Equities in most major markets posted minor gains last week with global stocks up +0.3% in Sterling terms, as inflation concerns seem to have stemmed a previously strong investor sentiment. US stocks were up +0.2% as multi-year high inflation data offset positive news on employment data. EU stocks were up +0.2%, despite Covid-19 cases surging in most countries in the region. UK stocks were up +0.7% while EM equities rose by +2.2%, driven by China’s announcement that it would propose easing measures to aid indebted real estate firms. The US 10Y Treasury yield was up 11.0bps finishing the week at 1.561%, while the UK 10Y yield was up 6.9bps reaching 0.914%. In US Dollar terms gold posted solid gains for the second week in a row, up +3.1%, while oil was down -0.1% to $80.4 per barrel.

CIO Analysis

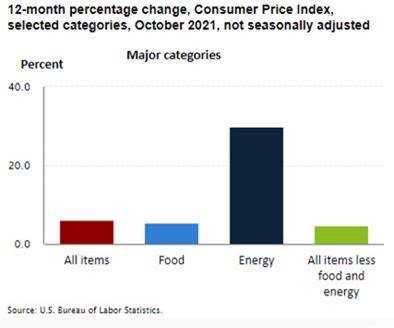

Inflation concerns dominate the discussion after last week’s surprise 6.2% yearly rise of goods in the United States. European numbers also picked up, with Germany, the manufacturing heartland of Europe and historically an inflation-phobe, registering the highest inflation numbers in more than two decades.

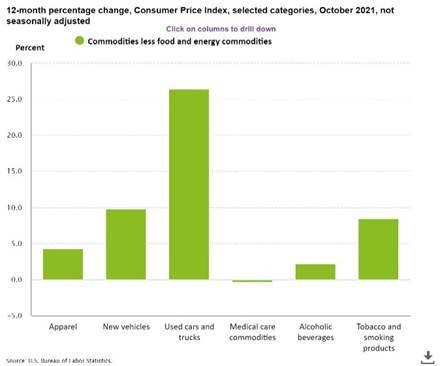

Numbers themselves are useless, of course, if they are not broken down. While year-on-year US inflation has hit 6.2%, since October 2019, prices in the US have risen 3.6% per annum. This of course is still close to twice the Fed’s target of 2%. Excluding food and energy, the bi-annual rate is closer to 3%. Around a tenth of the weight is due to sharp rises in the costs of new cars and trucks, which have risen more than 12% per annum. Deduct just this one category, plus energy and food, and average-two year inflation would be closer to a much more acceptable 1.9%-2%.

This 6.2% headline number is highly focused on energy and car prices. And while these are very real costs for consumers there is precious little central banks can do about them. With supply chains stretched to the point of breaking and possibly beyond, demand for manufacturing goods has been erratic and based on availability. Scarcity only drives up demand itself (“I may need one item X now, but if there are only a few available, I might as well order two to cover future needs”). Just-in-time inventories have given way to a good-old-fashioned stocking-restocking cycle and without the availability of warehouses, congested ports have taken their place, causing even more congestion. This has caused energy and transportation costs to soar. The supply chain problem is so sprawling that it would take a centralised global approach to address. Unfortunately, the Covid-19 crisis has only exacerbated geopolitical problems, placing a coordinated solution realistically beyond reach.

Adding to lockdown-related dysfunctions, China, the world’s top trading partner, is going through its own political and economic transition. Supply chains were already stretched and have become hyper-sensitive to even the smallest disruptions (see Suez Canal issues). China adding further pressure could well break the proverbial camel’s back.

The length of this inflationary bout will be very closely correlated to developments in China. What it will not be correlated to is the Fed’s interest rate cycle. The US central bank has signalled that it does not intend to fight this price spike. If it did, interest rates would already be above 5%. Whether transitional or not, the Fed doesn’t have the tools to deal with supply inflation in a globalised economy. Instead, it is tapering asset purchases to fight asset price inflation, which is taking place in the financial economy. Reports last week suggest that Joe Biden is thinking of replacing dove Jay Powell with uber-dove Lael Brainard.

As inflation grips economies, it has become apparent that to assess this particular incident, we must look beyond interest rates, money velocity and recent history. For markets to understand what will happen with the financial economy and risk assets, they still need to focus on central bankers. To understand what the future brings on inflation and growth, however, instead of economists, portfolio managers would be better served to turn their attention to operations management and Xi Jinping.

–David Baker, CIO

Related posts

Weekly Market Update: Investors dilemma: Cheaper bonds or returning dividends?

