both...

Ecological taxes: new updates in Mexico

Several Mexican states had imposed ecological taxes in order to encourage certain industries to reduce their polluting emissions. In addition, green taxes have recently been imposed as a consequence of the warning issued by the Mexico Climate Initiative (MCI) that Mexico’s carbon dioxide emissions could increase by up to 59.8% by 2050 if the country’s green […]

A basic guide to understanding Pillar 2 GloBE minimum top-up tax rules

As in-scope organisations* embark on a new Pillar 2 Global Anti-Base Erosion (GloBE) journey, having a clearer understanding of how jurisdictions will enact the global minimum 15% tax rule is vital. Notably, while Pillar 2 GloBE sets out model rules on what jurisdictions need to achieve, there is an element of flexibility in how each […]

Green investments in Austria: new tax allowance introduced effective 2023

When the Austrian government – a coalition between the conservative People’s Party and the Green Party – presented their government program for 2020-2024, an “eco-social tax reform” was one of the key elements. The most recent measure has been the introduction of an investment allowance that especially incentivises “green investments”. The two main pillars of […]

How CARF, MiCA, and DAC8 will impact tax transparency in relation to the WEB 3 and other recent web developments

The development of new web communication systems such as WEB3 is making it very difficult for tax authorities to trace taxable transactions. However, measures proposed by the OECD and the European Union aim to provide a framework that will permit traceability of tax transactions. The technical characteristics of a crypto asset make it difficult for […]

ATAD3 update: significant amendments recommended by the European Parliament

The European Parliament proposes significant amendments to the Anti-Tax Avoidance Directive, commonly known as ATAD3. ATAD3 seeks to prevent the misuse of shell companies for tax purposes. Compared to the initial draft Directive, the proposed amendments may provide relief for international organisations. In essence, ATAD3 imposes increased reporting obligations and denial of tax benefits under […]

Mexico approves the Multilateral Instrument (MLI) to implement Tax Treaty Measures

On 12 October 2022, the Mexican Government approved the Multilateral Instrument (MLI) related to the application rules for double taxation agreements (DTAs) to prevent Base Erosion and Profit Shifting (BEPS). The rules were published in the Official Gazette of the Federation on 22 November 2022. Included in the Mexican Government’s reservations and notifications are […]

EU’s new SAFE initiative to bolster existing tax evasion measures

The European Commission (EC) launched an initiative on 6 July 2022 concerning the fight against tax evasion and aggressive tax planning. As a result, a public consultation introducing the Securing the Activity Framework of Enablers (SAFE) directive has now been held. The proposed measures could increase compliance costs for all those involved in providing tax […]

Proposed changes to the offshore regime for passive income in Hong Kong

Background To address harmful tax competition, the European Union (“EU”) requires Member States to refrain from introducing any new harmful tax measures and amend any laws or practices deemed to be harmful. Regarding non-EU jurisdictions, the EU has also evaluated their tax regimes against international tax standards and put in place a list of noncooperative […]

The Google tax: The UK story, 7 years later

The Diverted Profits Tax (DPT), or what the media have dubbed the Google tax, was introduced in 2015 to dissuade and counteract contrived arrangements used by large multinational groups that divert profits from the UK and erode the UK tax base.

The impact of digital assets and cryptocurrencies decentralised finance on taxation in various jurisdictions

Digital assets and cryptocurrencies continue to evolve by offering new services and products such as Decentralized Finance (DeFi) and non-fungible tokens (“NFTs”), but is tax legislation also keeping up to date with the ever-changing world of digital assets and cryptocurrencies?

Are you ready for the GloBE tax challenges?

On 14 March 2022, the OECD published a comprehensive commentary and illustrative examples of how implementing the Global Anti-Base Erosion Model Rules (GloBE rules) could look. In this blog, we discuss the GloBE rules and examine how the rules apply and filing requirements. On 20 December 2021, the OECD published model rules that member countries […]

Environmental tax pillar in the environmental, social, and governance system

The information regarding environmental taxes paid by an organisation, as well as the actions taken to mitigate the impact on the environment could be included in environmental, social, and governance (ESG) reporting. Environmental reporting in total is an important element for parties to consider when doing business. Along with environmental reporting, environmental taxes play a […]

Tax compliance and incentives during martial law in Ukraine

A crucial number of Ukrainian companies (including subsidiaries of international enterprises) experienced negative business and financial impacts as a result of the Russian invasion of Ukraine which started on 24 February 2022. The urgent relocation of staff to other regions of Ukraine and abroad, interruption of access to internal databases, IT systems, and paper documents […]

The Anti-Tax Avoidance Directive II: Will other jurisdictions follow the UK’s lead?

ATAD II is the EU translation of BEPS Action 2, the part which is focused on the ability of taxpayers to design situations of double non-taxation or heavily reduced taxation by exploiting hybrid mismatches. They apply to mismatches between the EU Member States, the UK, Mexico, Australia, New Zealand, and third countries. This legislation has […]

Compliance bulletin helps businesses in Mexico

Mazars experts around the world deliver tailored services in audit, accounting, tax, financial advisory, consulting, and legal services. In Mexico, local experts have created a compliance dashboard with news items to help guide businesses as they navigate issues related to finance, tax, legal, and labour updates. With the global economy recovering from Covid-19, new government-required procedures […]

Brexit impact on in/outbound payments

When the UK finally left the EU ended on 31 December 2020, the application of provisions that have been beneficial to cross-border payments within the EU ceased, or will cease to apply. The elimination of withholding taxes, formerly part of these provisions, means companies with cross-border dividend, interest and royalty payment flows to or from […]