Markets returned to positive territory this week, supported in part by progress on the Biden stimulus bill. However, chair of the Federal Reserve Jerome Powell’s speech, with a lack of updates to current policy, disappointed investors leading to a sell-off on Thursday afternoon. US equities rose +1.7% in Sterling terms. UK equities rose +2.5%, with UK equity markets benefiting from rising oil prices. Emerging Markets grew +0.9% in Sterling terms, although this was a more moderate +0.1% in local currency terms. Globally the best performing sector was Energy, whilst IT was the worst performing, as the rising yield environment impacted valuations. Japanese equities rose +1.0%. The US 10Y yield continued its rise, up 16.1 bps to 1.6%, while the UK 10Y fell 6.4bps to 0.8%. Gold fell -1.1% on the week. Oil rose sharply, up +8.4% on the week to $66.5 following the OPEC meeting where it was decided to hold production at current levels, when a rise in production had been anticipated.

Weekly Market Update: Port congestion isn’t dealt with interest rate hikes

Equities in most major markets edged higher last week, partly offsetting the previous week’s losses, with global stocks up +0.3% in GBP terms. US stocks were up +0.4% despite the disappointing jobs report published on Friday. European stocks were up +0.2% amid high volatility while UK stocks were up +1.0% despite the BoE’s new Chief Economist raising the alarms on inflation’s persistence in the coming months. Globally, energy stocks outperformed all sectors for a fifth week in a row, posting solid gains of +4.9%, followed by financials, utilities and materials. The US 10Y Treasury yield was up 15.0bps, finishing the week at 1.612%, while the UK 10Y yield was up 15.6bps reaching 1.158%. Sterling rose by +0.5% against the US Dollar. In USD terms gold pulled back by -0.6%, while oil was up by +4.1%, reaching $81 per barrel.

Weekly Market Update: Bonds Sell Off Spills Over to Wider Market

A significant rise in US Treasury yields unsettled markets last week. US equities fell -1.9% in Sterling terms, with Tech stocks suffering their worst week in nearly six months. UK equities fell -1.9%, with Energy and Financials the only two positive sectors for the week. Emerging Markets suffered the greatest sell-off, having led global equity markets so far this year. UK and Emerging Markets are the only major equity markets still positive for the year in Sterling terms. Globally the only positive sector was Energy which was supported by rising oil prices. Investors will keep a keen eye on the OPEC+ meeting this week for any indication of increased oil supply. Japanese equities fell -2.4% in Sterling terms, the worst performing region year-to-date for UK investors. The US 10Y yield continued its rise, up 6.9 bps to 1.4%, at one point hitting 1.6%, and the UK 10Y rose 12.2 bps to 0.8%. Long-term yields are now trading at their highest level since the pandemic. Gold fell -2.3% on the week, while Oil rose +4.4% to $62.7.

Weekly Market Update: The Yield, Not “Inflation” Will Determine the Rotation

Equity market gains early last week were, broadly speaking, eroded as bond yields continued to rise, reaching one-year highs. Amid falling oil prices and rising political uncertainty caused by potential bans on vaccine exports coming out of the EU, many major equity markets fell last week. US equities fell -0.5% from record highs in Sterling terms, despite the country surpassing 100 million vaccinations on Friday. UK equities fell -0.7%, now down -2.4% from their 52-week highs in January. Globally the best performing sector was healthcare, whilst energy, due to oil prices, was the worst performing. Japanese equities rose +3.6% and are the best performing major equity markets this year. The US 10Y yield continued its rise up 9.6bps to 1.7%, while the UK 10Y rose 1.6bps to 0.8%. Gold rose +1.3% on the week. Oil has seen back-to-back weekly declines, down -6.1% to $61.2 a barrel, due to a glut of supply and weakening demand forecasts.

Weekly Market Update: Flexible Federal Reserve Sends Cable and Yields Higher

Read our full Market Update Market Update US equities climbed +1.4% last week with, major indices setting new record highs, as US Federal Reserve Chairman Jerome Powell announced a shift in how the Fed views inflation, saying it won’t increase interest rates to respond to low unemployment levels and also won’t worry as much about […]

Weekly Market Update: US Inflation Unnerves Equity Markets

Global economies are reopening, and moving into the recovery phase, this pickup in activity has lead investors to question the potential impact on inflation. Investors are cautious of whether inflationary effects will be transitory or long-lasting. The US inflation reading unnerved markets and all major equity markets fell last week. US equities fell -2.2% in Sterling terms, partly driven by currency effects, markets had sold off sharply at the start of the week before recovering in the latter half. UK equities, which typically move inversely to Sterling, due to high levels of overseas earnings, fell -1.2%. Japanese equities fared worst last week, caught in global equity volatility and increased lockdowns, falling -4.0% last week. Despite strong Chinese equity performance, emerging market equities fell -3.8% in Sterling terms. The US 10Y yield rose 5.1bps to 1.6%, while the UK 10Y rose 8.2bps to 0.9%. Both gold and oil were nearly unchanged, falling -0.2% and -0.1% on the week respectively.

Weekly Market Update: S&P 500 hits all-time high, Chinese economic growth slows to multi-decade lows

Read our full Market Update Week 28 Market Update Despite a mixed week for equities, the S&P 500 set new records on Friday, closing above 3,000 for the first time at 3,013.77. US equities gained +0.4% in Sterling terms, with all other major regions down. Emerging Market equities fell the most, down -1.2%, European equities […]

Weekly Market Update: Markets Rally for Second Week as Inflation Expectations Return

Global equities continued last week’s gains, rising +0.7% in Sterling terms. UK equities, amongst the top performing major markets, rose by +1.6%. They were supported by rising oil prices and positive returns from energy companies, as the domestic market is overweight to the Energy sector. European equities, amid high volatility, were up +0.8%, due to improved coronavirus infection rates and hopes of a large U.S. economic stimulus. US equities rose +0.4%, the worst performing major region. Globally, Energy was the best performing sector whilst Utilities and Cons. Discretionary were the only sectors to finish the week down. Emerging Markets maintained their strong performance since the start of the year, posting gains of +1.5%. Sterling rose +0.8% and +0.3% against the US Dollar and Euro respectively, continuing its strengthening trend this year. The US 10Y yield rose 4.5bps to 1.2% and the UK 10Y rose 3.5bps to 0.52%. Gold fell -2.0% on the week, while Oil rose +3.7%.

Macroeconomic View – French unemployment down

French ILO unemployment dropped unexpectedly from 9.6% to 8.9%. It was further proof of the strength in the French, and subsequently, the European economy. European equities lost 1.5% briefly after the US inflation report was released, with figures higher than expected. The market recovered, but the move is indicative of the factors that affect traders. […]

Weekly Market Update: Inflationary pressures may be moderating. Supply chain pressures aren’t.

Equities in most major markets posted losses last week with global stocks down -0.4% in Sterling terms, as inflation concerns, supply chain issues and rising coronavirus cases dampened investor sentiment. US stocks were up +0.1% with growth stocks exhibiting solid gains, outweighing the losses in more cyclical firms. European stocks were down -1.8%, as countries within the region started imposing restrictions to curb rising Covid-19 cases. UK stocks were down -1.6% amid CPI inflation figures hitting a ten-year high, while EM equities fell by -1.7%. The US 10Y Treasury yield was down 2.2bps finishing the week at 1.548%, while the UK 10Y yield was down 3.5bps reaching 0.880%. In US Dollar terms gold lost some of its previous weeks’ gains, down -1.3%, while oil was heavily down -6.2% to $76 per barrel.

Macro of the Week – Fed hikes rates, more expected

As widely expected the FOMC raised the Fed Funds Rate target by 0.25% to a range of 1.5% – 1.75%, in what was a unanimous decision by the committee. It was the sixth rate hike since the GFC as the central bank looks to ‘normalise’ interest rate policy and was the first major decision under […]

Weekly Market Update: Equity Markets Rebound, Gold continues to soar

Read our Full Market Update Market Update Bucking the trend of two consecutive weeks of falling equity markets, all major indices were positive last week. Global equities gained +2.7% in Sterling terms, with the Nasdaq Composite reaching new highs, and the S&P 500 now close to its February peak. After a poor week last week, […]

Macro of the Week – US wages accelerate

US hiring picked up in January and wages rose at the fastest pace since the GFC. Hourly earnings increased 0.3%, resulting in an unexpected year-on-year increase of 2.9%, up from 2.7% in December (which was also revised up from 2.5%). This was on the back of a nonfarm payrolls increase of 200k, which was upwardly […]

Market Update A generally positive week for equities in local currency terms was slightly negative in Sterling terms as markets became increasingly optimistic about a UK trade deal with the EU, sending the Pound higher. UK equities were the notable exception for the week, though down only -0.1%. Overall, global stocks gained +1.7% in local […]

Weekly Market Update: UK Equities on Track for Second-Best Month on Vaccine Rally

Market Update Once again vaccine optimism supported global equity markets; this time it was the turn of the AstraZeneca vaccine, which can be more readily stored and transported. Global equities rose +2.1% for the week in Sterling terms. Financials and Energy were the two best performing sectors, as both sectors would benefit greatly from a […]

Macroeconomic View – German exports accelerating

German exports were weak for the month, up only 0.3%, but are still accelerating year-on-year. Chinese exports were stable, but imports picked up significantly, offsetting last month’s weak data. UK The Markit Services PMI dropped slightly to 53 from 54.2. The Halifax House Price Index year-on-year for the 3 months to January fell from 2.7% […]

Weekly Market Update: Lockdowns and US Election Raise Market Volatility

Market Update Global equities suffered their worst week since March, with the sell-off attributed to renewed virus related lockdowns across most of Europe and the final stretch of the hotly contested US presidential campaign. Global and US equities were both down -5.0%. This was despite the fact that Tech giants Alphabet, Amazon, Apple and Facebook […]

Weekly Market Update: Markets Mixed As Lockdowns Reimposed Over Second Wave Concerns

Market Update Global equities were narrowly down -0.3% on the week in local terms, however Sterling weakness once again boosted returns to British investors. The US was the best performing region, up +1.0% in Sterling terms. This coming week will kickstart earnings season in the US, where earnings are expected to fall sharply relative to […]

Weekly Market Update: Rising Equities Shrug off Political Uncertainty

Read our full Market Update Market Update Major global markets were generally positive in local currency terms, but a strengthening Sterling, up +1.5% for the week against the US Dollar, eroded gains for British investors. US stocks recovered from their four-week losing streak to rise +1.5% in US Dollar terms, but would return -0.2% due […]

Weekly Market Update: Virus Fear and Bank of England Comments Drag Down Equities

Read Our Full Market Update Market Update Globally stocks were negative in local terms for the second successive week, losing -1.2%. Sterling recovered some of its losses against the US Dollar, up +0.9% despite comments from the Bank of England suggesting an increased likelihood of rate cuts. UK stocks outperformed global stocks in Sterling terms, […]

When the black swan visits

Since 2018, a key concern of financial markets has been the increasing trade tensions between the United States and China, more commonly referred to as the ‘trade war’. With delays and failed negotiations lasting over a year, markets finally breathed a sigh of relief on the 15th of January, as the US President Donald Trump […]

Xi Jinping’s Infinite Rule

Things have been looking up for China recently, as market sentiment towards the world’s second largest economy has finally started to take a positive turn. Since 2015, when the country’s stock market sold-off sharply and the Shanghai Composite Index crashed 45% in under two months, investors have understandably been wary of China. Redemptions in Chinese […]

Weekly Market Update: Global Equities Rise, but Sterling Rallies More

Market Update Global stocks rose +0.7% in local currency terms, which translated into a -0.4% fall in Sterling terms. Returns were mixed in local terms, however were universally down in Sterling term as the currency rose +1.0% vs the US Dollar to just short of the $1.30 mark. Emerging Markets had a challenging week falling […]

Weekly Market Update: Weak Week for Sterling

Market Update Major developed market equities gained in Sterling terms this week, due in large part to currency effects. Many of these indices actually fell in local currency. UK equities grew by +1.1% led by utilities and healthcare sectors. US stocks were up +0.4% in Sterling terms but had fallen -1.0% in local currency, this […]

Weekly Market Update: Major indices end the year on a positive note

Market Update Most major equity market indices ended the year on a positive note. Global stocks gained +0.2% in Sterling terms over the last two weeks of trading to close the year up +12.4% in Sterling terms. Over the year, due in large part to a Tech rally following the early pandemic crisis, US stocks […]

Market Volatility: This dance we have danced before (and shall again)

Financial market turmoil continues for the second straight week, plunging the S&P 500 close up to 7% from its peak, in a bout of volatility similar to last December’s. The reasons behind the recent tumult are rather straightforward: 1) A stock re-rating, after Fed Chair Powell last week suggested that the central bank is not entering […]

Macro of the Week – UK GDP slowing

The UK economy grew more slowly than previously estimated in Q4 2017, increasing by 0.4% quarter-on-quarter according to the second estimate by the ONS. This figure was a 0.1% downgrade from the original estimate. The downward revision was due to slower […]

Weekly Market Update: Global equities rally amid strong economic data

Read our full Market Update Week 27 Market Update US equities hit record highs last week as data on Wednesday showed the US trade deficit rose to a five-month high while services sector data showed a slowdown in activity, increasing hopes that the Fed would turn more dovish. These hopes were curtailed on Friday as nonfarm […]

Weekly Market Update: BoE’s Chief Economist dissents to put 2018 rate hike on table

Read our full Market Update Week 25 Market Update Global stocks turned negative last week following two weeks of positive performance. Emerging Market equities were the worst hit, falling -2.0% in Sterling terms, as rising trade war fears also weighed on global equities, which were down -0.7%. Japan was also badly hit due to its […]

The difference between a skirmish and a (trade) war

Why geopolitics now matter more In the past few years, investors and economies have grown somewhat insensitive to geopolitical surprises. Brexit, for example, did not cause the massive initial shock to either the economy or the stock markets that many analysts had predicted. Neither did Mr. Trump, whose election has sent stocks soaring by more […]

How much of the FTSE’s strength is due to currency effects?

Currencies have historically been extremely volatile, and predicting FX movements is recognised as a very difficult and risky strategy. Exchange rates move on several, often unpredictable, macro-economic factors, including differences in interest rates or inflation, geopolitics or due to government intervention such as capital controls. Many funds have exposure to currency risk from investing in […]

The Current (Trade) War

In the past weeks we saw markets react negatively to fresh tariffs on China. However, it is more likely that traders were simply responding to the Federal Reserve’s attempts to maintain its independence against the US President by taking a more staunch view on the cost of money. The Fed’s independence might just be an […]

Is China facing an economic slowdown?

China was the first country to successfully emerge from the initial Covid-19 wave. People were back to the office in 2020 itself, infection rates plummeted and as a result economic growth was stellar, beating all expectations. China emerged as the winner at a time when most western countries were still coming to terms with the […]

Weekly Market Update: Improving Economic Outlook and Falling Volatility Support Equity Markets

Global equities rebounded from their sharp sell-off last week, rising +4.0% in Sterling terms. US equities were some of the best performing, rising +4.5% and more than recovering the previous week’s losses in spite of weaker than anticipated labour market data. UK equities rose +1.3%, the worst performing major region. Energy particularly struggled, in spite of rising oil prices, as UK energy giants BP posted its first annual loss in a decade, while Royal Dutch Shell profits fell 71%. European equities rose +2.8%. Emerging Market equities fared best, up +4.8%, reverting back to their trend of equity leadership in 2021. Globally, all sectors were positive with the Technology sector the strongest. Sterling rose +0.2% and +1.0% against the US Dollar and Euro respectively, continuing its strengthening trend this year. The US 10Y yield rose 9.8bps to 1.16%, while the UK 10Y rose 15.5bps to 0.38%. Gold fell -2.0% on the week, while Oil rose +8.7%.

Weekly market update: The Fed is not the answer to everything!

US, UK and European equities were relatively unchanged in Sterling terms last week, faring -0.1%, +0.1% and -0.1% respectively, amid concerns that the rate of global growth could start decelerating. Japanese equities were up +4.0% despite the resignation of Prime Minister Yoshihide Suga, while emerging market equities were up +2.7%, positive for a second week in a row after the Chinese tech sector had fallen significantly in previous weeks. Globally, stocks were up +0.3%, with energy and financials being the only sectors exhibiting losses. The US 10Y Treasury yield was down -1.5bps finishing the week at 1.322%. The German 10Y Bund yield was up +6.2bps amid higher than expected inflation in the euro area. Sterling was up +0.8% against the US Dollar and unchanged relative to the Euro. In US Dollar terms gold lost -0.1%, while oil prices rose slightly by +0.1%.

China’s property sector woes

China’s Evergrande Group has rapidly become Beijing's biggest corporate threat as it wrestles with debts of more than $300 billion as a result of years of aggressive expansion. But that was just the tip of the iceberg.

Investing in a world without QE

Inflation rising may upend a 12-year investment paradigm. Is there life after Quantitative Easing?

Weekly Market Update: A game of variants

Equities in most major markets posted large losses last week with global stocks down -1.8% in Sterling terms, driven by a sharp sell off on Friday after news that the new omicron coronavirus variant could be extremely contagious. US stocks were down -1.3% despite positive economic data being published earlier in the week, with weekly jobless claims hitting their lowest level since 1969. European stocks were down -3.8%, as certain countries continued to impose restrictions to curb rising Covid-19 cases. UK stocks were down -2.4%, while emerging market equities fell by -2.7%. The US 10Y Treasury yield was down 7.3bps finishing the week at 1.473%, while the UK 10Y yield was down 5.4bps reaching 0.825%. In US Dollar terms gold fell -1.3%, perhaps surprisingly given the perception it is a defensive asset, while oil was heavily down -10.2% to $68 per barrel.

Weekly Market Update: Was it a good idea for the BoE to surprise markets? Probably not.

Equities in most major markets posted gains last week with global stocks up +3.3% in Sterling terms, amid continued strong investor sentiment. US stocks were up +2.0% on the back of positive earnings surprises, a dovish Fed meeting and strong employment data. EU stocks were up +3.2%, with the ECB insisting that rates will stay low for the near future. UK stocks were up +1.0% as the BoE unexpectedly kept interest rates unchanged, which caused Sterling to fall -1.4% against the US Dollar. Globally, consumer discretionary and IT were the best performing sectors while financials and healthcare were the worst performing. The US 10Y Treasury yield was down 10.6bps finishing the week at 1.455%, while the UK 10Y yield was down 19.0bps reaching 0.845%. In US Dollar terms gold was up +3.4%, while oil was down -1.3% to $81.2 per barrel.

Weekly Market Update: Santa rally, or not, we remain equal weight

Equities in most major markets posted gains last week with global stocks up +1.4% in Sterling terms, amid stronger investor sentiment. US stocks were up +1.7% as positive earnings surprises continued for a second week in a row. EU stocks were up +1.2% despite heightened concerns that a rate hike could come sooner than expected, while UK stocks were down -0.4% as the latest inflation readings remained above the BoE’s 2% target. Globally, most sectors posted gains with healthcare and utilities being the best performing, while materials and telecoms underperformed. The US 10Y Treasury yield was up 6.2bps finishing the week at 1.632%, while the UK 10Y yield was up 3.9bps reaching 1.145%. Sterling remained flat against the US Dollar. In US Dollar terms gold was up +1.4%, while oil was up +2.9% reaching $84 per barrel.

Weekly Market Update: Look it’s China

Equities in most major markets posted gains last week with global stocks up +1.1% in Sterling terms, amid some improved economic figures. US stocks were up +0.8% as the earnings season kicked off strongly with major banks beating earnings expectations. EU stocks were up +1.6% despite a contraction in the industrial sector while UK stocks were up +2.0% amid strong macroeconomic data showing output growth during August. Globally, almost all sectors posted gains with cyclicals outperforming relatively versus more defensive stocks. The US 10Y Treasury yield was up 3.8bps finishing the week at 1.574%, while the UK 10Y yield was up 5.6bps reaching 1.105%. Sterling rose by +1.0% against the US Dollar. In USD terms gold pulled back by -0.4%, while oil was up by +2.5% reaching $82 per barrel.

Weekly Market Update: Reducing to equal weight

Equities in most major markets pulled back amid inflation worries, persistent supply side issues and more contractionary anticipated monetary policy - global stocks were down -1.6% in GBP terms. US stocks were down -1.2% as uncertainty loomed around the federal debt ceiling and the approval of the USD 1 trillion infrastructure bill. EU stocks were down -1.2% amid higher than expected inflation while UK stocks were down -0.3% despite an upward revision of latest GDP figures. Globally, Energy stocks continued their upward trend for another week in a row posting solid gains of +4.9%, with the rest of the sectors pulling back. The US 10Y Treasury yield was up 1.2bps finishing the week at 1.465%, while the UK 10Y yield was up 8.2bps reaching 1.00%. Sterling fell by -1.0% against the USD. In USD terms gold rose by +1.6%, while oil was up by +3.5%.

The UK’s energy market and its broader implications

Much of the recent news in the UK has been devoted to the spike in household energy costs and the potential collapse of the number of providers in that market from around 50 to 10 by the end of winter. In fact, since writing this first draft of this piece 2 providers have gone bust, leaving more than 800,000 customers without a provider. Of itself this is an interesting topic: it seems remarkable that rising wholesale gas prices can rupture the UK energy market and reduce the number of energy providers by 80%. For us the more relevant question relates to the wider economy and how energy costs can impact consumer demand and inflation, which contributes to our discussions when deciding asset allocation. This blog post aims to explore the former and explain the Mazars Investment Team thinking on the latter.

Weekly Market Update: China’s ‘LTCM moment’ may be the least of its problems, and ours.

Global stocks were relatively unchanged in Sterling terms (down -0.7% in USD terms) last week amid investors’ skepticism around supply chain issues hampering growth, elevated valuations and future monetary policy. Japanese stocks posted gains for a consecutive week, rising by +1.1%, as campaigning began for the next president of Japan’s ruling LDP. UK stocks fell by -0.9% amid higher than expected inflation, while US stocks were up +0.2% driven by a strengthened US Dollar. Globally, all sectors exhibited losses apart from energy stocks which posted solid gains of +2.8%. The US 10Y Treasury yield was up 2.1bps finishing the week at 1.363%, while the UK 10Y yield was up 8.9bps reaching 0.848%. Sterling fell against the US Dollar by -0.7% and remained flat against the Euro. In US Dollar terms gold lost -1.2%, while oil was up by +4.0%.

Weekly market update: How much longer can liquidity mask reality?

Global stocks were down -1.1% in Sterling terms last week amid fears of momentum fading and growth concerns due to the persistence of supply chain issues. Japanese stocks were the only region to post gains, rising by +3.8% in Sterling terms, buoyed by news of prime minister Suga stepping down and expectations of further stimulus. UK, US and European equities were all down -1.5% driven by inflation concerns and uncertainty about the economic outlook. Globally, all sectors exhibited losses apart from consumer discretionary. The US 10Y Treasury yields were up 1.7bps, finishing the week at 1.343%. German 10Y Bund yields were up +2.6bps to -0.332% after the ECB announced it would reduce the pace of its pandemic asset purchasing programme. Sterling fell against the US Dollar by -0.2% and rose by +0.4% vs the Euro. In US Dollar terms gold lost -2.1%, while oil was up by +0.7%.

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

Inflation momentum will recede. But prices may remain elevated.

There’s a strong possibility we may see the end of the episode soon. But supply chains could take long to mend and overall price levels could remain elevated versus pre-pandemic numbers.

Quarterly Outlook: An investor’s inflation and growth playbook

Investing during the past twelve years has been underpinned by a basic principle: market participants have been encouraged to take risks, mainly to offset the trust shock that came with the 2008 financial crisis (GFC). Each time equity prices have fallen significantly, the Federal Reserve, the world’s de facto central bank, would suggest an increase in money printing, or actually go ahead with it if volatility persisted. Bond prices, meanwhile, kept going up, as central banks and pension funds were all too happy to relieve private investors of their bond holdings even at negative yields. Market risk was all but underwritten.

Is gold a good hedge against inflation?

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise.

Weekly Market Update: Markets Grapple With Eventual Tapering of Asset Purchases

In a relatively volatile week of equity market trading, ultimately most major equity markets ended nearly unchanged. Following on from US inflation last week, there was increased focus on the UK and EU readings this week, with investors looking for any evidence of a potential shift in monetary policy. US equities fell most of major equity markets for British investors, down -0.7% in Sterling terms, although more modestly in local currency terms. UK equities ended a mixed week down -0.2% as the effects of stronger than anticipated labour market data and inflation played out. Emerging markets and Japanese equities saw a role reversal last week as they moved from laggards to leading markets, with emerging market equities providing the best returns to Sterling investors up +1.4% on the week. European equities rose +0.6% in Sterling terms. The US 10Y yield fell -0.7bps to 1.6%, while the UK 10Y fell -2.7bps to 0.8%. In commodity markets, gold rose +1.7%, while oil fell -2.9% to $64.1 a barrell.

Weekly Market Update: Mixed Results in Equity Markets as Economies Reopen but US Jobs Disappoint

With many regions operating a shortened trading week, returns varied significantly across major equity markets. UK equities provided the best returns to Sterling investors, up +2.4%. The rise in UK equities was helped in part by rising commodity prices, with miners and energy firms benefiting from rising metal and oil prices. European equities provided the next best returns, up +1.7% in Sterling terms. US equities rose a modest +0.2% in Sterling terms, though up +1.3% in local currency terms, as the rotation from growth to value impacted returns. Emerging markets fell -1.0% in Sterling terms. Japanese equities rose +1.3% in Sterling terms, not quite enough to move the region into positive territory year-to-date. The US 10Y yield fell temporarily on bad jobs data, although recovered somewhat, ending down 4.9bps to 1.6%, while the UK 10Y fell 6.7bps to 0.8%. Gold rose +2.4% on the week, while oil rose a further +1.0% to $65.4.

Weekly Market Update: Consumer-Led Recovery at Close to Fastest Pace in Modern History

Once again many major equity markets finished the week not far from where they started. Market attention was squarely focused on the Federal Reserve, where chairman Jerome Powell promised not to raise rates in the near term; as a consequence, markets did not sharply react in either direction. US equities were flat in US Dollar terms, but up +0.2% in Sterling terms. UK equities were the best performing region, up +0.5% last week. European equities fell for the second consecutive week, down -0.8% in Sterling terms. Emerging markets fell -0.2% in Sterling terms. Japan was the clear laggard, where earnings failed to meet expectations and the Bank of Japan kept policy unchanged. Japanese equities fell -1.9% in Sterling terms. The US 10Y yield rose on improved economic data, up 6.8bps to 1.6%, while the UK 10Y rose 9.8bps to 0.8%. Gold fell -0.3% on the week. The better than expected economic data helped oil to rise +2.4% last week to $64.4.

Weekly Market Update: Indian Covid Crisis Captures Attention of Markets

Equity markets ended the week largely unchanged, with the largest movements seen in Japanese and UK stocks. UK equities fell -1.1%, driven in part by a falling oil price, as the global economic outlook increasingly uncertain, with clear inequality in the vaccination progress between regions, dampening expected demand for oil. US equities fell -0.3% in Sterling terms, with plans to raise capital gains tax only making a slight impact on US markets. European equities rose +0.2% in Sterling terms due to currency effects, having fallen -0.4% in local currency terms. Emerging markets were the only risers in local currency terms, and were up +0.1% in Sterling terms. Globally the best performing sector was healthcare, whilst energy was the worst performing. The US 10Y yield fell slightly by 2.2 bps to 1.6%, while the UK 10Y fell 2 bps to 0.7%. Gold fell -0.2% on the week. Oil fell as the economic outlook deteriorated, down -1.7% on the week to $62.1.

Weekly Market Update: Caveat Emptor

UK equities reached the highest level in over a year as part of a broad-based rally in equities globally. Equity markets continue to benefit from increasing risk appetite as investors become increasingly bullish on a 2021 recovery. UK equities rose +1.6%, although it remains one of just a few regions not back to all time highs.US equities rose +0.7% in Sterling terms, the stronger growth moderated by Sterling rising +0.9% against the US Dollar. Globally the best performing sector was materials, whilst telecoms lagged other sectors. The US 10Y yield fell 7.9 bps to 1.6%. The UK 10Y yield was more or less unchanged, down just 1.0 bps to 0.8%. Gold rose +1.1% on the week, although it remains -7.6% so far this year. Oil rose +5.7% last week to $63.1 a barrel. Oil is up +28.5% this year. The jump in oil prices comes in spite of global coronavirus cases beginning to rise in many regions, with several European and Asian economies looking likely to increase the stringency of lockdowns.

Weekly Market Update: Rational Exuberance

Markets opened positively this week thanks to the impact of stronger than anticipated US payrolls data released over the bank holiday. Meanwhile, the EU vaccination campaign is finally beginning to pick up pace. US equities rose +3.4% in Sterling terms, reaching further record highs. UK equities rose +2.7% in the final week before the second phase of lockdown easing. European equities rose +3.2% in Sterling terms, supported by the increased likelihood of fiscal stimulus in the region. Emerging market equities fell in local currency terms, but gained +0.1% in Sterling terms. Globally, the best performing sector was information technology, whilst energy was the worst performing. The US 10Y treasury yield fell slightly down 6.3 bps to 1.7%, while the UK 10Y gilt yield fell 2.1 bps to 0.8%. Gold rose +1.6% last week. Oil fell for the second week, down -2.8% to $59. Oil has fallen almost -20% from its earlier surge, driven partly by a more challenging route out of the pandemic than originally forecast.

Will the rotation into value continue?

While it remains to be seen how long value leadership will last, many of the drivers that led investors to flock to growth stocks have reversed and now favour value stocks.

Relative to the year so far, last week saw quite a heterogeneous response to news by markets. On one hand there is continued and growing positivity surrounding the opening of economies, but this has lead to some inflationary concerns. Meanwhile, the Suez Canal blockage raised concerns about supply chain disruptions. US equities rose +2.2% in Sterling terms, hitting record highs, helped by a more optimistic vaccine schedule from President Biden. UK equities rose a more modest +0.6%. Globally the best performing sectors were more defensive names such as consumer staples and utilities, whilst telecoms was once again the worst performing. Japanese equities fell -1.5%, moving back into contractionary territory this year. The US 10Y yield fell slightly, down 4.5bps to 1.7%, while the UK 10Y fell 8.1bps to 0.8%. Neither gold nor oil were much changed, both down -0.1% on the week, with oil trading just under $60 a barrel.

Weekly Market Update: Stocks ended the week near all time highs

A positive week for equities saw all major equity markets close the week positive in local currency terms. With Sterling continuing its bullish start to the year this pushed EM equities down to a flat week in Sterling terms. US equities rose +2.0% in Sterling terms, hitting record highs. US equities were helped by falling bond yields, from Tuesday, which helped boost equity investor sentiment. UK equities rose +2.1%. Globally the best performing sector was consumer discretionary, whilst telecoms was the worst performing. Japanese equities rose +1.5%, erasing their losses year-to-date. The US 10Y yield continued its rise, although more modestly, up 5.9 bps to 1.6%, while the UK 10Y rose 6.6bps to 0.8%, reversing last week’s fall. Gold rose +0.8% on the week. Oil fell, after last week’s strong rise, down -1.4% on the week to $65.8. Oil is up +32.6% on the year, highlighting the extent to which vaccination programmes are increasing forecasters’ outlooks for economic activity later this year.

Market Comment – Macro headwinds

Last year was very positive, both in terms of stock market and macroeconomic volatility (the volatility of macroeconomic releases). In recent weeks, however, we have noticed a deterioration in macroeconomic releases, especially in the US. Lower inventories and higher imports took a toll on GDP. More detailed data on capital expenditure also shows weakness in […]

Copyright 2020 - Mazars

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.